Savings interest rates don't rise as quickly as you might think

Add Axios as your preferred source to

see more of our stories on Google.

As the Federal Reserve raises rates to fight creeping inflation, you might find yourself checking to see if your savings account's interest rate is rising to match. After all, the idea is to make saving more attractive than spending to cool an overheating economy, right?

Yes, but: Historically, savings account interest rates haven't climbed in lockstep with the Fed rate — even though they tend to fall when the Fed rate does.

Why it matters: As higher interest rates make it more expensive for Americans to pay off their mortgages, auto loans and credit card bills, many will be desperate for any financial leg up — especially as inflation skyrockets and even the basics get more expensive.

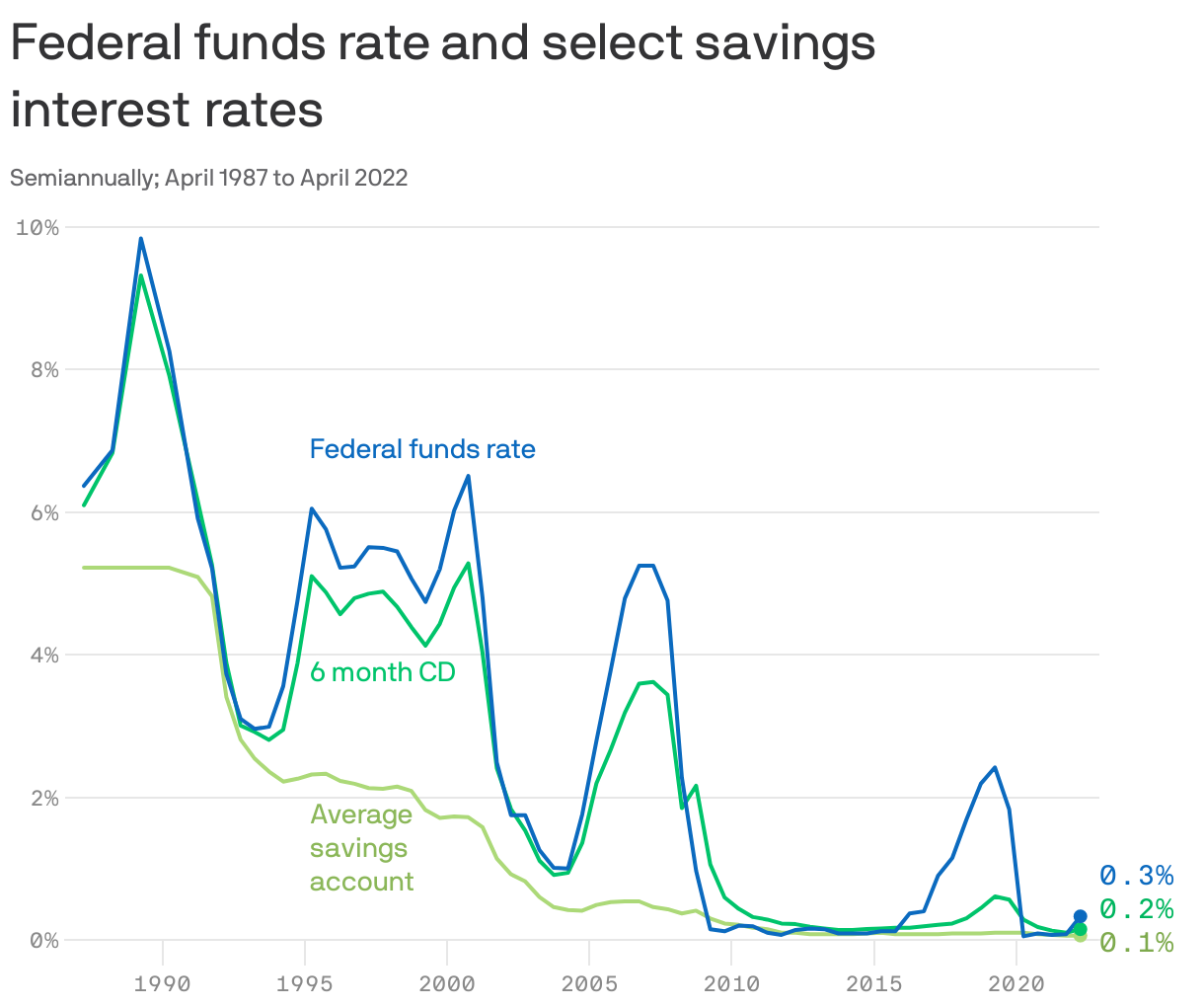

The details: The savings interest rate data charted above comes from Bankrate's survey of big U.S. banks, and "larger banks have a lot of pricing power," says Bankrate chief financial analyst Greg McBride.

- "They rarely pay up for liquid money such as savings accounts and checking accounts," adds McBride.

The big picture: Banks are historically slow to raise the rates they pay on deposit accounts — after all, they don't have to because they don't need to compete very hard for people's money.

- And while the nation's banks passed their annual Fed stress tests with flying colors last week — meaning they're prepped to weather a downturn — debate has emerged over whether banks should be holding more capital in reserve, which could make them more tight-fisted.

Where it stands: Even if the big banks aren't rushing to raise interest rates, you can still find relatively good alternatives by shopping around.

- "Banks that are hungrier for consumer deposits are paying much higher returns and are actively raising rates in this environment," says McBride.

- Some high-yield savings accounts, for example, are advertising rates over 1%. My account, via American Express Personal Savings, is at 0.9%, and seems to be climbing every week.

- Online high-yield accounts can offer better rates in part because they don't have the overhead of brick-and-mortar banks.

The alternatives ...

- Certificates of deposit (CDs) track the Fed rate much more closely. But they're offered on time-based terms (e.g. 6 months, 12 months, etc.), and you'll be penalized for early withdrawals — meaning they're not a great option for money you might need on short notice.

- Over long enough timelines, stocks blow traditional savings accounts out of the water, returns-wise (especially if you reinvest your dividends). But markets do sometimes fall — the S&P 500 is down around 20% year-to-date — whereas cash in a savings account will at the very least be insulated from market downturns.

- I Bonds — long-term government savings bonds with an interest rate that partially adjusts with inflation — offer rates above 9% and are all the rage among some money experts right now. But there's a limit on how many you can buy, and as with CDs, there are penalties for tapping out early.

What's next: Savings interest rates should keep rising "in the months to come" says Kendall Little, a personal finance writer at NextAdvisor.

- That's especially true for online-only banks, local banks and credit unions, Little adds, which are in much hotter competition with one another for your dollars compared with the big banks.

The bottom line: It's still hard out there for a saver. But remember that building wealth is a long-term process, and don't forget underused options like your employer's (401)k match, if they offer one and you're in a position to take advantage. That's just free money.