Axios Future of Health Care

October 17, 2025

1 big thing: Unsubsidized health insurance is unaffordable

Something big is being missed in the congressional showdown over enhanced Affordable Care Act subsidies: Health insurance premiums are eye-wateringly expensive for the average person without some kind of subsidy.

Why it matters: Health care in the U.S. is expensive, we know, we've all heard it a million times. But most of us don't really feel its full expense, which removes a lot of the urgency to truly address health care costs.

- Whether it's through government tax credits or employer premium assistance, most Americans with private health insurance don't pay the entirety of their premium.

- But we're all paying the freight one way or another, either through taxes or paycheck deductions.

State of play: The past few weeks have been full of dire warnings from Democrats and their allies about what will happen if the enhanced ACA subsidies from the pandemic era are allowed to expire at year's end.

- The gist is that millions of Americans will have sticker shock when they're exposed to more or all of the premium cost, and many will ultimately opt out of buying coverage. That's all probably true.

- Of course, allowing the enhanced subsidies to expire would just make the law's structure revert to its original state.

- And that's why some savvy Republican-aligned commenters are asking if that means the ACA is broken, or if the original version was unworkable.

Reality check: Premiums have gone up — a lot, in some cases. But that's not unique to the ACA marketplace, and premiums are even pricier in the employer market.

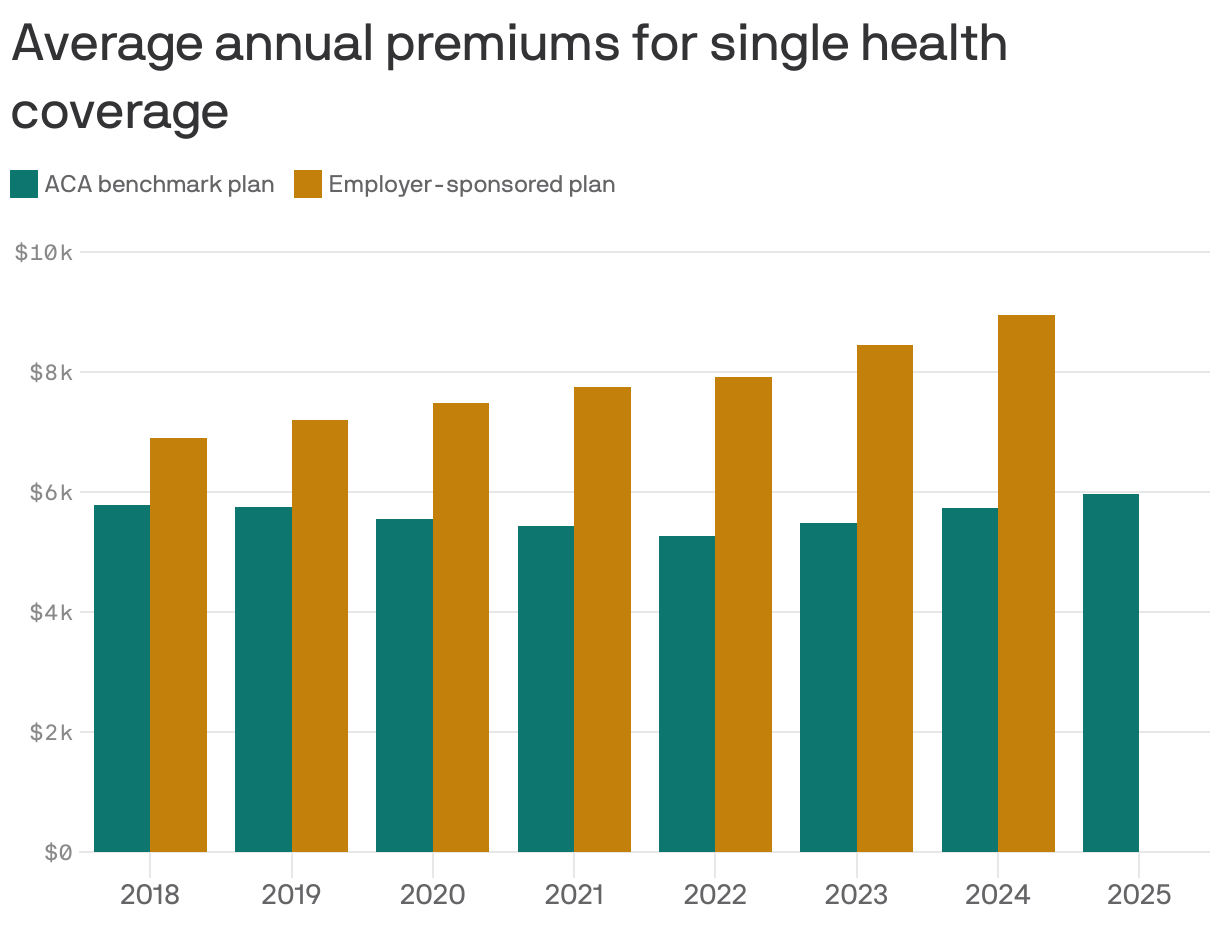

By the numbers: This year, the average premium for a benchmark ACA plan is $497 a month, or nearly $6,000 a year, according to KFF.

- The average employer-employee premium for single coverage was $8,951 last year, also according to KFF.

- The average premium for family coverage was a whopping $25,572.

Let's do some math. Without any form of subsidization, a single person making $60,000 would spend 10% of pretax income on an ACA plan, and 15% on an employer plan.

- Now let's say that $60,000 income is supporting a family of four. The average premium without subsidies would cost that family 43% of its pretax income.

- The median U.S. family income, according to the Census Bureau, was $83,730 in 2024. Health insurance premiums would be 31% of pretax income.

Between the lines: The definition of "affordable" is obviously very subjective, but it seems safe to say that some of these numbers — especially for families — aren't meeting it.

What we're watching: Open enrollment is coming, and people with ACA coverage aren't the only ones facing premium increases.

- Health benefit costs are expected to increase 6.5% per employee in 2026, according to Mercer. Many employers are planning to limit premium increases by raising out-of-pocket costs for employees.

- On average, ACA marketplace plans are raising premiums about 20% in 2026, according to KFF.

- How much of that increase gets passed on to enrollees will depend on whether the enhanced subsidies are extended, but the premium increases are partially due to insurers having accounted for the subsidy expiration.

The bottom line: Policymakers have two broad options: They can keep fighting over who pays for what, or they can do bigger, systemwide reform.

- If you're waiting for the latter, don't hold your breath!

2. Why this drug deal is different

Axios Future of Health Care