Axios Macro

June 23, 2026

1 big thing: The labor market's quiet upgrade

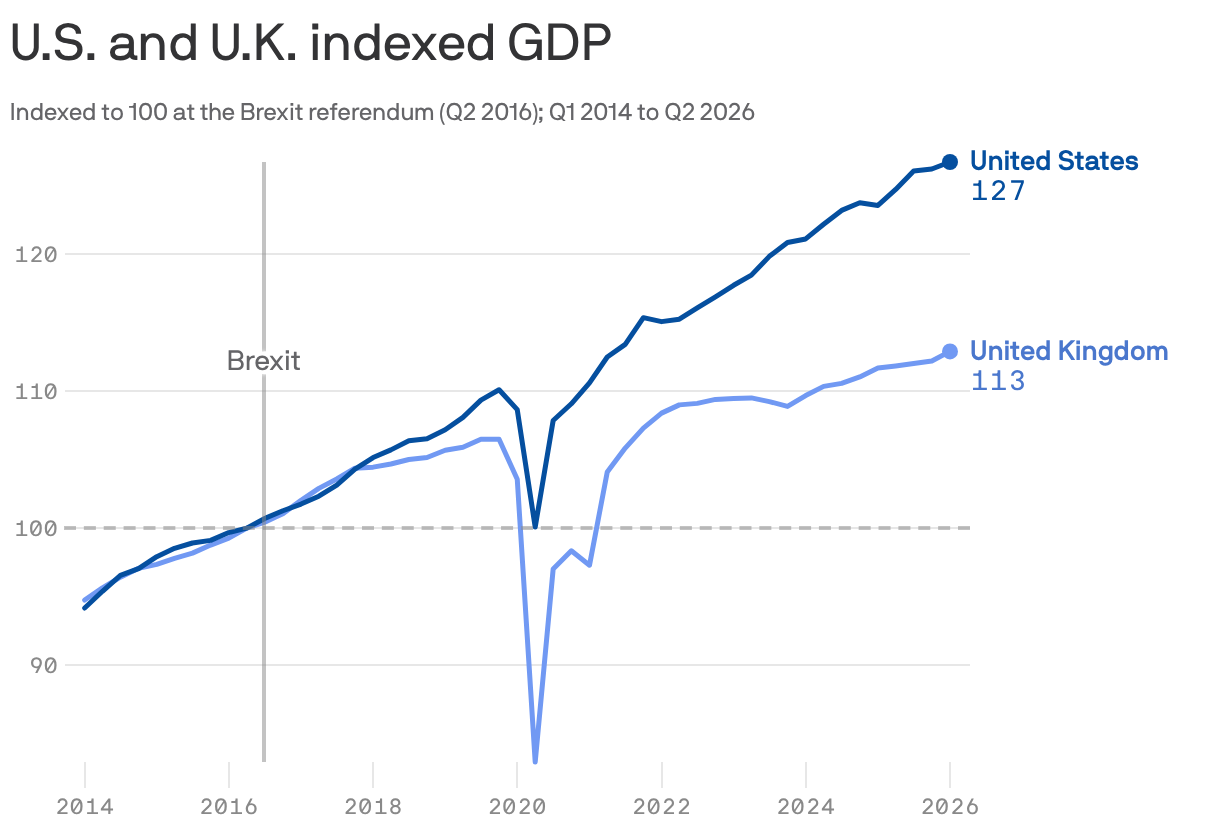

2. The cost of Brexit, 10 years later

Brexit is the real-world test of what happens when a major economy voluntarily raises trade barriers, restricts the free flow of workers and generates years of policy uncertainty — all at once.

- A decade since the vote to leave the European Union, the results are largely in.

Why it matters: The economic drag came from overlapping effects.

- Businesses held off on investment as uncertainty dragged on, executives spent years consumed by Brexit logistics, and the firms most integrated with European markets were often the ones hit hardest.

By the numbers: Since the Brexit referendum, the U.K. economy has grown about 13% — less than half the American pace over the same period, according to FactSet calculations. But even that growth gap might understate the cost of Brexit.

- A paper updated this month from economists at Stanford, the Bank of England, King's College London and the University of Nottingham estimates that by the end of 2025, Brexit had made the U.K. economy between 6% and 8% smaller than it would have been had the country voted to remain.

- The authors estimate business investment was between 12% and 13% lower than the counterfactual, a gap that widened gradually over the full decade.

- Both employment and productivity were as much as 4% lower than they otherwise would have been, the authors estimate.

The intrigue: Economists who predicted Brexit's costs before the vote were roughly right in the first five years — but few understood how much the damage would keep piling up over a full decade, the authors note in the paper.

The bottom line, via Axios' Zach Basu: Britain remains marooned in a low-growth cycle: saddled with trade friction, high prices, strained public services and a hyper-sensitive electorate that tolerates virtually no political failure.

- Go deeper: Britain's lost decade

Axios Macro