Axios Crypto

May 08, 2023

🇧🇸 1 big thing: Updating rules in the Bahamas

Illustration: Shoshana Gordon/Axios

🤡 2. Charted: Bitcoin fees

Bitcoin fees are crazy at the moment, Brady writes, and they really spiked this weekend.

State of play: The world's oldest blockchain is seeing an uptick in demand right now for exotic use cases, making it much more expensive for regular users as well.

Driving the news: Binance actually shut down bitcoin withdrawals twice yesterday due to the congestion.

- Based on what Binance said about the pauses, it sounds like its systems were proposing fees that were too small for miners to want to pick up under the current load.

- Meanwhile, rival OKX made sure to let everyone know it was having no trouble.

Be smart: As a decentralized network, users have to pay the network itself for it to do anything, because no one entity is paying to run it (like everything else people use on the web).

- Sending a transaction causes the Bitcoin network to do a little bit of calculation. In fact, every computer on the network has to run that calculation, so to pay for that work each transaction comes with a fee.

- Bitcoin doesn't care what you're doing or how much bitcoin you're sending. It's just a question of how much work you're asking it to do.

- Transaction fees are set via an auction. The more people try to squeeze into blocks, the more expensive they get.

Between the lines: Until the Ordinals project came along, there wasn't an excess of demand. Lots of blocks would be finalized without using all the data available. Not lately though.

- Now people are trading Meme coins and NFTs that run on Bitcoin, and it's getting a bit crazy.

- As of this writing, over 400,000 transactions are waiting to become official. 😮

Flashback: The last time they were this high was May 2021 (before this newsletter existed).

- The highest they have ever gotten was in April 2021, when sending a transaction could cost over $60.

For newbies: The high fees have no impact on trading fees on exchanges like Coinbase or Huobi or Binance. Exchanges operate off-chain.

- The fees on a blockchain only matter to exchange users if they want to withdraw a cryptocurrency to hold in a personal crypto wallet.

🖖 3. The weekend chain split on Bitcoin

Illustration: Natalie Peeples/Axios

🚴 4. Catch up quick

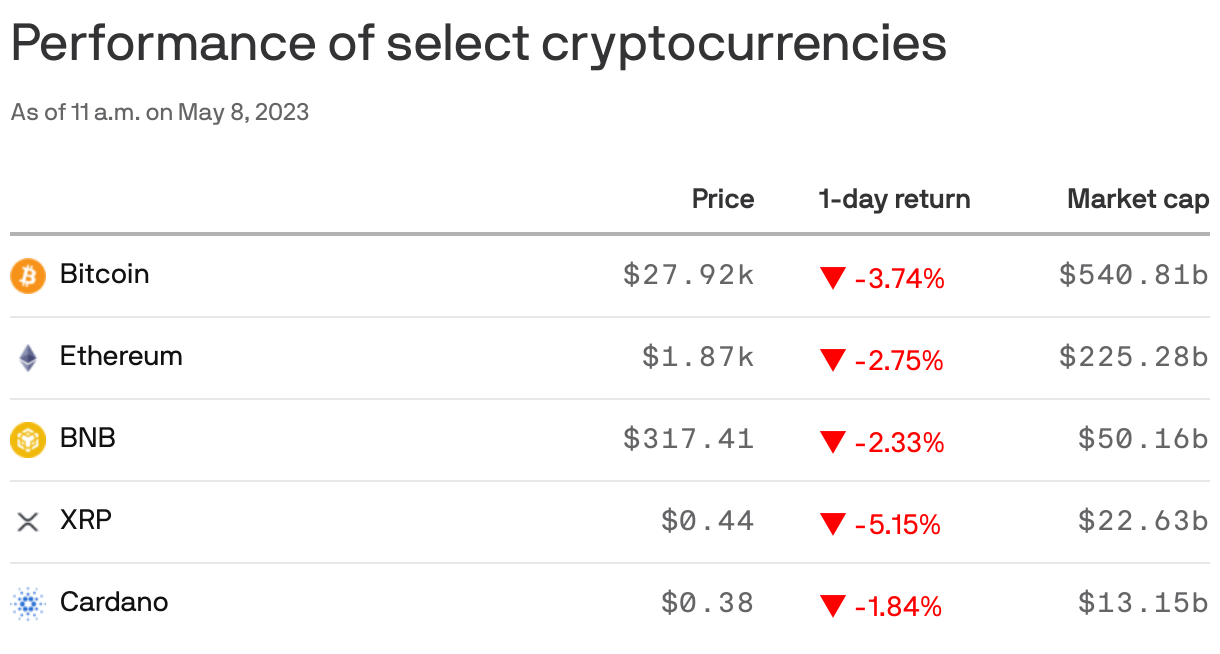

Top coins

🫤 5. Culture hash: Satoshi who?

Screenshot: @udiWertheimer (Twitter)

Axios Crypto

Brady Dale covers crypto and blockchain impacts on markets and regulation.