Axios Markets

May 09, 2024

2. Another kind of gender gap

For the seventh consecutive year, women reported being less satisfied with their jobs than men, according to a survey from the Conference Board out this week.

Why it matters: Women make up nearly half the workforce, and employers need to attract, hire and retain them.

Zoom in: In almost every aspect of work the Conference Board asked about, from pay to quality of leadership and benefits, women were less happy.

- The biggest divergences were in their feelings about the company bonus plan, opportunities for future growth and health benefits.

The big picture: Considering the long-standing gender gap in pay and other inequities at work, perhaps it's not shocking that there's also a difference in the way men and women feel about their jobs.

Zoom in: The gap between men and women wasn't very wide, and sometimes didn't exist at all, in the first few years after the Conference Board started tracking this in 2011.

- But in 2017 it broadened out. That coincides with the emergence of #MeToo, effectively a nationwide feminist consciousness-raising.

- In the wake of the sexual assault revelations about Hollywood producer Harvey Weinstein, women started speaking up about discrimination and harassment in the workplace — with stories in the press emerging seemingly every day.

Between the lines: With more conversation and attention paid to gender inequality, women were perhaps more likely to see and recognize the sexism they'd previously written off.

Women are also more likely to be juggling family and care responsibilities, too, also dragging down workplace satisfaction.

- The satisfaction gap widened again in 2020 when schools and day cares were closed and many women were taking on even more of this work.

- Even now, women are working longer hours outside their paying jobs on housework and child care, the Department of Labor's deputy director Tiffany Boiman told Axios recently, pointing to data from the American Time Use Survey.

- "This is definitely making them feel squeezed," she said.

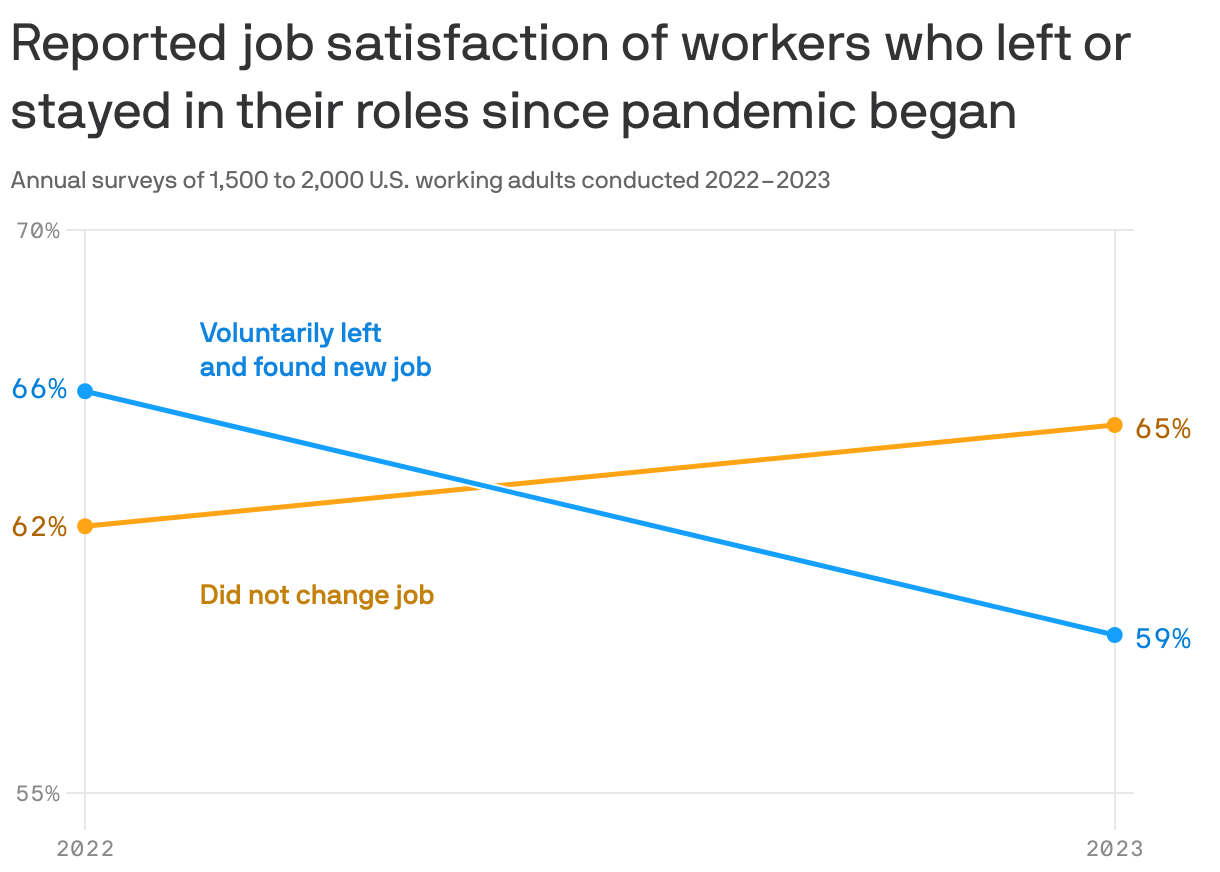

3. Speaking of job satisfaction...

Call it Great Resignation regrets: Workers who switched employers after the pandemic hit were less satisfied with their jobs last year than those who stuck around, per a new survey from the Conference Board.

Why it matters: It's a big change from 2022 when job switchers were more satisfied and may indicate some other simmering issues in the labor market.

Zoom in: Workers who switched jobs after the pandemic were more likely to say they weren't satisfied with their job security.

- Insecurity about employment status is likely more of a concern in 2023, as the frenzy of hiring that spurred the Great Resignation died down.

- And firms are more apt to let go of recently hired workers. As the adage goes: Last in, first out.

The bottom line: The grass isn't necessarily greener on the other side, the Conference Board notes in its report.

Axios Markets