Axios Pro Rata

October 15, 2022

1 big thing: The curious case of 2022's venture fundraising

Illustration: Natalie Peeples/Axios

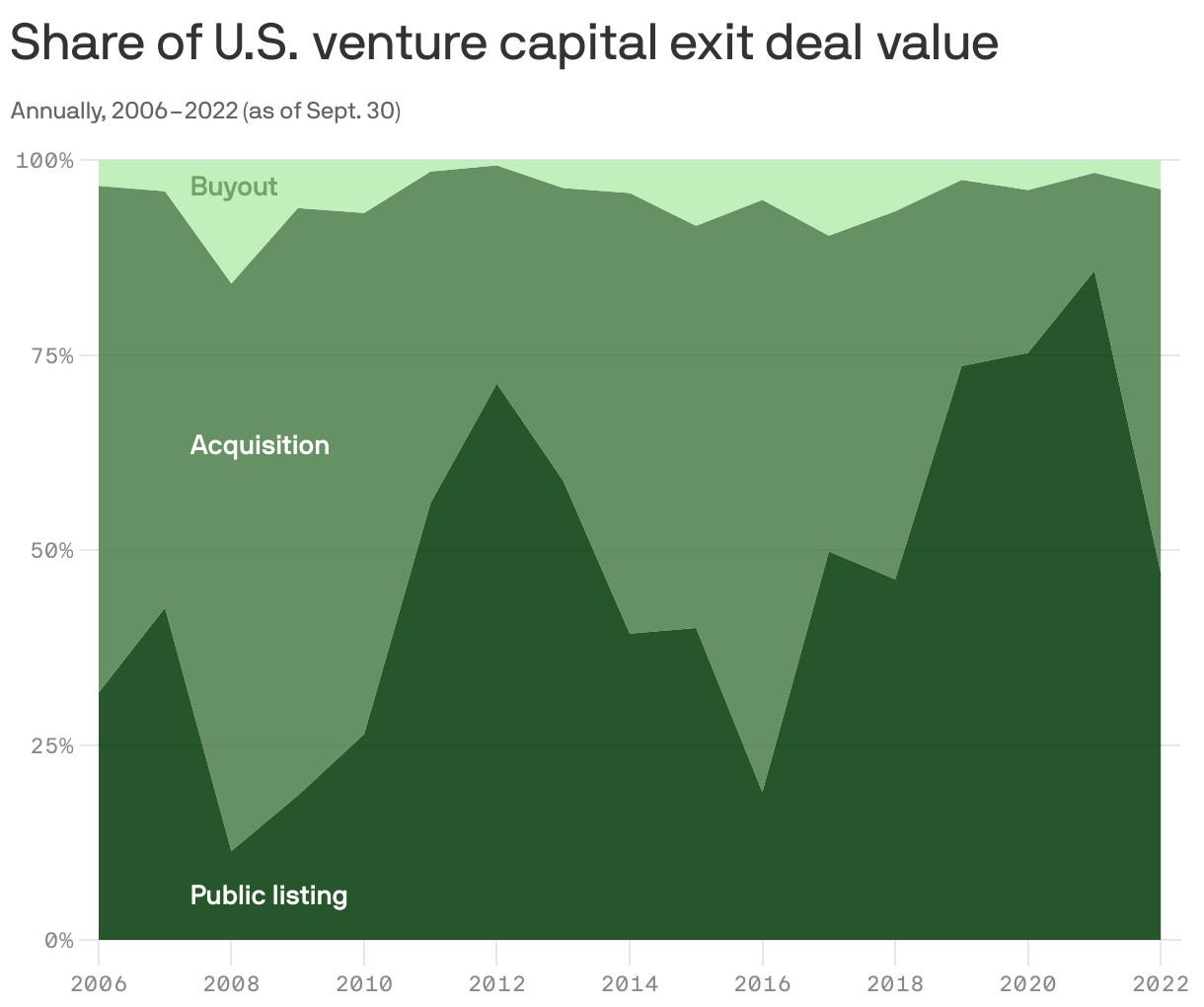

2. 🙏 Unanswered prayers for exits

The data is in, and it has confirmed what everyone's suspected: Venture-backed exits this year are on track to hit a five-year low, per Pitchbook.

Why it matters: Fewer distributions back to VCs' own investors are adding to the ongoing squeeze those investors have been feeling. The market's in turmoil, and many have been stretching their allocations into the asset class during the pandemic boom.

Zooming in: With the IPO window virtually shut most of this year, it's no surprise that almost 50% of exit value so far this year has come from acquisitions.

- The last time acquisitions represented about this portion of exit value was in 2018. Last year, 86% came from public listings, which represented a record 16% of exit counts.

And so far this year, seed-stage startups are the majority of venture-backed companies getting acquired — the highest proportion since at least 2012.

- This suggests that a slew of smaller companies may be opting for a sale amid the more challenging fundraising environment.

Yes, but: One brighter spot is that median acquisition exit value remains above historical figures, at about $100 million. That's up from $66.6 million last year.

- Meanwhile, median public listing and buyout values plunged to $353.6 million and $65 million, respectively (down from $722.5 million and $175 million).

The bottom line: All eyes are on what 2023 holds for exits.

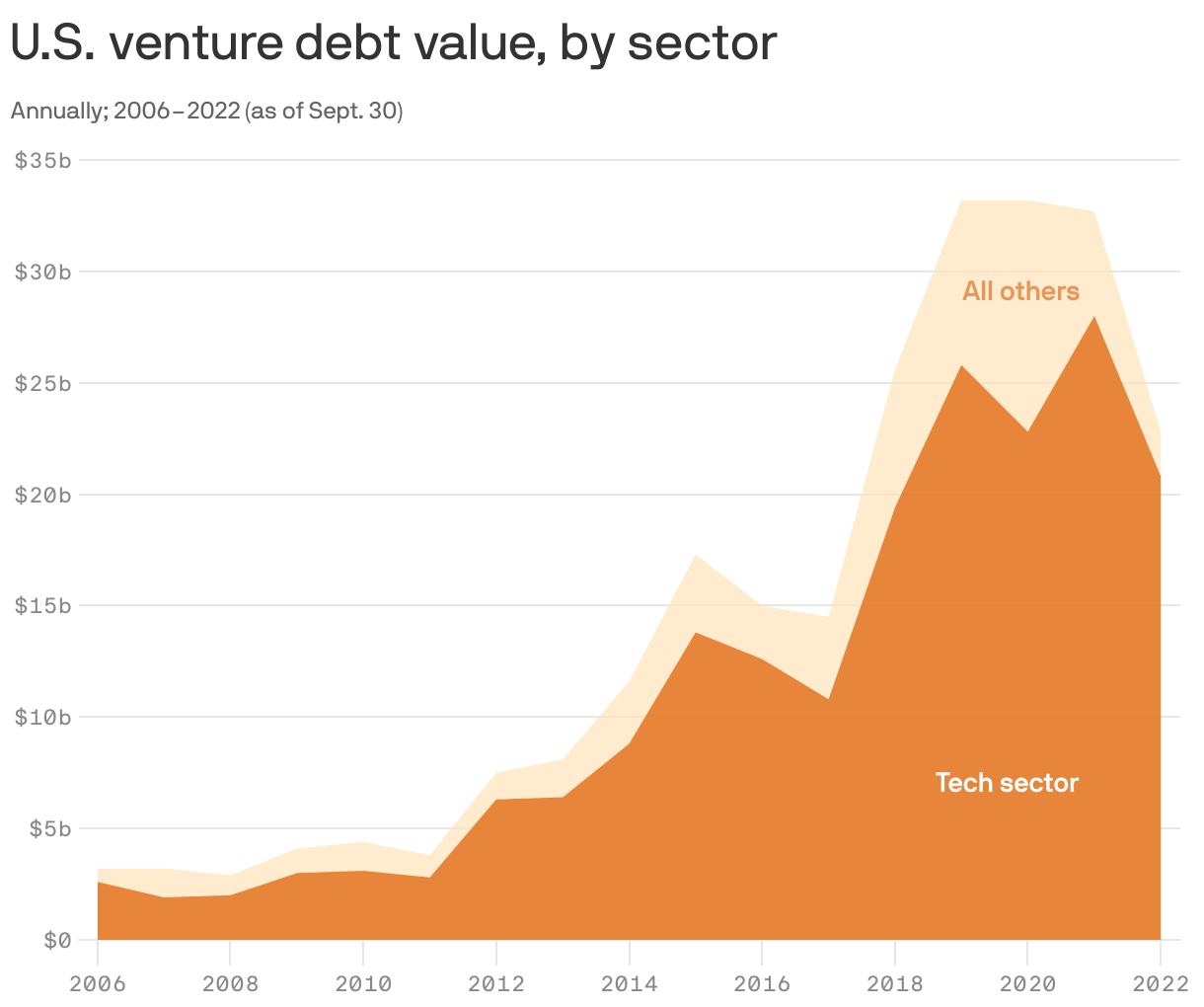

3. 🤔 Who's really venturing into debt...

Venture debt financing so far this year is not as high as the previous three years despite its surge in popularity amid the tighter venture market, per new Pitchbook data.

Yes, but: As expected, most (70%) of the venture debt dollar is going into late-stage companies: Early-stage loans are becoming a smaller portion of overall counts.

Between the lines: Larger, later-stage companies have been the fastest and hardest hit by the public market downturn, as IPO plans evaporated and VCs quickly started to rethink their valuations.

- Debt has become a more popular alternative to provide such companies the cash they need, avoid a down round, and extend their runway as they adjust their fundraising plans.

Bonus: Female founders

📚 Due Diligence

🧩 Trivia

🧮 Final Numbers

Axios Pro Rata

Dan Primack’s briefing on VC, PE & M&A for dealmakers.