Axios Crypto

July 22, 2022

🧿 1 big thing: Regulation by enforcement

Illustration: Sarah Grillo/Axios

🙈 2. The nine ill-fated tokens

Illustration: Eniola Odetunde/Axios

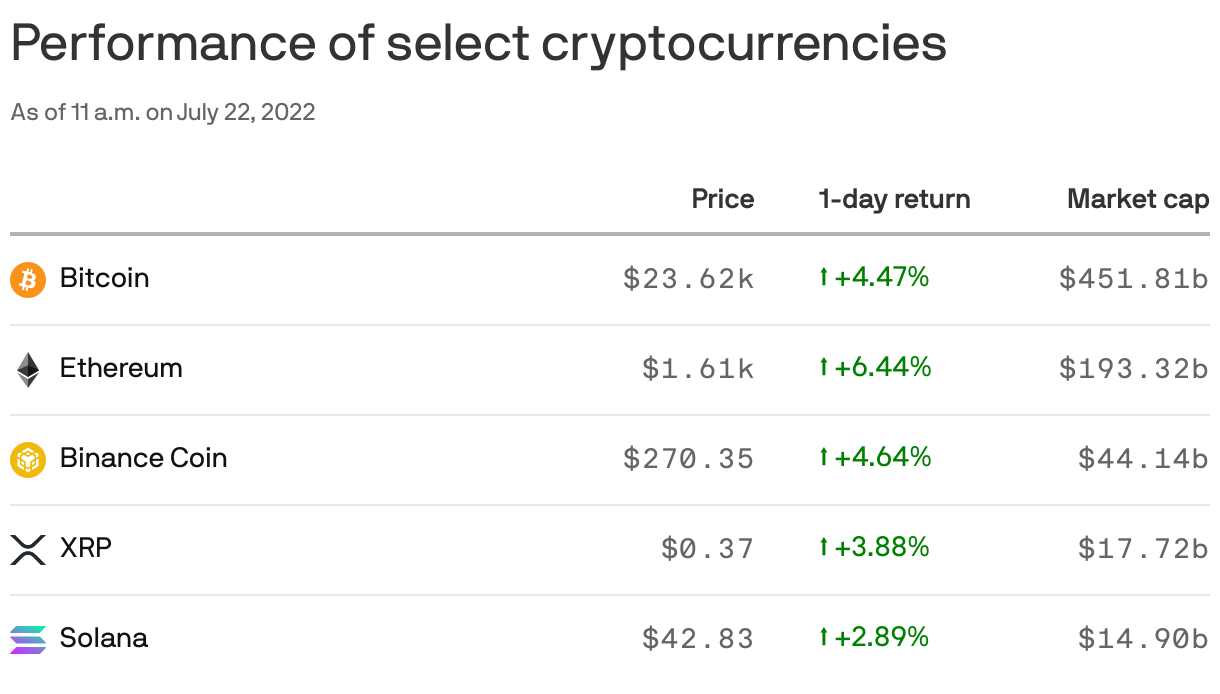

🧊🧊 3. Two cases, one glaring issue

Illustration: Maura Losch/Axios

So there are two cases open after yesterday's token drama, Brady writes, hinging on trades that occurred between June 2021 and April 2022, across 10 Coinbase announcements of new token listings.

- In the first, the Department of Justice alleges three people committed wire fraud by trading on information stolen from Coinbase, information about which tokens it would list on its cryptocurrency exchange.

- In the second, the SEC brings civil charges for "insider trading in certain crypto asset securities," under the Securities Exchange Act of 1934.

What they're saying: "Our message with these charges is clear: Fraud is fraud is fraud, whether it occurs on the blockchain or on Wall Street," U.S. Attorney Damian Williams said in a statement.

- Sources with knowledge of the matter explained to Axios that the wire fraud statute is quite broad.

- The fact that the defendants were using stolen information to make money at the expense of others in the market should be enough to persuade a court it was wire fraud.

Of note: Whether or not a token is a security has no impact on the DOJ indictment.

Why it matters: Because of Coinbase's dominant position in the most important cryptocurrency market in the world, tokens make a strong uptick in value when they get a listing there.

- Which makes knowledge of such a listing extremely powerful. That's why Coinbase employees are expressly forbidden to trade on that information.

- The accused trio is alleged to have made a little over a million dollars front-running the listings.

Details: The key defendant is a former Coinbase product manager, Ishan Wahi, 32, of Seattle, who was assigned to the asset listing team.

- He's alleged to have informed his brother, Nikhil Wahi, 26, also of Seattle, and a friend, Sameer Ramani, 33, of Houston, of which tokens to purchase ahead of listings.

- The Wahis have been arrested. Ramani remains at large.

Zooming out: The case follows much the same mechanism as the one against Nate Chastain, who was arrested in early June in connection with trading on NFTs ahead of them being showcased on OpenSea.

- In each case, employees benefited from knowing in advance which assets would get the spotlight from a major platform.

Twitter was key in both cases. The DOJ credits a Twitter user with spotting what looked like insider trading. They cited what appears to be a tweet from Cobie (Jordan Fish, formerly known as Crypto Cobain).

- 👀 Coinbase security replied to Cobie that it was already on the case.

The intrigue: Most of the SEC's complaint is given over to making the case that the aforementioned nine tokens qualify as securities.

- "The DOJ did not charge securities fraud. No assets listed on our platform are securities, and the SEC charges are an unfortunate distraction from today’s appropriate law enforcement action," Coinbase wrote in a blog post update yesterday.

The bottom line: "We are not concerned with labels, but rather the economic realities of an offering," Gurbir Grewal, director of the SEC’s Division of Enforcement, said in a statement.

🧑🚀 4. Culture hash: A little too real

Screenshot: @pt (Twitter)

Top coins

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.