Rising rates make America's fiscal arithmetic worse

Add Axios as your preferred source to

see more of our stories on Google.

Suppose you expect your income to rise 5% a year, and you borrow money each year at a 6% interest rate with no plans to pay it down. The debt service will take up a rising share of your income.

- That is the situation the U.S. government now faces after a shift in bond markets in recent weeks has worsened America's fiscal arithmetic.

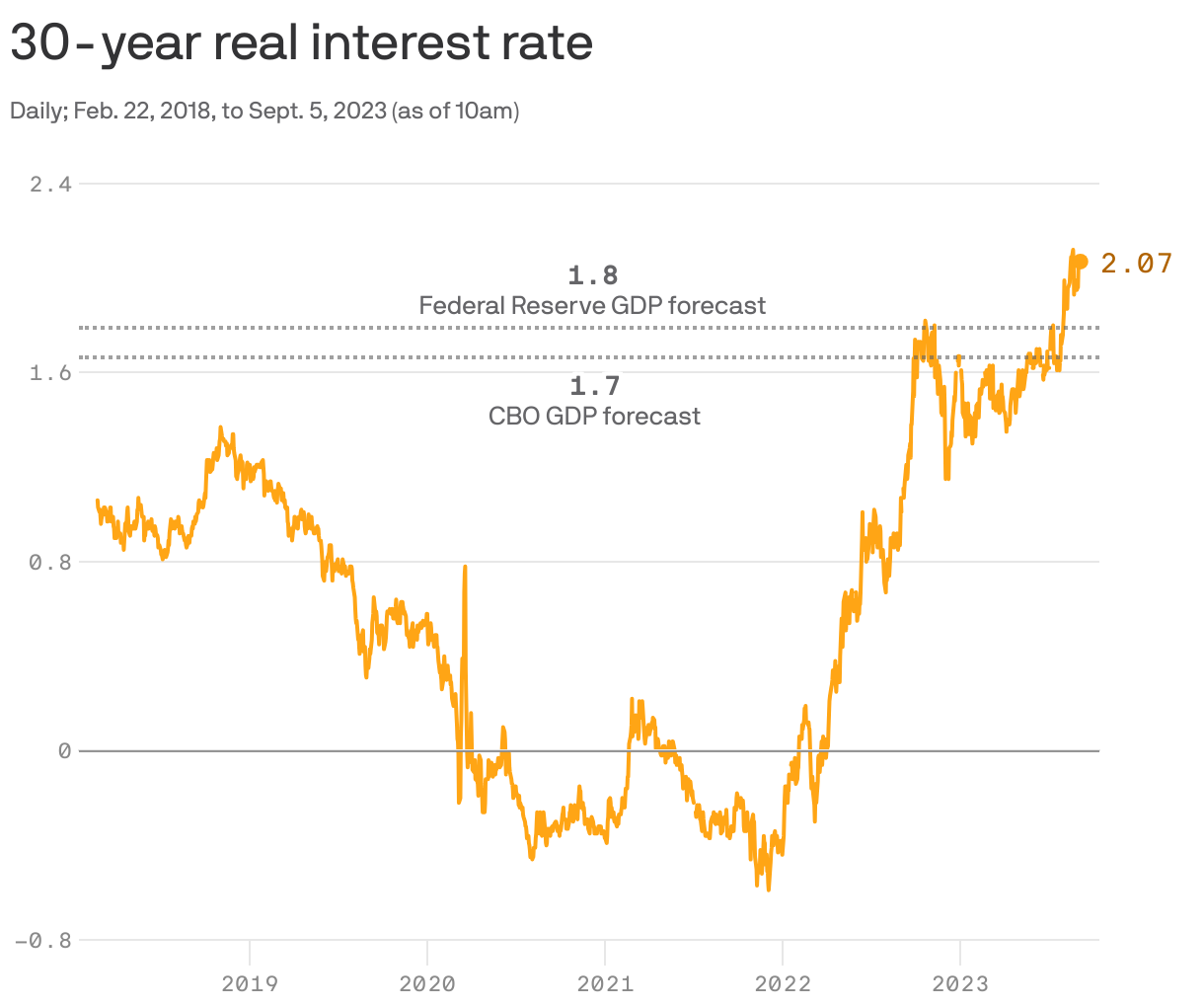

Driving the news: Real yields — the interest rate the government pays on inflation-protected bonds — have risen sharply since July and are now higher than mainstream estimates of real GDP growth for the coming decades.

Why it matters: If current rates and growth forecasts hold, the cost of servicing existing debt will become more onerous, even apart from additional debt from future deficits.

- It's a reversal of the dynamic from 18 months ago, when real yields were well below projected growth, giving many economists comfort that even sizable public debt was manageable.

By the numbers: The Congressional Budget Office's projections for GDP growth over the coming decade average 1.7%. Federal Reserve officials' long-term projection is 1.8%.

- As recently as July, real interest rates were below those levels. The 30-year inflation-protected Treasury yield was 1.61% on July 24, for example. Those numbers were below zero as recently as March 2022.

- But August's surge in yields has flipped the story. The 30-year real yield was 2.07% on Tuesday morning.

- To use economists' shorthand, it used to be the reassuring case that r < g (rates were lower than growth). Now, r > g.

The intuition: The numbers wouldn't be terribly worrying if the United States were running a primary surplus — bringing in more revenue than it spends on everything other than debt service costs.

- But that is not the case. Instead of a primary surplus, the CBO's projections include an average 3% primary deficit over the coming decades.

- In other words, it's not just that the math of servicing existing debt is getting worse. The U.S. government is still adding to that debt pile.

What they're saying: "We're facing an increasingly worrying triple whammy," said Jason Furman, a Harvard University economist and former chairman of the White House Council of Economic Advisers.

- "Starting from a high debt level, adding to it every year with non-interest spending in excess of tax receipts, and now we can no longer count on the cushion of growth rates well above interest rates," he tells Axios.

- "It won't force an imminent crisis, but policymakers cannot ignore this indefinitely," he said.

Yes, but: The actual interest rates the U.S. government faces as it rolls over debt in the coming years could vary significantly from what is currently priced into long-term bonds.

- Economic growth could prove stronger than projected if, for example, there were an artificial intelligence-driven productivity spike, or a surge in labor supply due to immigration.

- If the recent surge in rates turns out to be temporary or caused by rising productivity growth, then it wouldn't damage long-term fiscal math, Brookings Institution economist Louise Sheiner said.

The bottom line: Sheiner said that if the higher real interest rate persists, "and if it isn't offset by higher productivity growth, it means we have to do somewhat more to cut the deficit, but not really much more than was already baked into CBO projections."