At Dish Network, a bondholder vs. shareholder fight is brewing

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Natalie Peeples/Axios

One of the year's biggest debt market fights is taking shape.

Driving the news: Dish Network shareholders, and multiple warring factions of the company's bondholders, have become combatants in a clash that could turn into a battle royale.

The big picture: The brewing struggle centers on a controversial balance sheet maneuver to help address looming debt maturities and avoid the prospect of bankruptcy — but it protects shareholders at the expense of creditors.

Why it matters: It flips an investing mainstay on its head — if a company faces balance sheet trouble, shareholders are supposed to bear the losses first. Higher risk, higher reward.

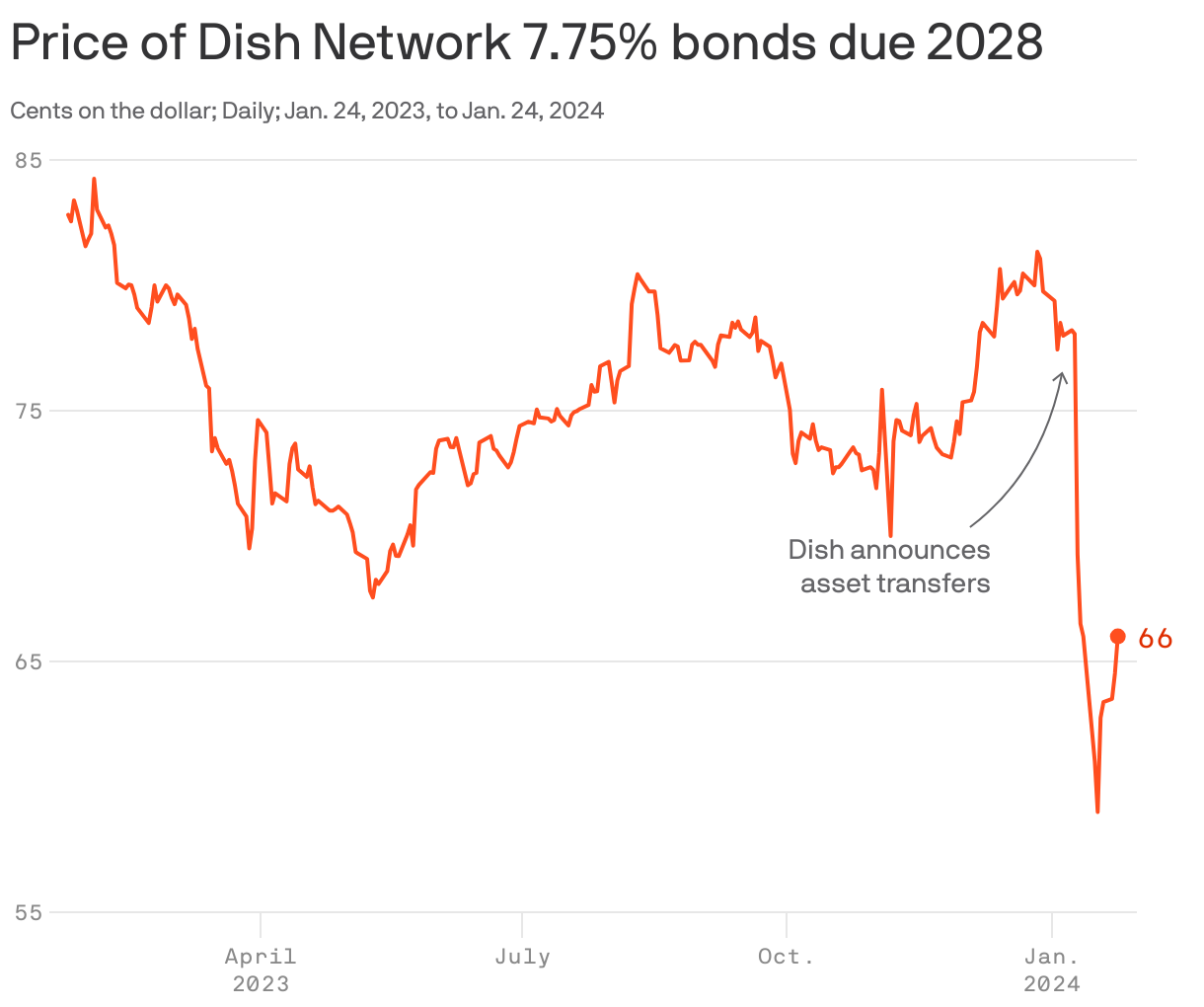

What's happening: Dish announced this month that it's moving some of its assets into a new subsidiary, and plans to use those assets to back a new debt issuance that will help address upcoming maturities.

- That may sound like no biggie — regular corporate finance stuff — except that some of Dish's existing bonds had a claim on those assets before they were moved. Those bonds are now worth less, and the bondholders who lost the assets are not pleased.

- Meanwhile: Shares of Dish parent EchoStar, controlled by telecom mogul Charlie Ergen, surged on the announcement of the transactions (though they've since given up some of those gains).

"The asset transfer trend is just starting, and I think we're going to see it more and more. We'll continue to see more pushing of the envelope," says John McClain, high-yield portfolio manager at Brandywine Global.

- It amounts to "a wealth transfer from debt-holders to equity-holders," he adds.

How we got here: Historically, high-yield rated companies (those with lower credit ratings) always had a bunch of rules in their loan and bond agreements — putting companies on a tight leash for how they use their cash and other assets.

- That's supposed to force the companies to prioritize paying back creditors over doing shareholder-friendly stuff.

Yes, but: In the post-financial crisis loose-money era, these rules (known in the market as covenants) started to weaken.

- Borrowers pushed for ever weaker covenants, and the debt-investing community acquiesced, largely because of supply and demand. There always seemed to be more cash chasing deals than actual deals to invest in. It was a borrower's market.

- The weaker covenants paved the way for companies, if they ran into trouble later on, to get a little more creative if they couldn't pull off a regular-way refinancing.

- In 2016, J. Crew blazed the trail: It was the first to pluck assets out from under its existing creditors and use them to raise new debt — igniting the trend and spawning the term "J Screwed" (seriously).

Where it stands: More recently, rapidly rising interest rates have swelled the ranks of companies that may have trouble refinancing their upcoming maturities — including Dish, which has over $20 billion in debt, much of it trading at distressed levels.

- "There is no doubt that, as financing becomes harder for stressed issuers to access, they'll look for creative ways to extend runways, to extract value from their creditors, and to restructure themselves without being forced to go through a bankruptcy," says Josh Kramer, senior distressed analyst at CreditSights.

Zoom out: Though these types of asset transfers have become more common, they never fail to light up the debt market with fury and pushback (see also: Revlon, Neiman Marcus).

- The deals usually wind up in court, because the way the covenants are written often leaves room for interpretation, and creditors look for any legal hook to block the transaction. (Court verdicts have so far been a mixed bag.)

- The Dish situation already looks to be heading toward litigation. Multiple groups of bondholders have formed and hired lawyers — and at least one of those groups already sent a threatening letter to Dish's board alleging the transactions are fraudulent, Bloomberg reported.

Worth noting: From the company viewpoint, these transactions are supposed to buy them time.

- But for all the time and resources spent fighting over their legality, the transactions often don't accomplish their ultimate goal: keeping the companies out of bankruptcy.

- J. Crew, Revlon and Neiman Marcus all ultimately filed for Chapter 11 within a few years of their asset transfers.

The bottom line: A central paradox of financial capitalism is that bondholders have first claim on a company's assets, but shareholders are the ones who actually run it.

- The closer a company gets to bankruptcy, the greater the tensions that tend to result.