Interest rate inversions reflect questions about economy's health

Add Axios as your preferred source to

see more of our stories on Google.

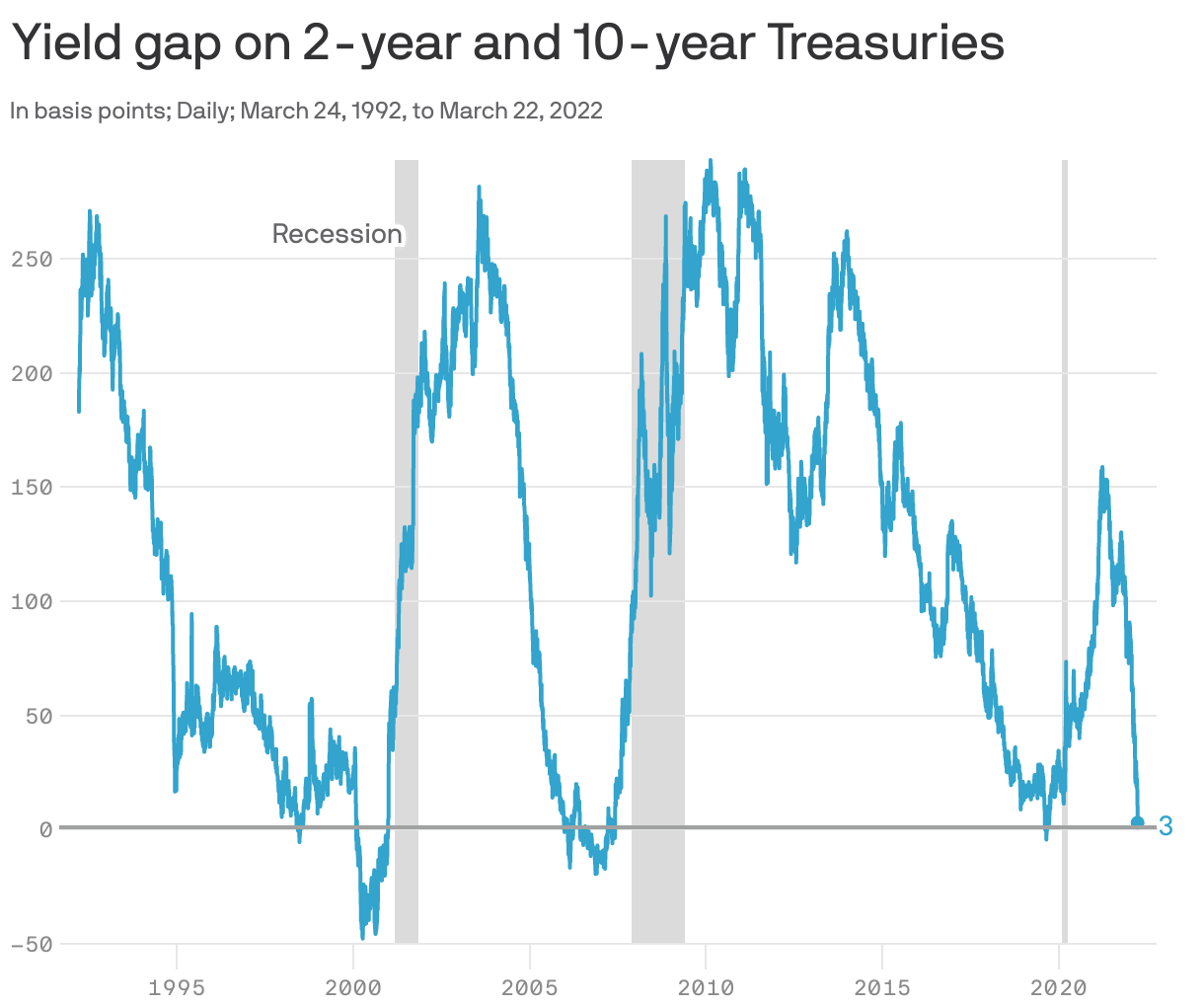

It's really happening. We're within spitting distance of the long-awaited inversion of the yield curve — at least the portion of it that covers the 2-year and 10-year notes.

What's new: Yields on the 2-year note briefly went higher than that of the 10-year note on Tuesday.

- Those notes ended the day at 2.37% and 2.40%, respectively — leaving just a hair between the current world and the massive economic anarchy that yield curve purists believe will surely ensue once long-term rates fall below those of short-term rates.

Backstory: When the cost for the government to borrow over the short term is higher than the cost for a longer period, that's known as an inverted yield curve (the curve between the 5-year and 30-year also inverted this week).

The big picture: While an inverted yield curve is one of the most reliable indicators of a looming recession, it's also subject to a wide range of interpretations.

- Meanwhile, the version of the yield curve that's supposed to have the best track record of predicting economic downturns is the gap between the three-month bill and the 10-year Treasury note — which right now remains hugely positive.

The bottom line: Still, the flattening curves seem to reflect growing concerns on Wall Street that the Fed is going to have to push the economy into a recession by jacking up rates — sort of a Volcker shocklette — if it's really going to get inflation under control.