Axios Capital

June 09, 2022

1 big thing: The disutility of economic forecasts

Illustration: Aïda Amer/Axios

2. Picking good forecasters is impossible

Illustration: Annelise Capossela/Axios

3. When economic forecasting goes horribly wrong

Photo: Chris Ratcliffe/Bloomberg via Getty Images

4. How stock trading might change

Illustration: Megan Robinson/Axios

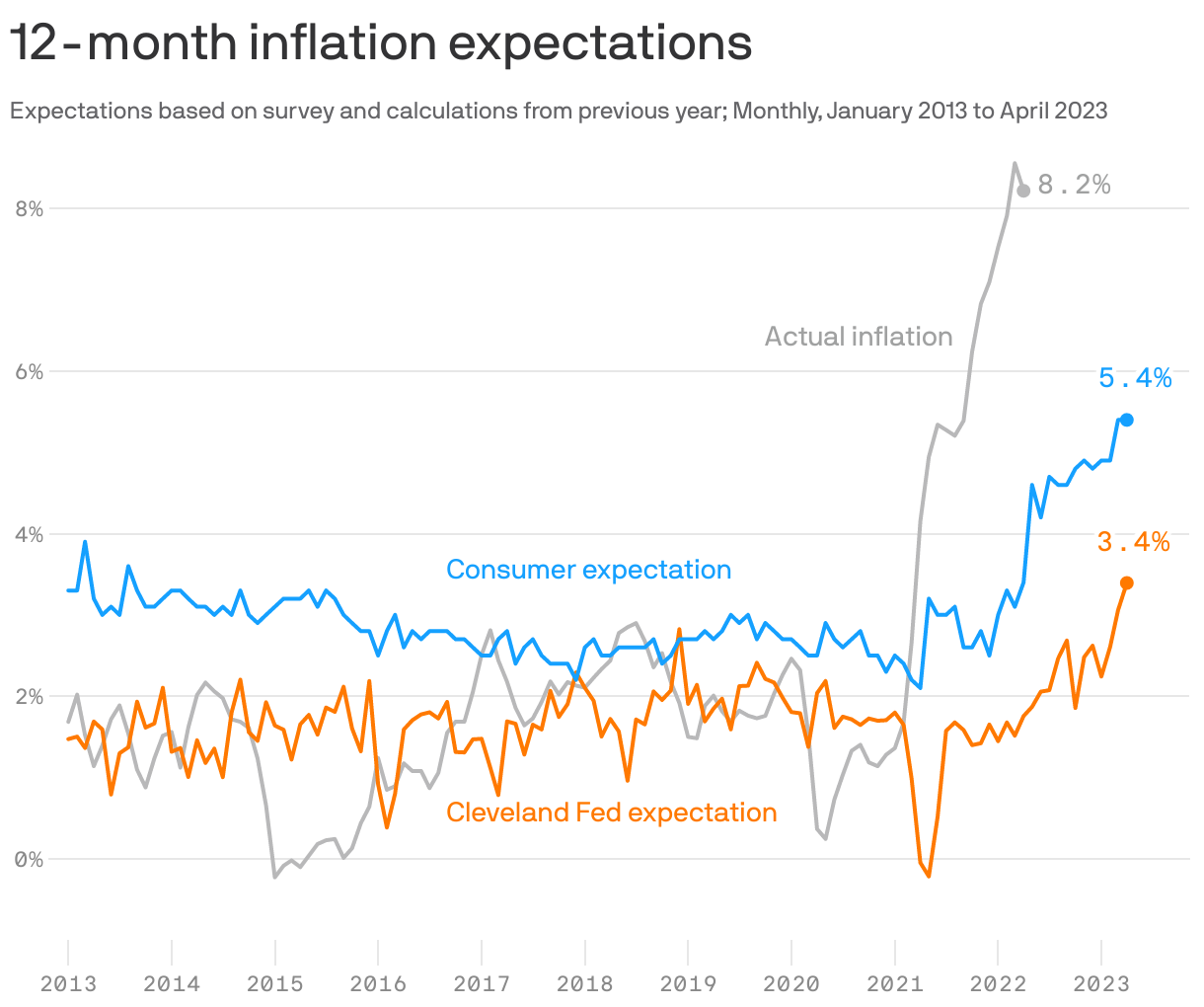

5. How inflation defied forecasts

Americans are congenitally pessimistic when it comes to inflation — surveys of where consumers expect inflation to be in a year's time generally show levels a point or two above the broad market consensus.

Why it matters: Historically, inflation has almost always come in significantly lower than we expected. But when it finally did spike, it rose much higher than even the pessimists had predicted.

What's next: Markets expect that consumer prices in a year's time will be 3.6% higher than they are today, per the Cleveland Fed. Consumers expect they'll be 5.4% higher.

- Both numbers are well below the current rate of inflation, which means that for the first time in many years, America expects inflation to fall rather than rise.

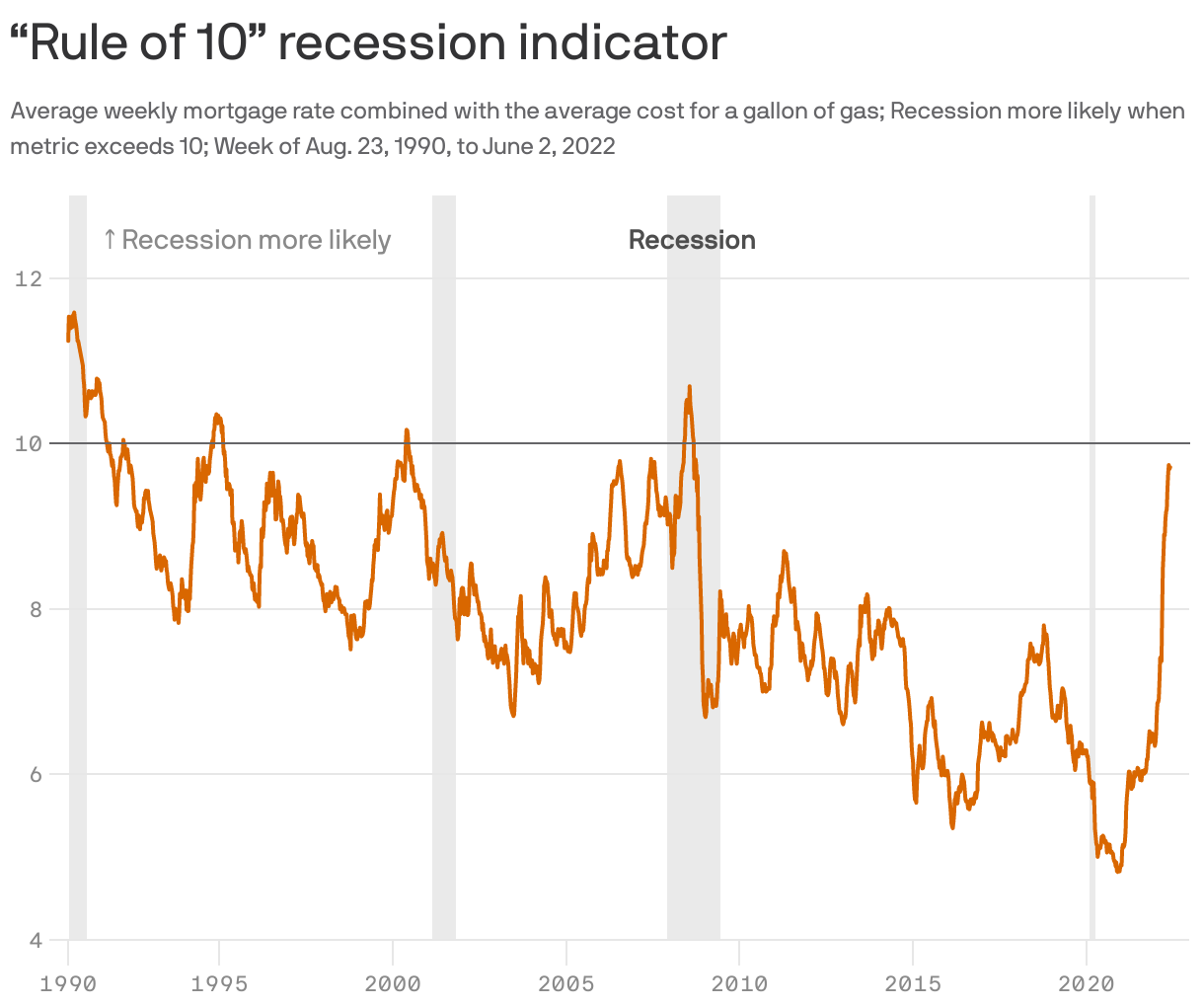

6. Recession indicator of the week

7. The executive chairman lives on

Illustration: Eniola Odetunde/Axios

8. Bringing fiscals back

Screenshot: Knotwords

9. Building of the week: Museum of Ethnography, Budapest

Photo: Attila Kisbenedek/AFP via Getty Images

Axios Capital

Learn about all the ways that money drives the world