First look: White House seeks to coordinate debt-ceiling message

Add Axios as your preferred source to

see more of our stories on Google.

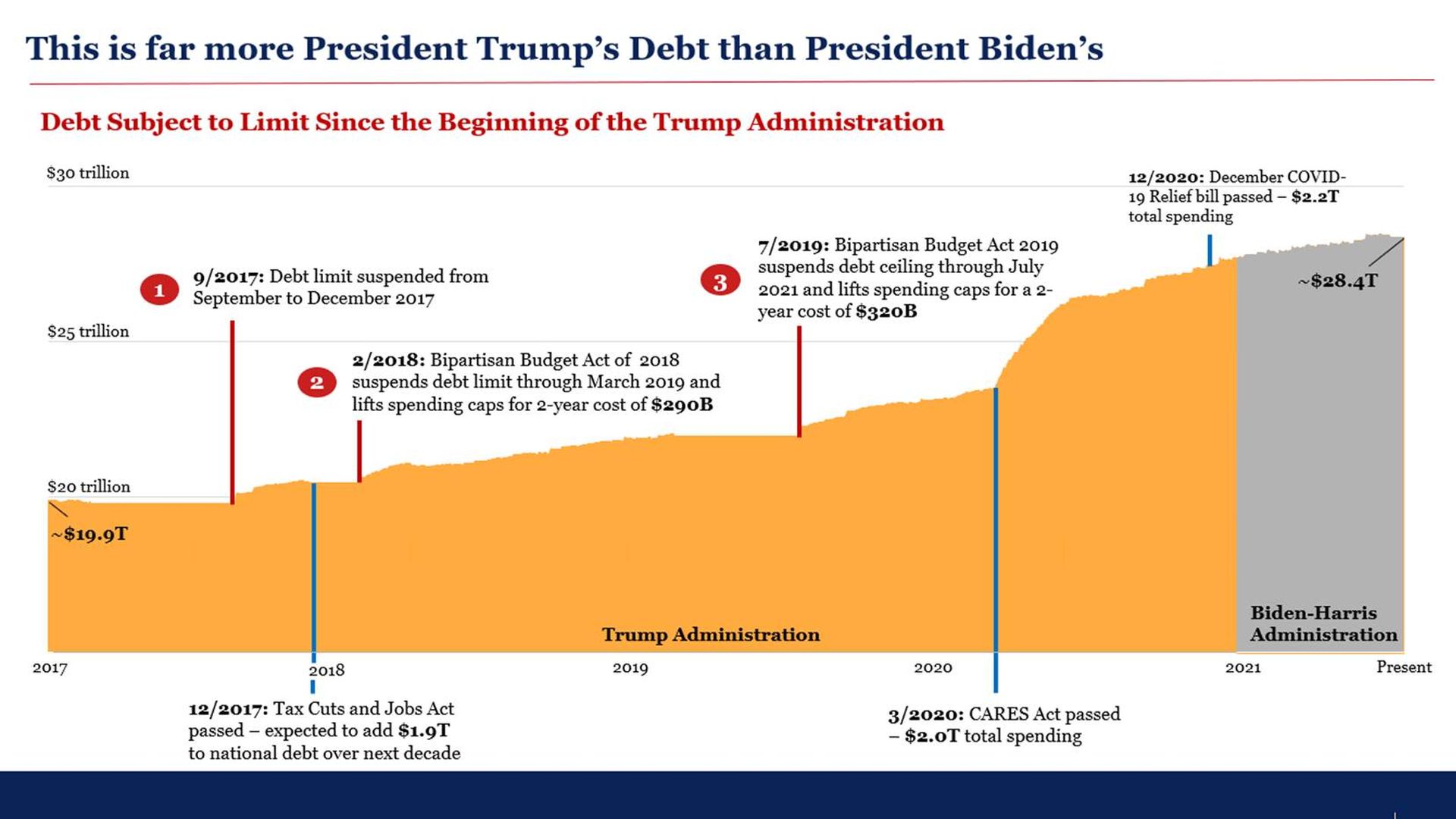

White House slide for congressional briefing about debt increase, obtained by Axios.

Biden administration officials are briefing senior Democratic Senate aides about why Congress needs to raise or suspend the federal debt limit.

Why it matters: By coordinating its message with Congress, the White House is trying to ensure Democrats stay unified on a simple argument: that 97% of the $28.7 trillion national debt was incurred before President Biden assumed office.

- Both the administration and Senate Democrats face a battle with Senate Minority Leader Mitch McConnell (R-Ky.) about how to protect the full faith and credit of the United States.

- He continues to warn that Republicans will not vote to raise the debt ceiling.

Driving the news: Bharat Ramamurti, a deputy director on the National Economic Council, and Ben Harris, a counselor at the Treasury Department, are dialing into the weekly meeting of Senate chiefs of staff held Wednesday mornings, according to a person familiar with the matter.

- Ramamurti, a former aide to Sen. Elizabeth Warren (D-Mass.) who is well-known on Capitol Hill, is explaining to his former colleagues why Congress should vote to increase or suspend the debt ceiling. He notes a Republican-controlled Senate did, with bipartisan votes, three times under President Trump.

- The officials will note the national debt increased $7.8 trillion during Trump's presidency, which accounts for 28% of its total.

- The national debt has increased by about $670 billion during Biden's first seven months in office.

- The officials have a similar briefing scheduled for Thursday for House staff.

The big picture: On Aug. 2, the Treasury Department was forced to resort to "extraordinary measures" to service debt.

- The last debt-limit suspension, passed in 2019, lapsed on July 31.

- The federal government will run out of money in either October or November, the Congressional Budget Office estimates.

- Predicting when the cash will dry up, though, is more of an art than a science. It's been made more difficult by the various tax and spending programs Congress passed to address the economic fallout from COVID-19.

What we're watching: The White House is nervous there will be turmoil in the financial markets the closer Treasury gets to default. That turmoil — and the threat of default — could drive up borrowing costs.

- There’s also a risk that veterans and Social Security recipients miss monthly payments.

Flashback: In 2011, Standard & Poor’s downgraded the U.S.’s AAA credit rating, as President Obama and congressional Republicans deadlocked about how to reduce annual budget deficits and increase the debt ceiling.

- They eventually cut a deal, but in 2013, Obama drew a line in the sand.

- He vowed he would “not negotiate over whether or not America should keep its word and meet its obligations.”

Between the lines: Democrats need Republican votes in the Senate to suspend the debt limit until a future date, but they can increase the total amount through their proposed $3.5 trillion budget reconciliation package.

- McConnell urged Democrats to pay any increase through reconciliation, which the party plans to pass without any Republican support — making it easier to saddle his opponents politically with greater debt.

- The reconciliation process, however, may not be completed before the debt limit is breached.

- That creates the potential for some Republicans to be forced to vote for an increase.

Go deeper: Get ready for debt-ceiling drama