Axios Pro Rata

May 15, 2019

Top of the Morning

Illustration: Sarah Grillo/Axios

The BFD

Illustration: Sarah Grillo/Axios

Venture Capital Deals

• Away, a New York-based luggage maker, raised $100 million in Series at a $1.4 billion post-money valuation. Wellington led, and was joined by Baillie Gifford, Lone Pine Capital and Global Founders Capital. http://axios.link/OZQv

• Grofers, an Indian grocery delivery startup, raised $200 million. SoftBank Vision Fund led, and was joined by KTB and return backers Tiger Global and Sequoia Capital. http://axios.link/31i2

🚑 ArcherDx, a Boulder, Colo.-based personalized genomics company, raised $60 million in Series B funding. Perceptive Advisors led, and was joined by return backers PBM Capital, Boulder Ventures, Longwood Fund and Peierls Foundation. http://axios.link/nQGR

🚑 CinCor Pharma, a Cincinnati-based biopharma focused on cardiovascular, metabolic and kidney diseases, raised $50 million in Series A funding co-led by 5AM Ventures and Sofinnova Partners. It’s the largest-ever Series A round for a Cincinnati startup. http://axios.link/hH8i

• Pleo, a Copenhagen-based provider of prepaid digital and physical cards, raised $56 million in Series B funding. Stripes Group led, and was joined by return backers Kinnevik, Creandum and Founders AS. http://axios.link/oZa8

• Ghost, a Mountain View, Calif.-based startup focused on converting cars to self-driving, raised $32 million in Series C funding. Founders Fund led, and was joined by return backers Khosla Ventures and Sutter Hill Ventures. www.gh.st

• Karat, a Seattle-based startup that conducts technical interviews for prospective employers, raised $28 million. Tiger Global led, and was joined by return backers Norwest Venture Partners and 8VC. www.karat.io

• Algorithma, a Seattle-based, raised $25 million in Series B funding. Norwest Venture Partners led, and was joined by Madrona, Gradient Ventures, Work-Bench, Osage University Partners and Rakuten Ventures. http://axios.link/qgBH

🚑 IsoPlexis, a Branford, Conn.-based developer of single-cell biomarkers for use in oncology, raised $25 million in Series C funding. Northpond Ventures led, and was joined by Spring Mountain Capital, Ironwood Capital, North Sound Capital and Connecticut Innovations. www.isoplexis.com

• Respond Software, a Mountain View, Calif.-based provider of robotic decision automation software for security ops, raised $20 million in Series B funding led by ClearSky Security. http://axios.link/sgdA

⛽ Innowatts, a Houston-based provider of energy monitoring and management software for utilities, raised $18.2 million. Energy Impact Partners led, and was joined by Evergy Ventures and return backers Shell Ventures, Iberdrola and Energy & Environment Investment. http://axios.link/BGIF

• Craftory, a London-based investment firm, acquired a majority stake in Seattle-based direct-to-consumer underwear brand TomboyX, by leading an $18 million Series B investment. http://axios.link/IHye

• Quadric.io, a Burlingame, Calif.-based developer of a supercomputer for autonomous systems, raised $15 million from Denso Corp., NSITEXE and an undisclosed automaker. http://axios.link/pl5M

• Wirepas, a Finnish wireless connectivity platform for industrial IoT, raised €14.4 million from ETF Partners, Inventure, KPN Ventures, TESI and Vito Ventures. http://axios.link/28Rn

• ClickSwitch, a Minneapolis-based provider of account switch solutions for financial institutions, raised $13 million in Series B funding co-led by Commerce Ventures and Point72 Ventures. http://axios.link/EyaO

• Glofox, a Los Angeles-based management platform for fitness studio owners, raised $10 million in Series A funding. Octopus Ventures led, and was joined by Partech, Notion Capital and Tribal VC. http://axios.link/cI7t

• Hydrow, a Cambridge, Mass.-based “Peloton for rowing,” added $7 million to its Series A round (total now $27m, including original tranche led by L Catterton). Investors include Rx3 Ventures, Raptor Group, Wheelhouse and The Yard Ventures. http://axios.link/nP5z

• MainStreaming, an Italian provider of online streaming infrastructure, raised $6 million from Indaco Venture Partners, Sony Innovation Fund and United Ventures. www.mainstreaming.tv

• Seekout, an engineer recruitment platform, raised $6 million in Series A funding. Madrona led, and was joined by Mayfield Fund. www.seekout.io

• Part & Parcel, a New York-based social commerce site for plus-sized women, raised $4 million in seed funding. Lightspeed Venture Partners led, and was joined by Peterson Ventures, Village Global and Poshmark founder Manish Chandra. http://axios.link/kx9i

• Storr, a San Francisco-based P2P retail marketplace, raised $3 million from Spark Capital. www.storr.co

• 4Stop, a German provider of compliance and fraud prevention software, raised $2.5 million in Series A funding from Ventech. http://axios.link/HmpH

Private Equity Deals

Public Offerings

Liquidity Events

More M&A

Fundraising

It's Personnel

Final Numbers

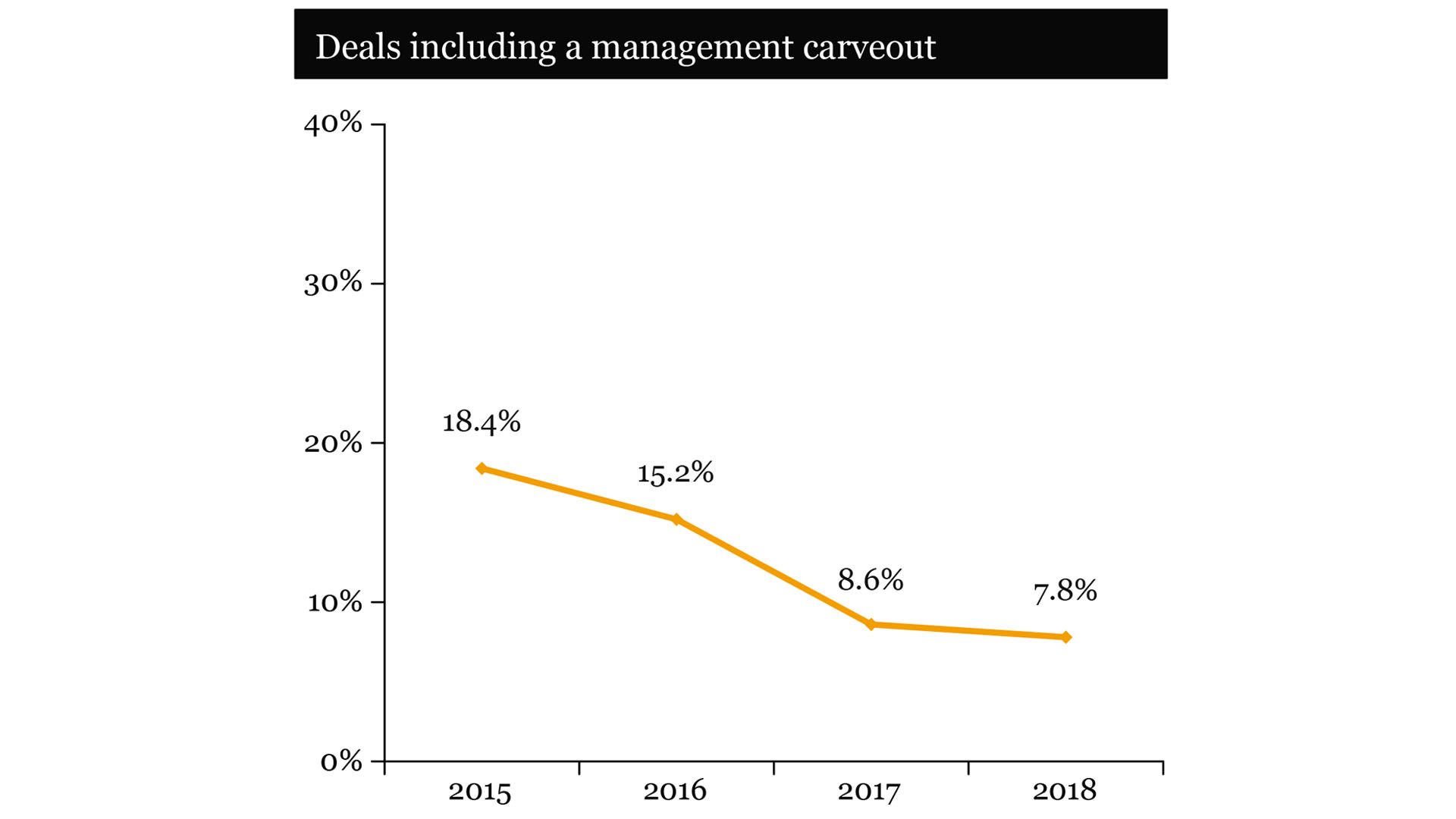

- Definition per SRS Acquiom: "A 'management carveout' in this study is a portion of deal proceeds guaranteed to seller's management when management would otherwise receive little or nothing for their equity ownership due to liquidation preferences. Transaction bonuses, which often differ materially from management carveouts in size and timing of adoption, are not included."

- Bottom line: The decrease in management carveouts seems inversely related to an increase in M&A prices.

Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.