Axios Macro

June 26, 2025

1 big thing: The ratio that explains trade war economics

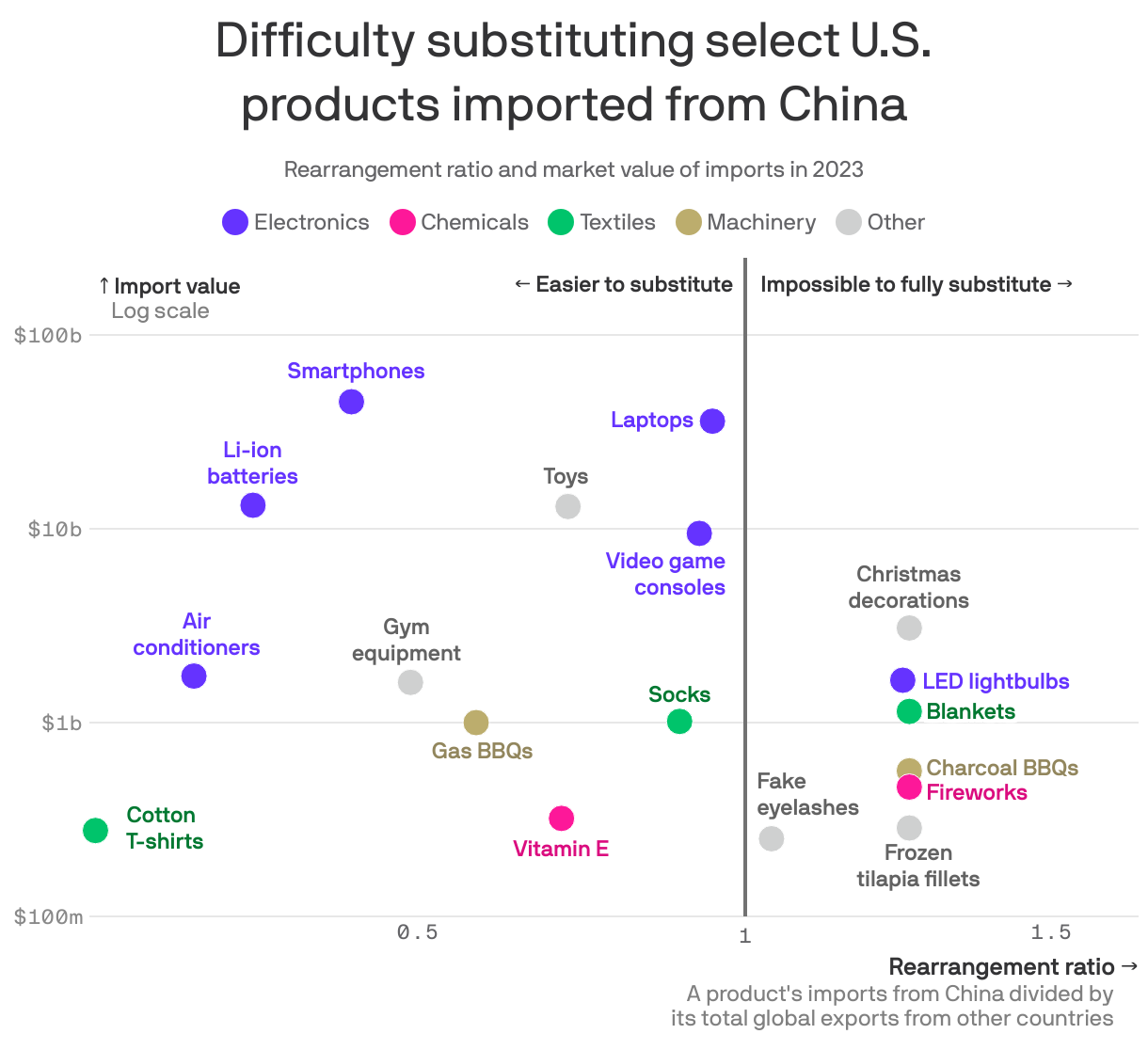

America buys a lot of cotton T-shirts from China — $277 million worth in 2023. We also buy a lot of fireworks — $465 million. But buyers of cotton T-shirts will have a lot more options to avoid the burden of tariffs than buyers of fireworks.

The big picture: That's the implication of revelatory new data from consulting firm McKinsey, which calculated a "rearrangement ratio" for hundreds of different goods the U.S. imports from China.

- The ratio captures in a single number how hard (or easy) it will be for importers to find alternate, lower-tariff suppliers.

- That, in turn, helps answer the question of whether 55% tariffs on Chinese imports are likely, for any given product, to result in higher prices or cause importers to switch up and import from elsewhere.

Zoom in: The ratio captures the value of U.S. imports of a good from China, relative to the total export volume for the product, excluding the U.S. and China.

- So a very low number, like 0.04 ratio for cotton T-shirts, indicates that there are plenty of supplies available on the global market, which allows importers lots of flexibility to shift to producers with lower tariffs.

- A number above 1, like the 1.25 ratio for fireworks, indicates that U.S. imports from China exceed exports for the rest of the world — meaning simply rerouting supply chains is impossible, and importers face high tariffs that they will need to pass on to customers and/or suffer lower profit margins.

A number in between, like the 0.59 ratio for gas grills, suggests a product where importers might be able to find alternate supplies, but could struggle to do so, at least in the short run.

- After all, if U.S. imports from China account for more than half of total available market from the rest of the world, "that's an awful lot of available market to go and capture and try to rearrange," said McKinsey's Olivia White, particularly if those suppliers are locked into existing long-term contracts.

Zoom out: The ratio helps capture the reality that not all products are created equal, and a one-size-fits-all analysis of trade economics doesn't capture what's happening on the ground.

- Goods with low rearrangement ratios are likely to be less affected by the trade war, as importers simply reroute supply chains.

- Consumer goods with high rearrangement ratios tend to be discretionary purchases that account for a low share of total spending (plastic ornaments, for example, with a ratio of 1.11). Importers are likely to pass on high tariffs, and consumers are likely to buy less.

- Business inputs, like industrial pumps and precursor chemicals for pharmaceuticals, are a trickier question, as they tend to be essential for U.S. companies producing higher-value products.

What they're saying: "Imported consumer goods are going to be more discretionary and have higher price elasticity," White, director of the McKinsey Global Institute, tells Axios. "So to the degree that rearrangement is tricky, people might prefer to buy a little bit less."

- To understand the economics of tariffs, she said, "what stood out to me was the degree to which you need to look granularly."

2. Why it would matter if Trump picks a Fed chair early

Axios Macro