Axios Markets

January 06, 2024

1 big thing: The 2024 risk that trumps all others

Illustration: Sarah Grillo/Axios

2. Beauty is in the eye of the market

L'Oréal and Estée Lauder are the two largest beauty companies in the world, boasting a market share of 16.1% and 13.6%, respectively. (LVMH is a distant third with 8%.)

Why it matters: The two stocks moved in perfect lockstep with each other from pre-pandemic to the beginning of 2023 — but since then, they have sharply diverged.

- L'Oréal is doing so well that Françoise Bettencourt Meyers, the heiress who controls 35% of the company's stock, is now personally worth $100 billion — the first woman ever to achieve that milestone.

- L'Oréal partners with very successful luxury companies like Yves Saint Laurent and Giorgio Armani; it also owns top beauty companies like Maybelline and Garnier (not to mention the namesake L'Oréal).

- Most importantly for me, it didn't ruin Kiehl's after buying the cult beauty brand — which at the time had just a single store in New York's East Village — for a reported $100 million in 2000.

The other side: Estée Lauder, on the other hand, has struggled of late. It overpaid for Tom Ford, which it acquired at the end of 2002 at a valuation of $2.8 billion, increasing its own indebtedness by $2 billion in the process.

- More importantly, the company's business in the Chinese duty-free island of Hainan imploded, and Estée Lauder found itself sitting on large amounts of unsellable inventory.

The bottom line: There wasn't anything particularly predictable about this sudden divergence in fortunes — although any hedge fund manager capable of seeing the relative-value play this time last year surely made a fortune.

- For the rest of us, this chart simply underscores the importance of diversification.

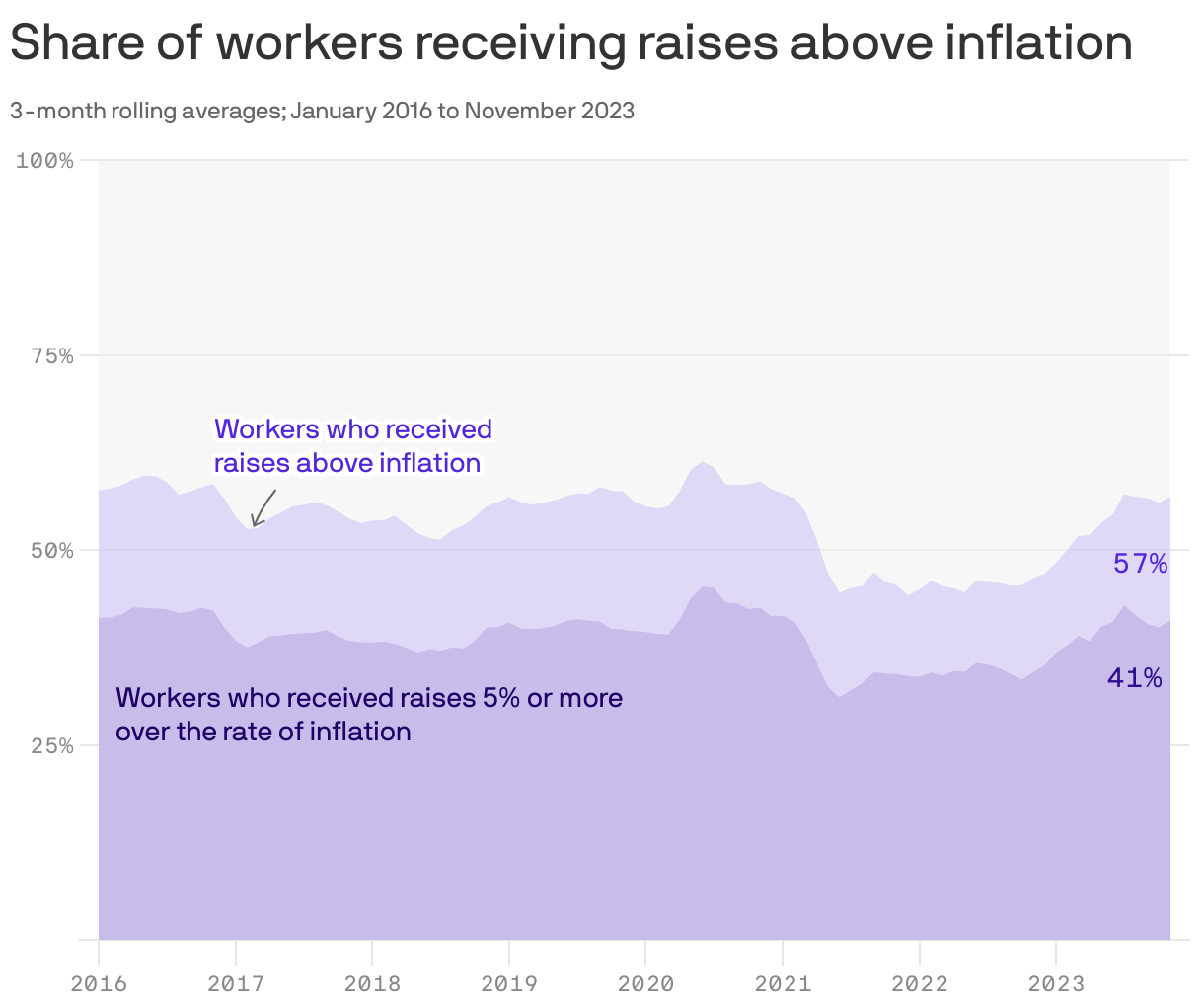

3. Real wage growth returns

Inflation is hated mostly because it erodes the power of your paycheck. But the good news — and the reason why optimism might return to the U.S. in 2024, as I wrote this week — is that real pay hikes have now returned.

Why it matters: As Brendan Duke of the Center for American Progress writes, 57% of workers are making more money now — after adjusting for inflation — than they were a year ago. 41% of us have seen a real wage increase of more than 5%.

- Be smart: Higher wages don't always psychologically offset higher prices. (A $20 cocktail is still expensive even after you've received a big raise.) That's why unhappiness with inflation can linger long after wages have risen to cover those expenses.

The bottom line: Once inflation falls, as it now has, the remaining discontent does tend to diminish as prices that used to cause shock and resentment become normalized. Meanwhile, higher real wages help everyone.

4. Bitcoin ETF frenzy

Illustration: Sarah Grillo/Axios

Axios Markets

Stay on top of the latest market trends and economic insights