A Wall Street trade that roiled COVID-era markets is back

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

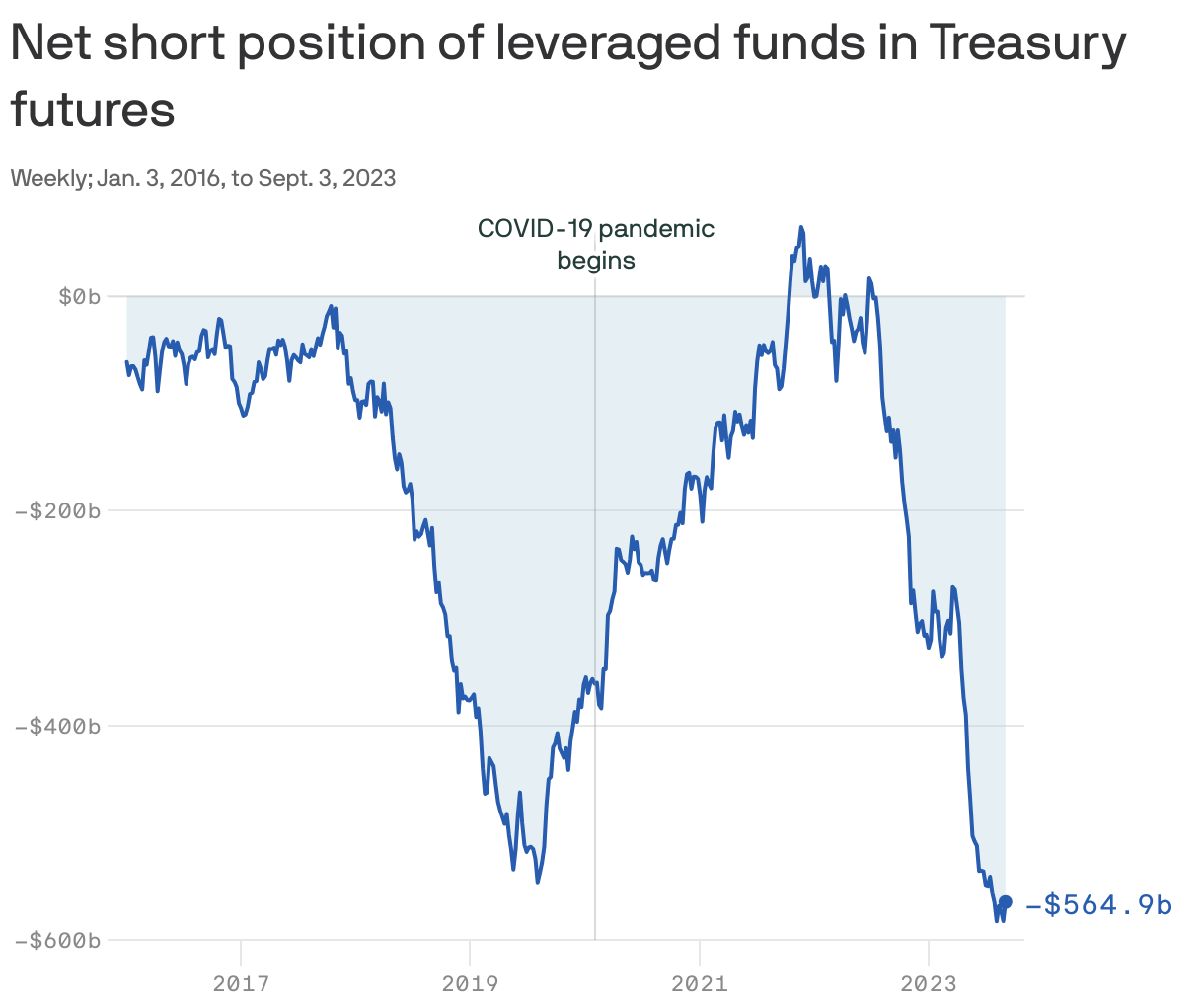

Open embedded content from datawrapper.dwcdn.netHedge funds are piling in once again to a trade that was popular before the COVID crisis — until it blew up.

Why it matters: In March 2020, this bet went bad and amplified the chaos in the most important market on earth, the market for U.S. Treasuries.

- The Federal Reserve was forced to pump massive amounts — about $2.5 trillion — of newly printed money into the markets to put out the fire.

The latest: Over the last couple of months, there's been a range of renewed warnings about the growth in the size of this trade, known as the "Treasury cash-futures basis trade," or just "the basis trade."

- In August, Fed researchers rounded up the evidence that the trade was back, noting that "sustained large exposures by hedge funds present a financial stability vulnerability."

- In September, the Bank for International Settlements — often called the central bank for central banks — noted in its quarterly report that the buildup in the trade "is a financial vulnerability worth monitoring."

Zoom out: Despite wars, congressional chaos, persistent inflation, and volatile markets, the U.S. economy is actually in pretty good shape.

- But adding a messy unwind of a big Wall Street trade to the mix probably isn't a great idea — so it's worth exploring exactly what this trade is about.

What's the basis trade?

It's either a masterpiece of the art of arbitrage — or a prime example of "picking up pennies in front of a steamroller." Or both.

The big picture: The basis trade consists of two separate Treasury market bets, that, when combined, can generate what looks like free money.

An overly simplified explanation goes something like this:

- Buy a Treasury security, say a two-year note, in the regular old Treasury market, which is known as the "cash" market.

- Go to the futures market, and sell a contract to someone — usually to a large asset manager — who will pay you to deliver the same Treasury security in a few months at a price higher than the one you paid.

For example: You pay $100 for a Treasury note, then deliver it to the futures market three months later for $100.50. Congrats, you made half a percentage point on the trade.

- The trade works when futures prices for Treasuries are a teensy bit higher than the price paid for the actual cash bond, as they have been lately.

Yes, but: A 0.5% return isn't enough for any self-respecting hedgie.

- So hedge funds amplify those returns by using a lot of borrowed money — also known as leverage.

How that works: Let's say you only put up $10 of your own money and borrow the other $90 to own the $100 bond.

- When you deliver the Treasury bill to the futures market, you still collect $100.50 and you still earn 50 cents on the trade.

- But if you only used $10 of your own money, that's a 5% return, rather than half a percentage point. Not bad.

Go deeper: Unlike a mortgage, which can last 30 years in the U.S., the term for repo loans can be a single day.

- That means the hedge fund has to find a new lender each day to provide it with the one-day mortgage on its Treasury — and the interest costs associated with that loan can change.

Most days this is no problem. Repo is a giant wholesale financial market where between $2 trillion and $4 trillion worth of these loans are made each day as a matter of course.

- Part of the reason the market functions is that everybody knows that Treasury bonds, which are the vast majority of assets financed in the market, are basically the safest investment on earth, and therefore the perfect collateral.

- But once in a while, a giant shock appears that makes people question such assumptions — like a once-in-a-century global pandemic.

What happened: When the realities of COVID hit the U.S. in early 2020, it sparked a worldwide rush to convert investments into cold hard cash.

- Usually, Treasuries are viewed as pretty much the same thing as cash. But the uncertainty surrounding COVID was so vast, investors were reluctant to even hold Treasury bonds.

- Amid the rush to sell, Treasury prices grew increasingly volatile.

- That volatility spooked repo lenders, who raised repo lending costs to protect themselves against growing risks.

- The rising cost to finance the cash bond leg of the trade effectively turned the basis trade into a money-loser.

- So these hedge funds exited the trade en masse, essentially selling all their Treasuries, which put further downward pressure on Treasury prices and magnified the death spiral of selling.

Worth noting: Nobody knows precisely how much the blowup of the basis trade in 2020 contributed to the disorder in the Treasury market. But the mass selling certainly didn't help.

Read more: The regulators' dilemma