Layoffs, shutdowns hit mortgage industry as high rates crush lending

Add Axios as your preferred source to

see more of our stories on Google.

After getting laid off from her job at mortgage provider Better.com in March, Charmaine Steele interviewed at eight other mortgage companies. Each one subsequently announced layoffs of their own, she tells Axios. At least one has gone out of business.

Why it matters: It's lean times in the real estate business. The slowdown is a warning for the economy more broadly, and a rare labor market weak spot at a time of strong overall employment.

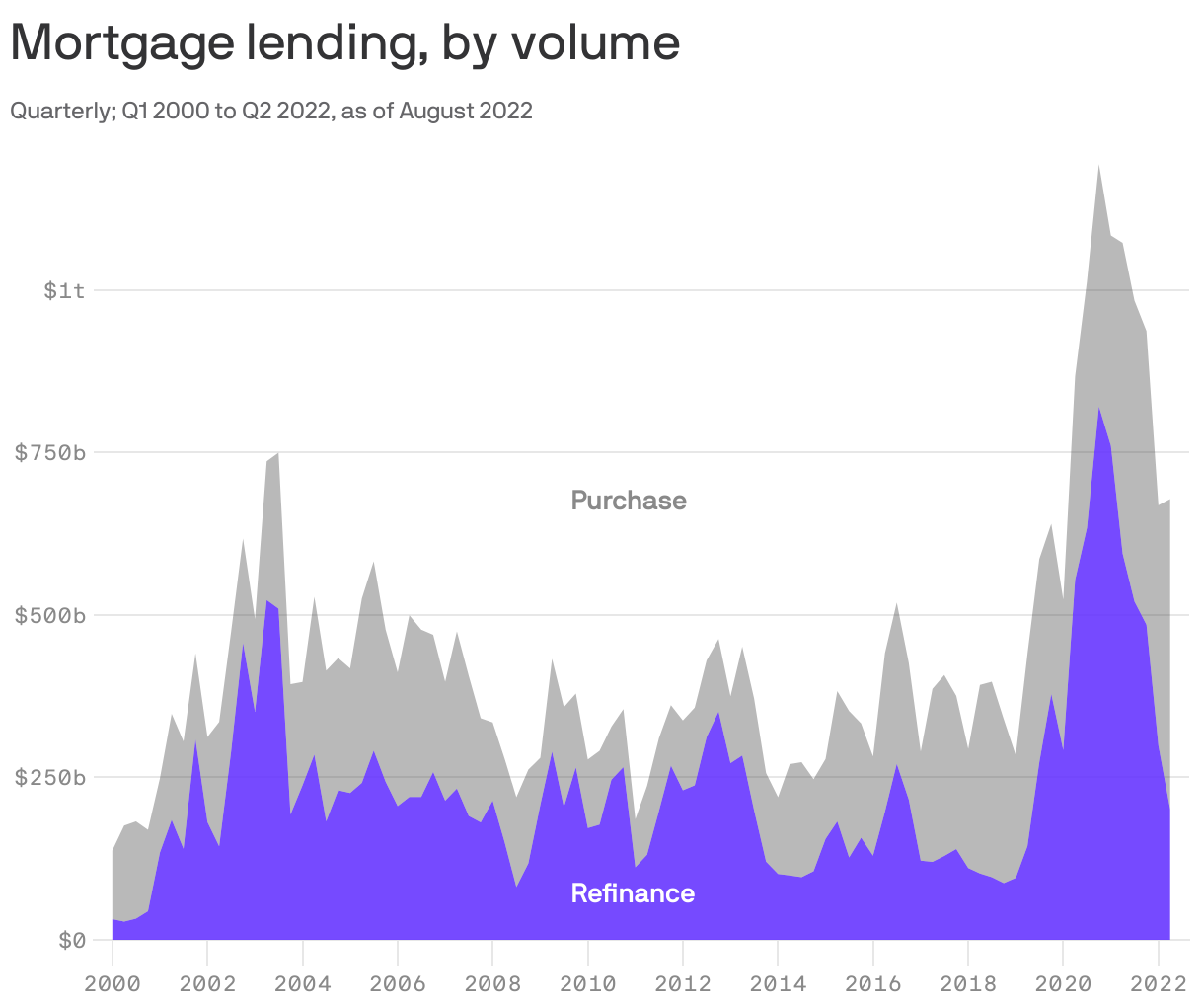

- With interest rates hitting 14-year-highs, and lending activity way down from the peaks of the past two years, layoffs and shutdowns are happening with alarming frequency.

"The housing market tends to lead the broader economy both into and out of recessions," Mike Fratantoni, chief economist at the Mortgage Bankers Association, tells Axios.

- It was a grim job search, says the 30-year-old Steele, who lives in Charlotte, North Carolina. "Nobody was hiring anybody."

State of play: On Tuesday, real estate brokerage Compass announced the second round of layoffs. Just the day before, Opendoor — which is in the business of buying and flipping houses — announced it lost money on 42% of its transactions in August.

- Steele's former employer Better.com has done four rounds of headcount cuts, including the famously botched mass layoff via Zoom in December 2021, Tech Crunch reported.

- Real estate company Redfin laid off 8% of its staff in June.

- Rocket, one of the largest non-bank mortgage lenders, has done two rounds of cuts. Briefly a meme stock in 2021 when it traded at over $25, Rocket is now at less than $8.

- Small fintechs in the mortgage space, like Reali, closed up shop. Sprout, a mortgage company, also went out of business. First Guaranty Mortgage Corp. filed for Chapter 11.

By the numbers: "Mortgage banking and brokerage shops trimmed 3,600 full-timers from their payrolls in July," reports Inside Mortgage Finance, citing the most recent BLS data. "Hardly anyone is immune. If a lender isn't cutting staff, it's offering early buyout packages."

Catch up fast: Mortgage companies hired like crazy over the past couple of years, as low-interest rates drove a surge in refinancing. For a while, things were great for workers in the industry — some companies were paying seven-figure signing bonuses, Fratantoni told MarketWatch recently. (A spokesman for the MBA confirmed the eye-popping number with Axios Tuesday.)

- Steele says she was earning around six figures at Better.com, her first job at a lender after working as a real estate agent. She's now working in the small business lending space, making 50% less.

The bottom line: For those getting financial crisis flashbacks, this is different. Two-thirds of the mortgage business is now the province of small non-bank lenders — and Fratantoni estimates there are 4,500 companies in the space.

- Though banks have made cuts to their mortgage businesses, too, in recent months, they're much less exposed to housing overall.

- And there's far less likelihood of the kind of systemic spillover we saw nearly two decades ago. Improved underwriting standards mean borrowers have better credit (foreclosure rates are still low), and most of them have mortgages with rates under 5%.

Editor's note: This story was corrected to show the Redfin layoffs happened in June, not August.