New York Community Bancorp's struggles

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netNew York Community Bancorp, a midsized New York lender, once looked like a winner of the regional banking crisis of 2023. Now it's in trouble.

Why it matters: The bank's shares have been plunging over the past week — and with more than $100 billion of assets, NYCB is big and important enough that its failure, were it to happen, would reverberate nationally and even internationally.

Where it stands: NYCB is not a Wall Street institution. Its headquarters are literally in a town named Hicksville, a place that senior investment bankers might occasionally fly over in a helicopter on their way to their summer house in the Hamptons.

- NYCB's assets — its loans — are heavily weighted toward commercial and multi-family real estate. The former has been hit hard by the failure of New Yorkers to return to the office after the pandemic, while the latter has suffered in the wake of a 2019 law that made it much harder for landlords to raise rents.

The big picture: NYCB has been diversifying via acquisitions.

- At the end of 2022 it bought Flagstar Bank, bringing in a broad branch network and deposit base.

- In 2023 it acquired most of the assets of Signature Bank, a crypto-heavy lender that failed on the same weekend as Silicon Valley Bank. (NYCB didn't take on any of the crypto assets.).

The good news: NYCB's acquisitions gave it a much broader base of operations, and also put most deposits under the Flagstar brand. The recent decline in NYCB's share price hasn't (yet) resulted in deposit outflows at Flagstar, whose name hasn't been front and center in NYCB stories.

- The bad news: After the two acquisitions, NYCB found itself over the $100 billion mark for total assets — a level which comes with significantly increased scrutiny from regulators and stricter capital requirements.

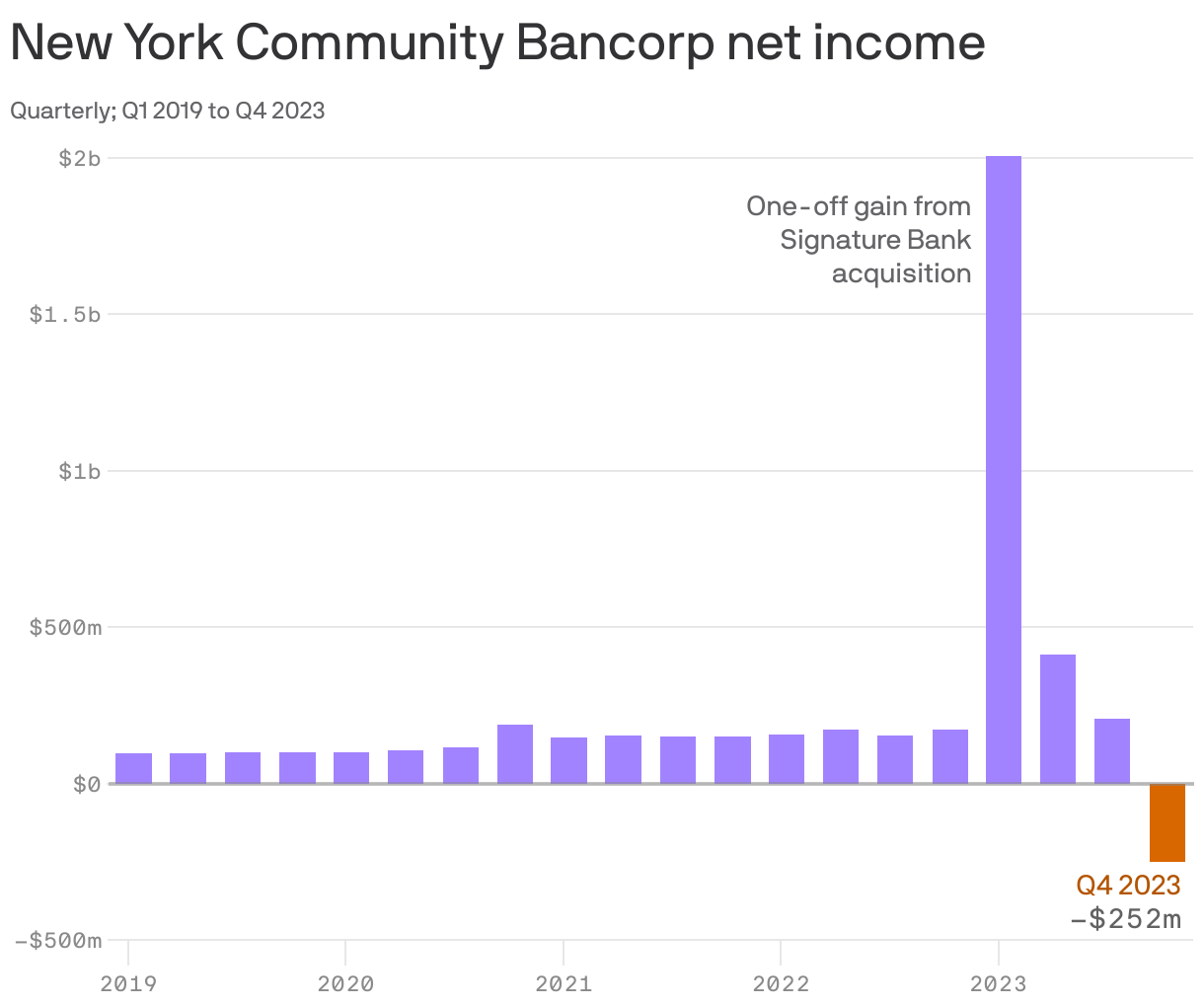

Driving the news: On Jan. 31, NYCB announced it had lost money in the fourth quarter, after taking a $552 million provision for credit losses on its commercial real-estate portfolio. It also slashed its dividend.

- That precipitated a plunge in the share price, as well as the revelation that the bank's chief risk officer and chief audit officer had both been pushed out.

- On Tuesday, Moody's cited "high governance risks" as it downgraded the bonds of NYCB's parent company to junk status. (Flagstar Bank, however, retains its investment-grade deposit rating.)

What's next: The bank responded Wednesday morning by announcing that Sandro DiNello, the former CEO of Flagstar who had been serving as non-executive board chair, would take on an executive role alongside CEO Thomas Cangemi.

- DiNello took the reins in a call with analysts Wednesday morning, where he underscored the strength of NYCB's deposits, the bank's underlying profitability, and its plans to improve its capital ratios.

- Bloomberg reported Wednesday that NYCB is trying to offload mortgage risk on about $5 billion of home loans, and that it might sell a portfolio of roughly $1 billion in loans on RVs and boats.

- That turned out to be enough to counteract the force of the Moody's downgrade, and the stock rose modestly on Wednesday.

The bottom line: DiNello did his best on the call to not sound panicked. But in banking, trust is everything — and the markets tend not to trust any bank whose share price has fallen more than 50% in the space of a week.

Go deeper: NY Community Bancorp shares plunge amid property loan concerns