Axios Pro Rata

March 09, 2024

Good morning, readers! This is a pretty historic week: Four years ago, the country implemented unprecedented lockdowns as the COVID-19 pandemic took over … and we're just a year removed from the collapse of Silicon Valley Bank. We're talking about the latter below.

- 👋 Reminder: Feel free to send me tips or comments by replying to this email or on X: @imkialikethecar. (Or ask me for my Telegram or Signal number.)

🚨 Situational awareness: OpenAI CEO Sam Altman has rejoined the company's board as part of a new lineup following last year's leadership shakeup.

Today's Smart Brevity™ count is 836 words — a 3-minute read.

1 big thing: A not-so-happy anniversary

Illustration: Aïda Amer/Axios

As if pulled from a movie script: Just days before the one-year mark of Silicon Valley Bank's collapse, New York Community Bancorp has avoided the same fate, thanks to a $1 billion cash infusion led by former Treasury Secretary Steve Mnuchin.

Why it matters: Despite all the ink spilled over the need to strengthen American banks in the past year, we're only at the beginning.

Catch up quick: On March 8, 2023, Silicon Valley Bank announced it had raised $500 million from General Atlantic and had plans to raise $1.75 billion to help it plug a hole in its balance sheet created by rising interest rates.

- Less than 48 hours later, regulators shut it down and took over.

- By then, crypto-friendly bank Silvergate had also been shut down; two days later, New York's Signature Bank would see the same fate.

- Before the end of the month, First Citizens had agreed to acquire SVB's core business, and on May 1, JP Morgan Chase said it was doing the same for First Republic.

Fast forward: Today, SVB says it's still the same bank customers loved, but with better risk management and some other tweaks, like smaller deposit requirements for startup borrowers, president Marc Cadieux told Axios last month.

- 81% of SVB's clients from a year ago are still banking with SVB, according to Cadieux, with "thousands of them" returning after initially switching out.

The big picture: The Federal Reserve, which was SVB's regulator, has so far mostly focused its efforts on proposing rules regulating banks' balance sheets and liquidity.

- This week, Fed Chair Jerome Powell told Washington lawmakers that the fiercely debated bank regulation proposal released last year — which includes capital requirement hikes — will have "broad and material changes."

- Yet, even as its own reports show, one additional failure was in enforcing existing rules.

What they're saying: "We put a Band-Aid on the structural problem and act like we fixed it," Brookings Institution senior fellow Aaron Klein tells Axios.

The other side: "I think there was an inference that this was a regional bank crisis, but it really wasn't — those were niche banks," Citizens CEO Bruce Van Saun tells Axios. "The failure was is in governance and the business model."

- Similarly, Van Saun (and others) pin NYCB's troubles on its outsized exposure to commercial real estate in New York, which is currently struggling.

Yes, but: Despite their flaws, SVB and FRB had businesses envied by some of their competitors.

- It's no secret that First Citizens had been angling for years to become better established within North Carolina's tech scene.

- Citizens launched a failed bid to acquire First Republic; even after it lost out, it still hired about 150 of FRB's private bankers, and is now gearing up to open three Bay Area offices.

The bottom line: As with all regulation, it'll be a long and slow road.

2. A boon for the new kids on the block

Illustration: Shoshana Gordon/Axios

SVB says it's still serving 81% of its old customers, but the events a year ago undoubtedly resulted in client defections that benefited the competition.

State of play: Many customers switched to other established banks, and a number of businesses shifted to startup-focused neo-banks. Here's how two of them fared:

Mercury: In the five days following SVB's collapse, more than 8,700 new customers flocked to Mercury with more than $2B in deposits.

- The firm debuted its Vault product, which includes up to $5 million in FDIC insurance through its partner banks and their sweep networks (deposits are spread across many banks).

- It also enables customers with more than $5 million to move additional funds into lower-risk, highly liquid mutual funds predominantly composed of short-term T-bills.

Brex: It took in 4,000 customers and $2 billion in deposits from March 9–16, 2023.

- Deposits increased 50%+ essentially overnight as a result of SVB's troubles.

- More than 90% of those that signed up during the week of the SVB collapse are still active Brex customers.

- More than one third of Brex customers now use its cash management product, up from fewer than 25% before.

- Today, Brex manages about $7 billion in customer deposits, up from about $3 billion before the events.

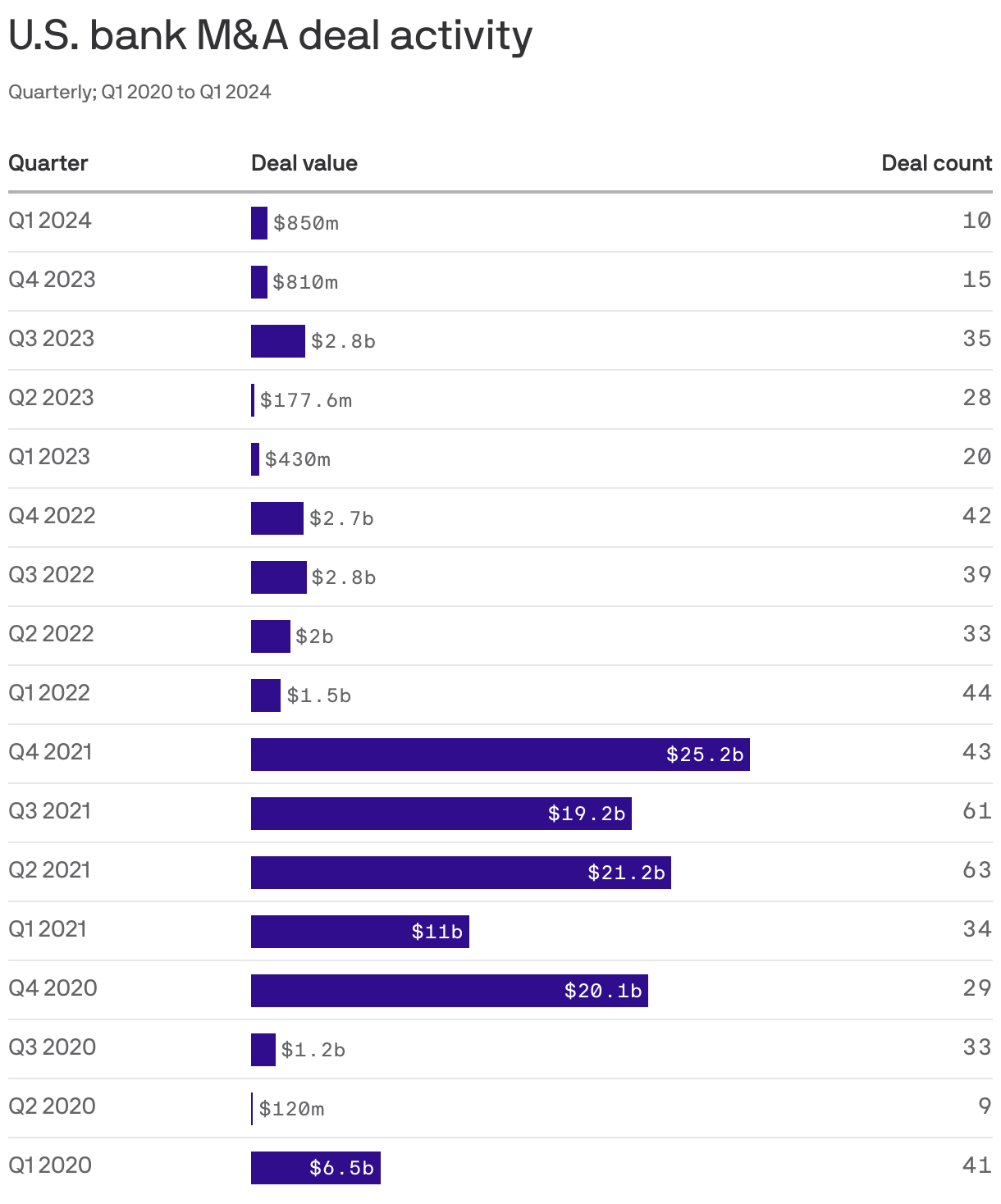

3. By the numbers: U.S. bank M&A

There's much more bank M&A activity than the few deals that grab the biggest headlines.

- Like broader M&A activity, bank sector deals dipped when the market turned two years ago, per S&P Global Market Intelligence data.

📚 Due Diligence

- How a surprise investment in NYCB helped avert a 2024 bank crisis (Axios)

- If one megabank collapses, the US economy goes with it. Should we have more? (Politico)

- One year after "all hell broke loose" at Silicon Valley Bank (Marketplace)

- How "credit risk transfers" could help banks shore up their balance sheets (Axios)

🧩 Trivia

In lieu of trivia this week, send me any and all of your thoughts on whether you're still banking at SVB, your banking strategy if not, and/or what the US should do to prevent bank crises!

🧮 Final Numbers

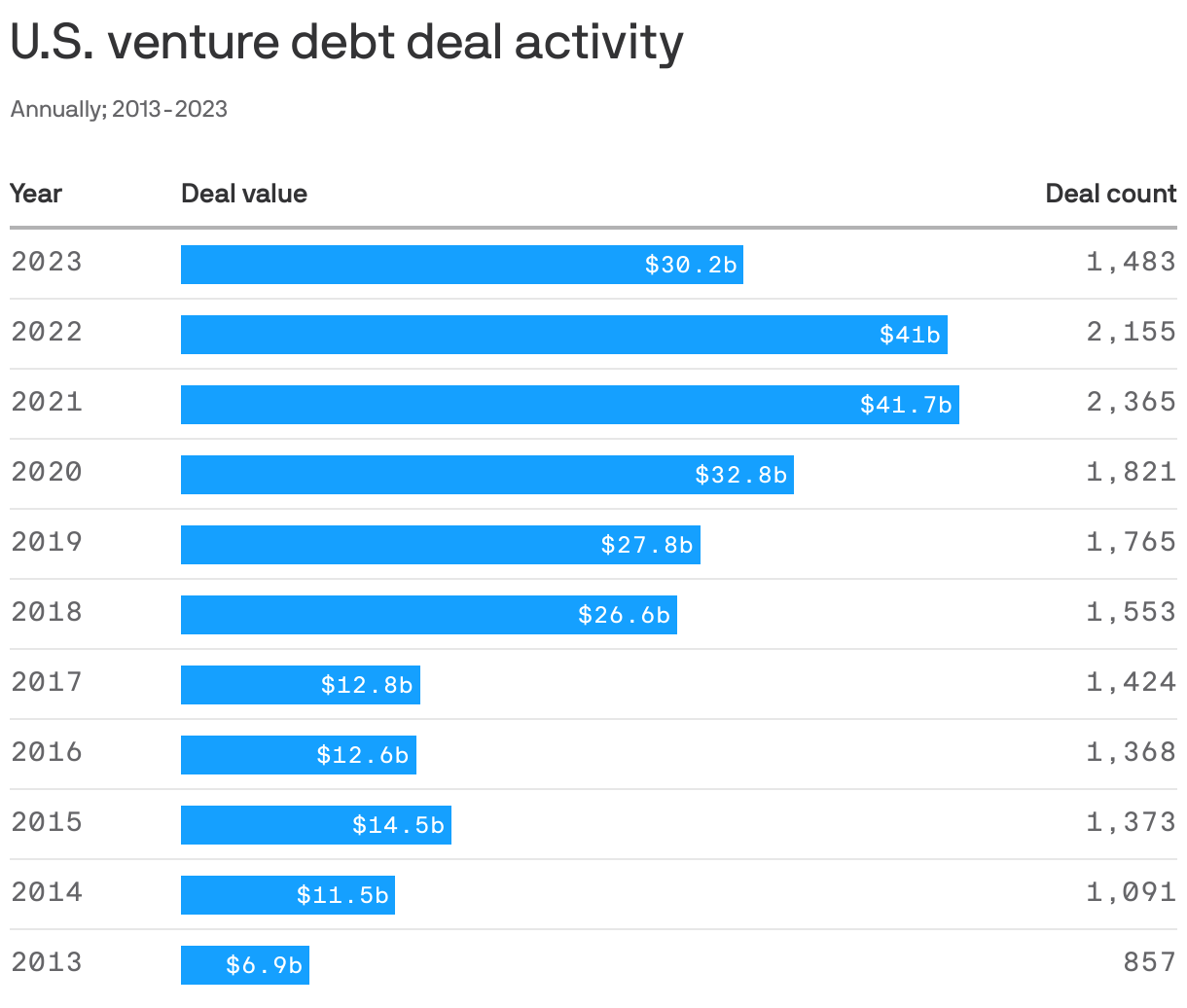

- SVB was (and still is) a prolific venture debt lender in startupland. As with everything else in the industry, levels peaked during 2021 and have declined since.

🙏 Thanks for reading! And to Javier E. David and Brad Bonhall for editing. See you Monday for Pro Rata's weekday programming, and please ask your friends, colleagues and contrarian private bankers to sign up.

Sign up for Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.