Axios Markets

March 11, 2023

1 big thing: Crypto's bedrock implodes

Illustration: Natalie Peeples/Axios

2. How SVB's rescue plan backfired

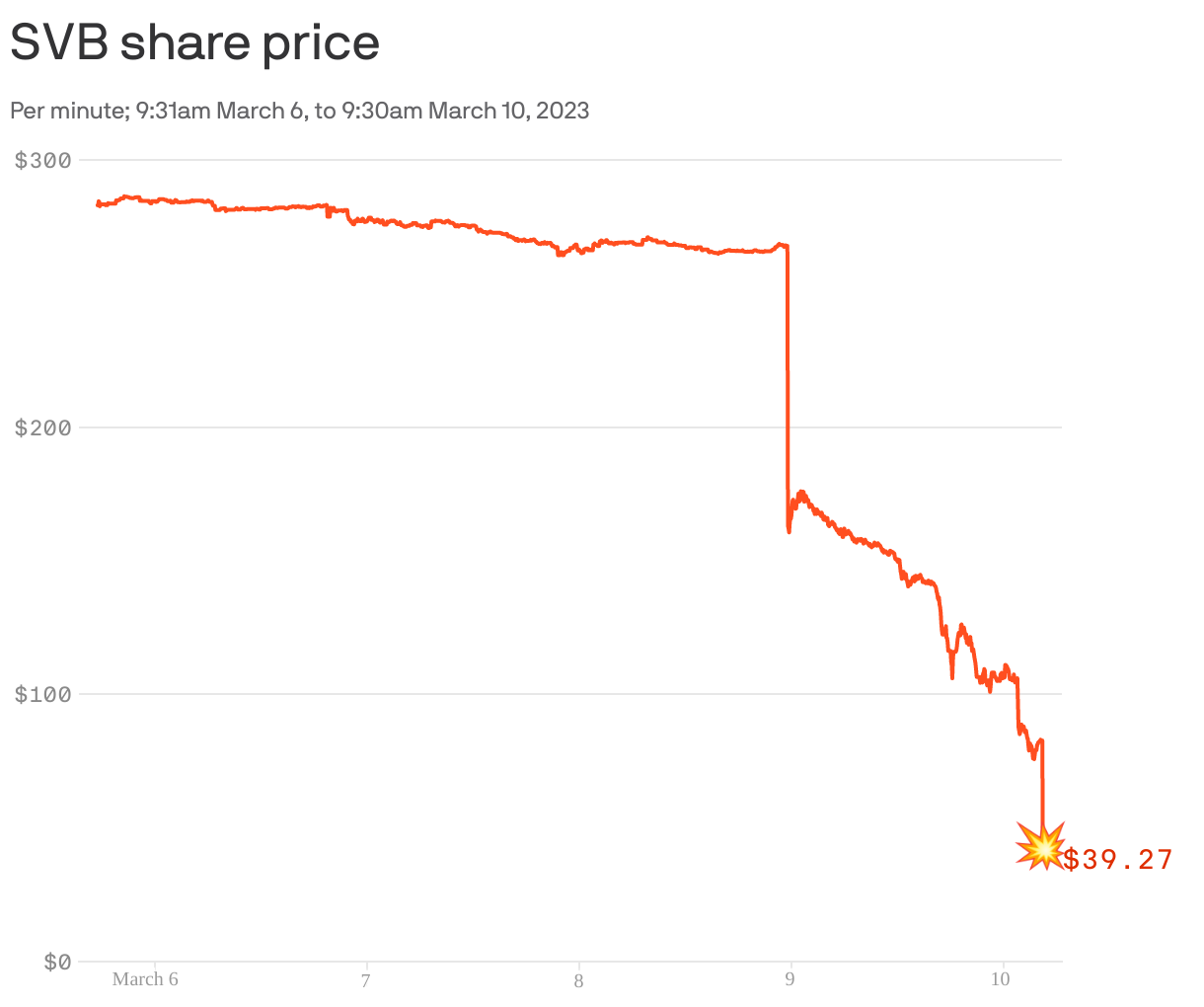

On Thursday morning, Silicon Valley Bank (SVB) had a plan to shore up its balance sheet. Clearly, the plan didn't work.

Why it matters: When SVB announced a plan to raise $2.25 billion of fresh capital on Thursday, it should have put worries about its solvency to rest. Instead, it precipitated a run on the bank, which has now been nationalized and is being run (at least until Monday, and possibly for much longer than that) by the FDIC.

The big picture: The now-defunct capital-raising plan involved issuing two different classes of stock, with pricing meant to take place after the close of trading on Thursday.

- The dilution of existing shareholders was therefore unknown. SVB planned to issue $1.75 billion of new common stock, for instance — which would be 8.75 million new shares at $200 each, or 17.5 million new shares at $100 each, or 44.5 million shares at $39.27, which is the last pre-market price at which the stock traded before it was suspended on Friday morning.

- The lower the share price, the greater the dilution. So when the stock started falling, the deal looked increasingly bad for SVB, putting extra pressure on the stock.

- Eventually, a distinction started being drawn between SVB Financial Group, the bank holding company that also has substantial outstanding liabilities, and Silicon Valley Bank itself. Even if the latter retains real value, the holdco could easily be insolvent.

Between the lines: It wasn't just stock-market investors who were fixated on the SVB share price. Depositors were too, especially given that Silvergate had announced that it was liquidating just one day earlier.

- Because SVB was now in the middle of a securities offering, it considered itself to be in a "quiet period" where it couldn't communicate anything substantive to depositors, investors, or the press beyond what was in its SEC filings.

- So the only real up-to-date information that depositors had about the health and viability of the bank was the plunging share price — and the ever-growing number of stories of other depositors pulling their deposits.

Be smart: Only a small handful of U.S. bank depositors have lost money in a bank failure in living memory, even when they had much more than the FDIC maximum on deposit.

- Still, the cost of moving money to a different bank, even if only temporarily, was tiny — so a lot of people did it. That's a bank run, and a bank run is an existential crisis for any bank.

- SVB CEO Greg Becker then did his bank no favors when he told customers to "stay calm" on a call, while also conceding that they were "starting to panic." Such talk has broadly the same effect on the market as it does on your spouse.

The bottom line: Between dilution worries and bank run worries, the share price just couldn't find a level at which there was any real buying interest — let alone enough buying interest to support a $2.25 billion share sale. So it just kept going down, deposits kept on flowing out, and eventually, on Friday, Silicon Valley Bank became the largest U.S. bank failure since the global financial crisis.

3. When your house funds your retirement

When Americans retire, they often move from expensive areas to cheaper ones. That frees up home equity that can rival or even exceed retirement funds held in 401(k) plans and the like.

Why it matters: People still need a place to live in retirement and rarely take advantage of reverse mortgages to get money out of their homes. Moving somewhere cheaper, however, is much more common.

Be smart: The people buying in expensive cities and states are the younger generations who want to live near good schools or high-paying employers. The cash they're borrowing in the mortgage market is being turned into retirement money for older Americans.

By the numbers: About 80% of Americans over the age of 60 are homeowners, per a new Vanguard report entitled "Home is where retirement funding is."

- By relocating, the median American over 60 can unlock about $100,000 of home equity — and even more if they downsize at the same time. That's a meaningful sum given that the same median American retiree has about $223,000 in financial retirement accounts.

Where it stands: About 25% of U.S. retirees sell their homes and relocate to somewhere cheaper over any given 10-year period, per Vanguard's Kevin Khang, one of the authors of the report.

- That doesn't just free up cash; it also reduces their day-to-day living expenses.

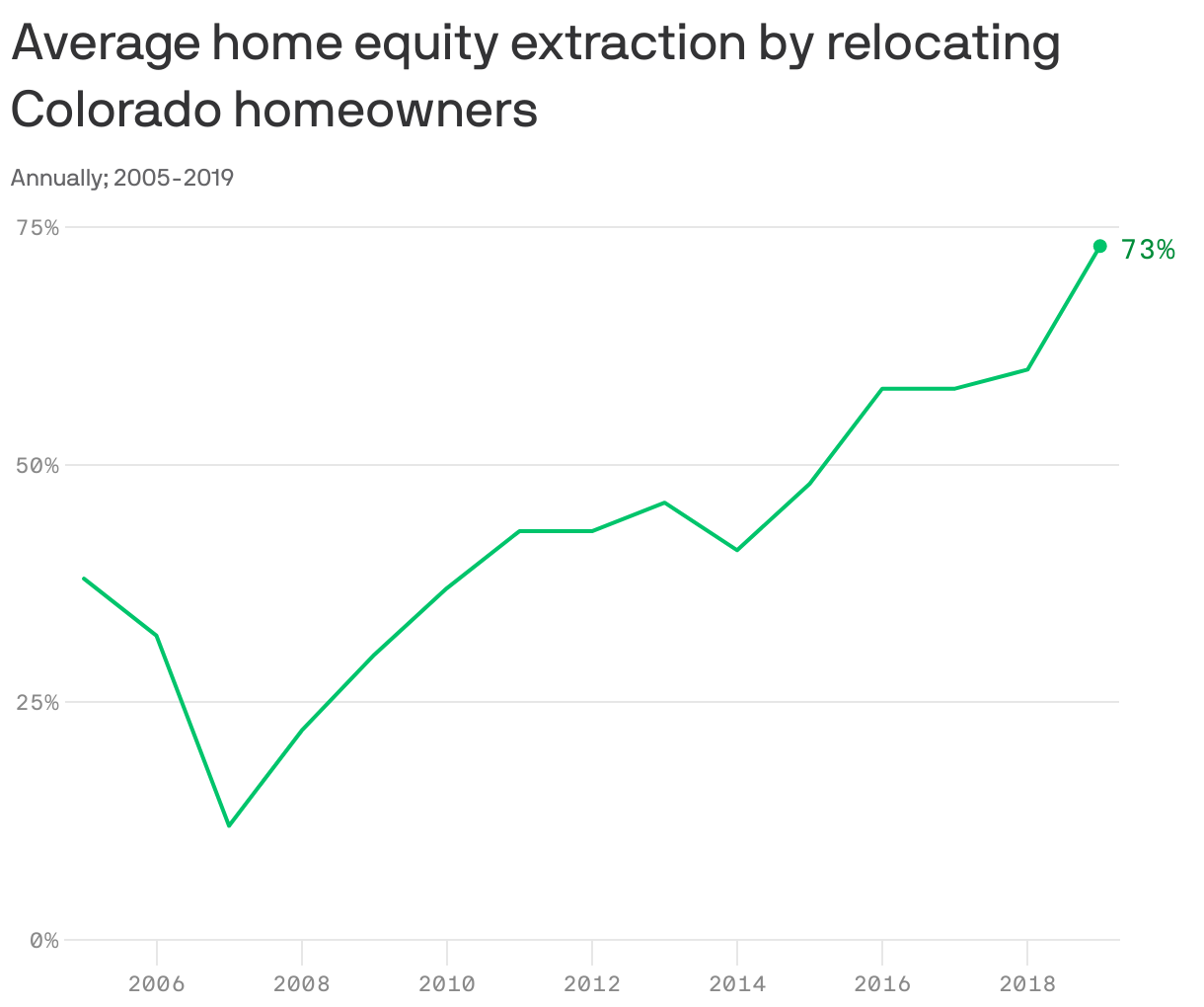

How it works: Let's say a homeowner sells her house in Denver for $600,000, and moves to a similarly-sized house in Florida costing $400,000. That means she's cashing out to the tune of $200,000 — 50% of the value of the new home.

- In fact, in 2019, that ratio averaged 73% in Colorado, up from just 12% in 2007.

- "Given what happened to housing values in Colorado during the pandemic, it's very likely that this number is even higher now," says Khang.

- Other states with lots of cashing-out potential include California (77%) and Hawaii (116%). Importantly, the cashing-out figures include moves within the state, not just moves to a different state entirely.

The bottom line: High housing prices are not the reason why younger Americans move to expensive cities and suburbs. But "when you’re retiring, you’re hyper sensitive to retirement resources," says Khang.

- For older folks who moved to expensive neighborhoods when they were younger, those resources often include their home — which can prove to be a source of substantial liquidity.

4. Building of the week: Inagawa Cemetery Chapel, Japan

Photo: Edmund Sumner/View Pictures/Universal Images Group via Getty Images

Axios Markets

Stay on top of the latest market trends and economic insights