Axios Markets

May 21, 2024

1 big thing: The latest attempt to thaw the housing market

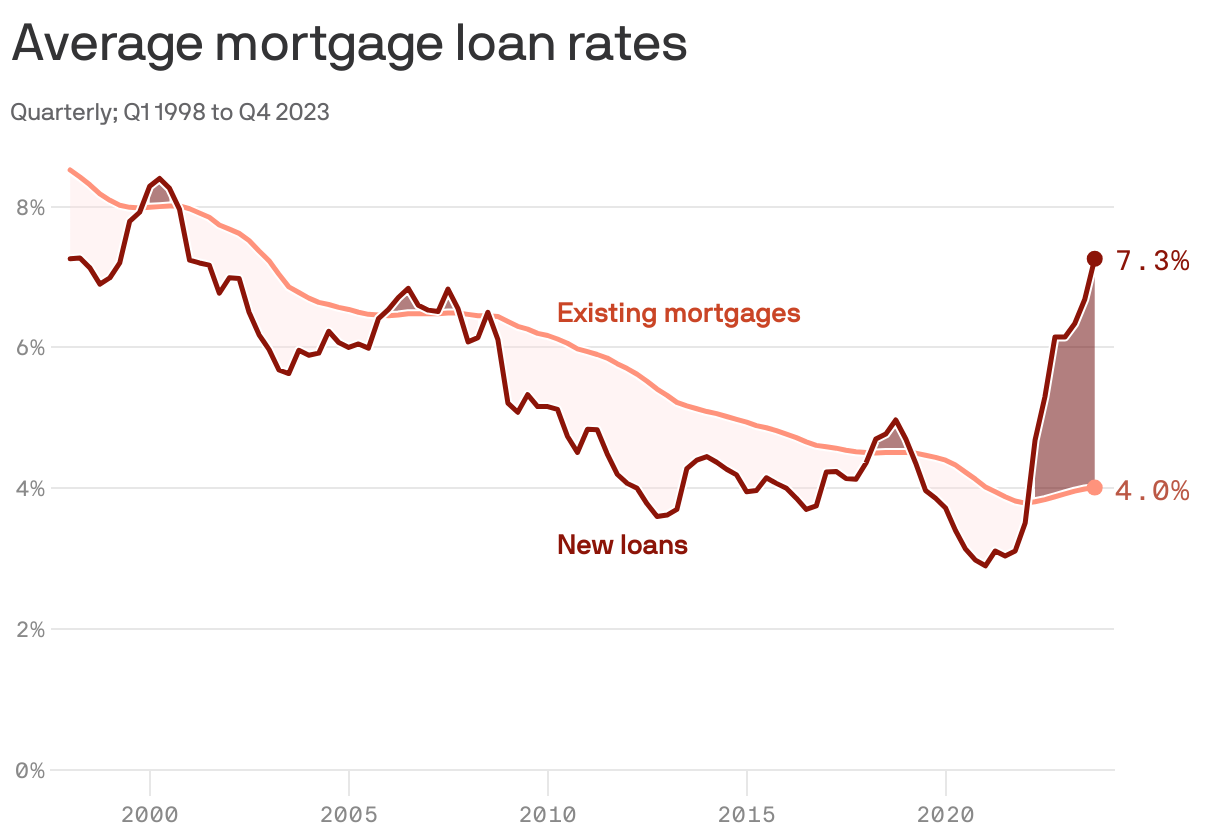

3. Charted: Rate lock

The gap between the mortgage rate you can get on a new loan and the rates most mortgage holders are holding hasn't been this wide in more than 25 years.

- This mortgage rate lock prevented 1.3 million home sales between the second quarter of 2022 and the fourth quarter of 2023, per a working paper from the Federal Housing Finance Agency out earlier this spring.

- The unusual situation is keeping first-time buyers out of the market, and reducing home inventory, which keeps house prices elevated.

The bottom line: "The "stuckness" in the housing market may also be feeding broader frustration with the economy," write Emily Badger and Francesca Paris in the NYT (read their full story).

4. Ivan Boesky, 1937—2024

Axios Markets