Axios Markets

September 24, 2024

2. Where the uninsured houses are

More than 6 million homeowners live in homes without homeowners' insurance.

The big picture: Most of them are poor: The states with the highest proportion of uninsured homeowners are Mississippi, New Mexico and Louisiana.

- That number will only increase as climate change makes insurance uneconomic in ever-greater swaths of the country.

Zoom in: One of the lessons of the Florida real estate market is that uninsured houses are far from worthless.

- Some 15% of Miami homeowners lack insurance, and some have even seen their property value go up.

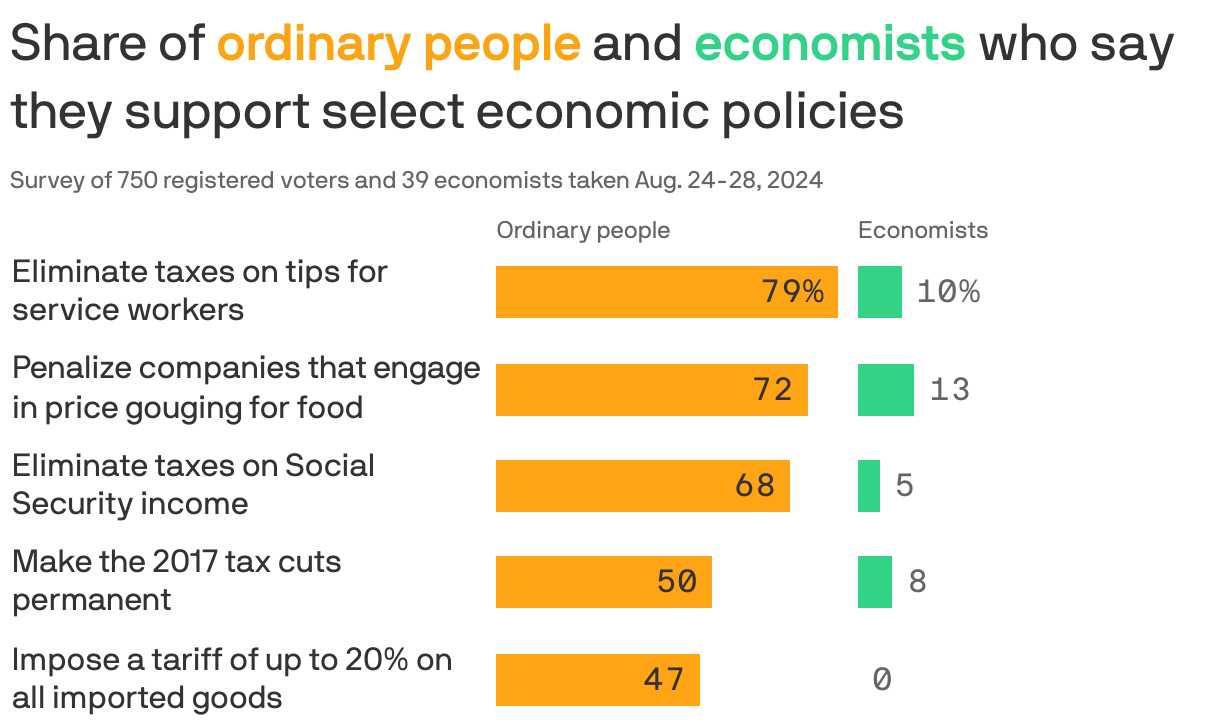

3. The big economic divide

There's another big divide emerging in this election. This time it's between voters and economists, finds new polling from the Wall Street Journal.

Why it matters: In their presidential campaigns, both Kamala Harris and Donald Trump are proposing economic policies that are popular with voters. Mainstream economists, meanwhile, find these ideas "appalling," the Journal notes.

Zoom in: 79% of voters like Trump and Harris's pitch to eliminate taxes on tips. Only 10% of economists support the idea. Many have said it unfairly favors one group of workers, creates incentives to cheat the tax system, and raises deficits.

- None of the 39 economists surveyed by the WSJ approved of Trump's idea to put tariffs on all imported goods.

- Similarly, voters like Harris' idea of penalizing companies for price gouging, but only 13% of economists support it.

For the record: Economists and voters both liked a few proposals: 74% of economists like the Harris plan to provide a $6,000 tax credit to new parents; compared to 67% of voters.

- Neither group particularly favors giving $25,000 to first-time homebuyers.

The big picture: The economist vote doesn't much matter at the moment; it's a tight race. And there are many, many more voters than economists in the U.S.

- Voters certainly haven't listened to all the economists who've been saying the economy is strong over the past few years.

The bottom line: Harris and Trump majored in economics, the WSJ points out, but their political expertise outweighs any lessons from university.

Axios Markets