FedNow launch hints at payments wars to come

Add Axios as your preferred source to

see more of our stories on Google.

The launch of the FedNow instant payments system on Thursday marks official ratification from the U.S. central bank of a model that has taken off very impressively elsewhere in the world.

The big picture: If it catches on here, the biggest losers are likely to be the major credit card issuers.

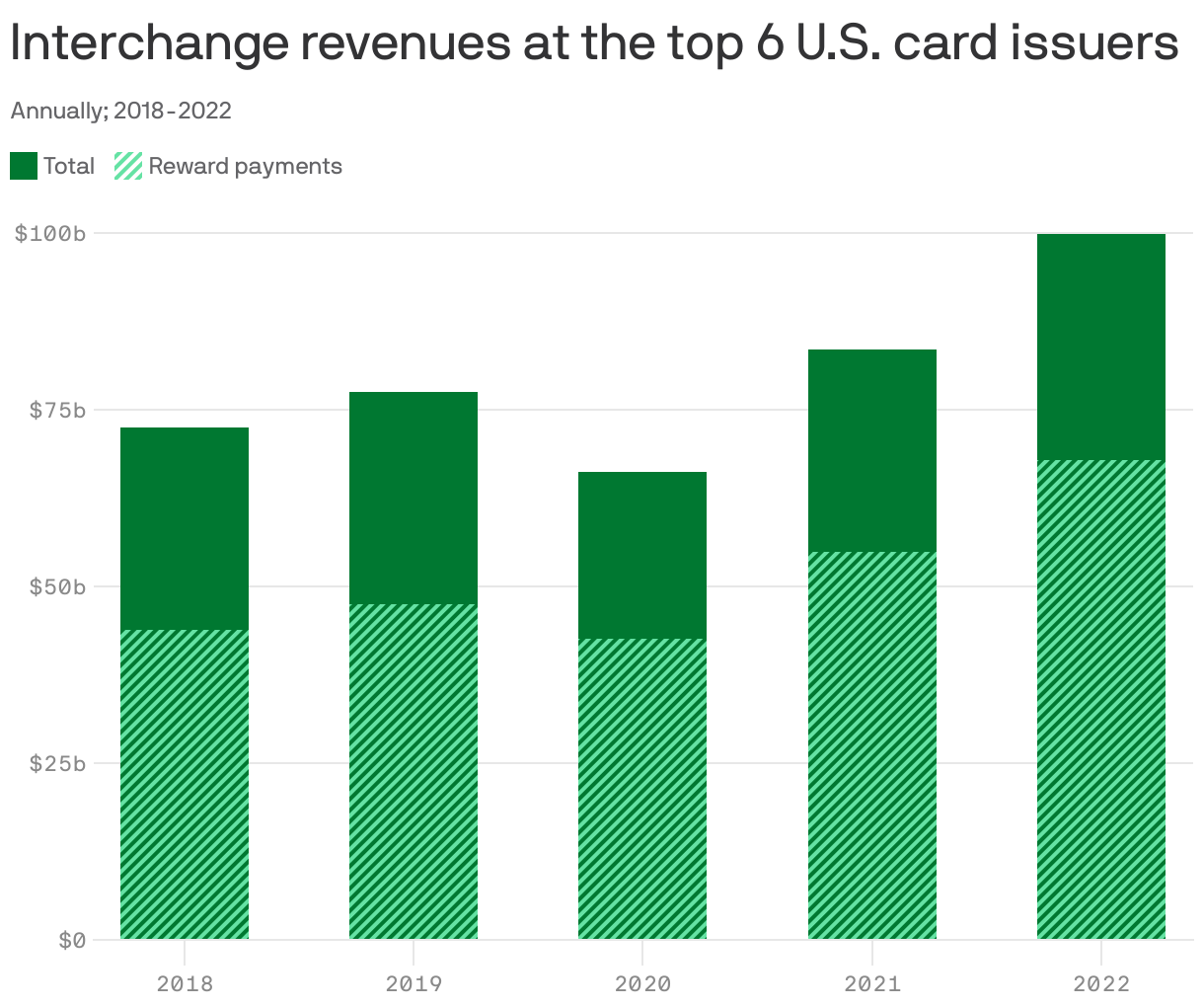

Why it matters: Interchange fees — the swipe fees paid by merchants when customers pay by credit card — reached $100 billion in 2022, per Matt Schulz of Lending Tree. That's more than $800 per household.

- In order to encourage credit card usage, issuers give cash, miles, or other rewards to consumers. The top six card issuers spent $67 billion on such activities last year.

Where it stands: In a world where goods cost the same regardless of how they're paid for, it's entirely rational for consumers to pay with credit cards and then collect their kickbacks.

The other side: There's no particular reason why this kind of financial intermediation should be a $100 billion industry, rife with inefficiencies. (My own rapidly rising pile of unused American Express points is a prime example of value being lost to time and laziness.)

- "The shift to instant payments is inevitable," writes TD Cowen analyst Jaret Seiberg in a research note, "though it will take time."

- FedNow, alongside its private-sector rival RTP, is a behind-the-scenes technology. Eventually, it will be built into point-of-sale terminals so that customers can buy things by transferring money instantly out of their checking account. But that's likely to take a while.

Zoom out: To get a feel for how fast instant payments can get adopted, just look to Brazil.

- Pix, the Brazilian instant-payments system, was nonexistent pre-pandemic. Today, per Matera, a Brazilian payments software company, Pix sees 8.1 billion transactions per quarter. That's more than the next two highest payments methods — credit cards and debit cards — combined.

- Credit card transactions have fallen by 20% in one year.

- “Pix shows how intuitive payments can be," says Matera CEO Carlos Netto. "It poses the greatest threat yet to credit card dominance."

Be smart: Pix isn't winning just because it's easy to use, but also because merchants are aggressively pushing it, making it the default payment option and even offering discounts for customers who use it.

- That's because the average Pix interchange fee is just 0.33%, compared with 2.34% for credit cards.

The bottom line: Americans will be slow to give up their credit cards. But if merchants get aggressive in pushing us toward something more instantaneous, they could end up saving tens of billions of dollars in interchange fees.