Axios Capital

February 10, 2022

Situational awareness: Before the NFL season began, the Cincinnati Bengals faced 150-1 odds to win it all. If they prevail on Sunday, they would be tied with the 1999 St. Louis Rams for longest-odds Super Bowl winner. 🏈 🎰

💰 In today's edition we unpack the hot controversy around a Fed nominee, think about financial regret, and study beer economics, all in 1,506 words, a 6-minute read.

1 big thing: Big clash over access to financial plumbing

Illustration: Maura Losch/Axios

A long-simmering question is coming to a boil: Which companies should (or shouldn't) get access to the core of America's financial plumbing?

- Stick with me here, this may seem technical but it's actually pretty juicy — and it's putting extreme pressure on the Federal Reserve, a key Biden nominee, and many ambitious fintech firms.

Why it matters: The long term economic stakes are huge. If America gets these decisions wrong, it will mean a higher risk of financial crises (if the rules are too loose) or a loss of innovation and competitiveness (if they're too tight).

The details: Banks hold a "master account" with their regional Federal Reserve bank. This allows them to deposit funds electronically backed by the one entity that controls the creation of dollars — the safest possible place.

- It also allows them access to FedWire, the system through which banks transfer money to each other, quickly and with minimal cost.

The issue: A bigger range of companies want access to this preferred status at the core of America's financial system. The Fed's Board of Governors has been reluctant to grant it, fearful that giving untested, lightly-regulated firms access to master accounts will create unintended consequences.

Consider The Narrow Bank: TNB was launched in 2017 as a novel sort of bank. The idea was that large institutions could deposit money in TNB, which in turn would keep all its assets as reserves at the Fed — not lend them out to borrowers like a normal bank.

It would be a super-safe way for large institutions to park their cash. But Fed officials have worried it could also risk financial stability by incentivizing runs on more conventional banks that take on more risk — lending money to consumers and businesses — and are thus more susceptible to losses.

- In a crisis like 2008, for example, depositors might pull money from traditional banks to park it in the safety of TNB.

- The Federal Reserve Bank of New York slow-walked TNB's application for a master account, and the TNB's lawsuit on the matter was dismissed by a federal judge. It now exists in regulatory purgatory.

Other courts have found differently, including an appeals court ruling that the Kansas City Fed must give access to a credit union serving the marijuana industry. Put a pin in that.

More recently, financial technology startups — notably "Special Purpose Depository Institutions" focused on cryptocurrency — are seeking access to Fed master accounts that would allow them to connect more deeply into core U.S. financial infrastructure.

The Fed has resisted, because, as chair Jerome Powell said at a hearing last month, "we want to be very careful because they are hugely important from a precedential standpoint."

- The Fed's concerns are less a specific theory of how startups having access to Fed accounts could destabilize the financial system, and more rooted in a sense of caution and a desire to understand what might go wrong if nontraditional companies had access.

- He added, "We start granting these, there'll be a couple of hundred of them very quickly, and we have to think about the broader safety and soundness implications."

2. Sarah Bloom Raskin's master account mess

Sarah Bloom Raskin at her confirmation hearing. Photo by Ken Cedeno-Pool/Getty Images

The master accounts controversy could now determine the future of President Biden's nominee to be the Fed's top bank regulator.

- Sarah Bloom Raskin, who awaits Senate confirmation to become vice chair of the Fed for supervision, helped an unconventional financial firm attain the master account status that many other firms covet.

Driving the news: Reserve Trust Co., where Raskin served on the board of directors after her time in senior roles at the Fed and in the Obama Treasury Department, obtained a Fed master account through the Kansas City branch of the central bank in 2018.

- The company advertises itself on its website as "the first fintech trust company with a Federal Reserve master account."

- Republican Senate staff said that the Federal Reserve Bank of Kansas City confirmed to them that Raskin called the bank on behalf of Reserve Trust. In written testimony, Raskin said she does not recall making the call.

The Kansas City Fed, in a public statement on the matter, said it is routine for the bank to communicate with an organization seeking an account, including with "its management (including directors), public officials and any relevant federal or state regulatory counterparts."

- Raskin sold stock in the company she received for her board service for $1.47 million in late 2020, according to filings.

To Senate Republicans, this is a classic story of the Washington revolving door, and Raskin is guilty of using her connections obtained as a top official to cash in. They view her responses on this question as disingenuous.

- "Even though Ms. Raskin claims not to recall whether she lobbied the Fed on behalf of Reserve Trust, she asserts, without any sense of irony, that if she did do it, it was done so ethically and entirely above board," said Amanda Thompson, spokesperson for Senate Banking Committee Republicans.

Raskin allies say there is nothing unusual about her actions. "I owned a bank," tweeted Cam Fine, former president of the Independent Community Bankers of America.

- "It is normal and routine for board members to help their institutions-in fact it is expected! There is nothing to see here, despite the efforts of those who wish Sarah Bloom Raskin ill!”

Worth noting: Raskin has agreed to abide by an ethics request from Sen. Elizabeth Warren (D-Mass.) to recuse herself from employment by the financial industry for four years after the end of her Fed service, if confirmed.

Yes, but: There is a broader question in play around whether a Fed regional bank is legally obligated to provide access to companies who meet basic legal standards.

- The Board of Governors in Washington has proposed regulatory guidance that would give it wide latitude to restrict access to the master accounts.

The bottom line: Regardless of whether Raskin is confirmed, the question of how much access the Fed should give novel financial firms remains open.

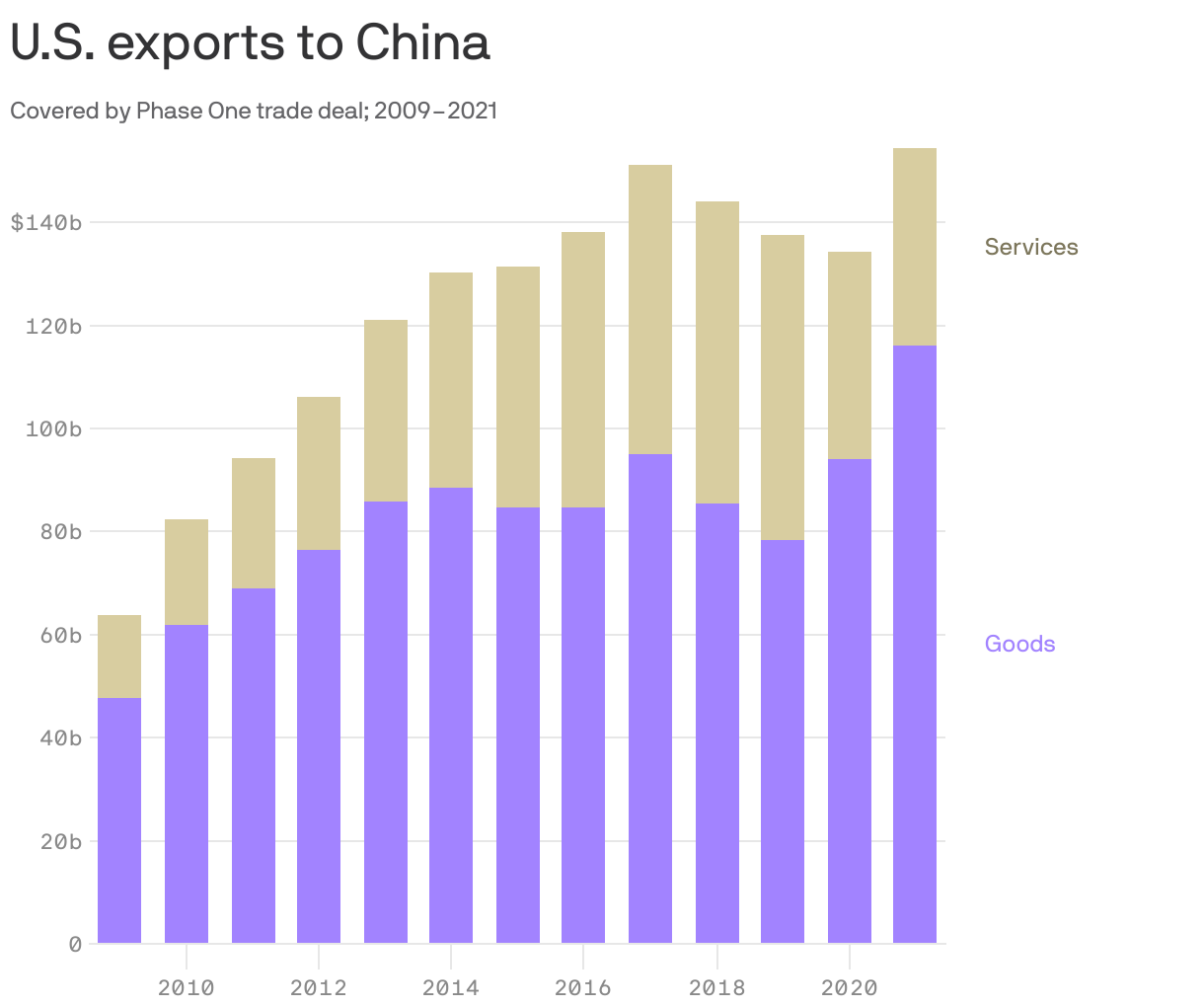

3. China trade bust

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netIt was only two years ago that former President Trump struck a mega trade deal with China, containing commitments by the Chinese to purchase vast sums of American exports. So how's it going?

- Not great, according to calculations by Chad Bown of the Peterson Institute for International Economics.

Bown finds U.S. exports to China since then have only been 57% of what was pledged as part of the deal, and below levels before the trade war even began.

By the numbers: Under the deal, China was to buy $274.5 billion in American goods and services covered by the deal in 2021. The actual number: $154.5 billion.

- Ultimately, Bown writes, "President Trump's trade war and phase one agreement did little to change China's economic policymaking."

4. The money decisions people most regret

Source: Riverhead Books

When it comes to financial decisions, it's easy to have regrets. How many people wish they hadn't sold their Amazon stock in the dot-com crash, for example, or coulda-shoulda-woulda bought bitcoin in 2013?

- But that isn't the type financial regret that is most common, Daniel H. Pink, author of a new book on regret, tells Axios.

Pink collected regrets of 16,000 people in 105 countries for The Power of Regret — and the financial regrets people have fall most often into two buckets.

- "First, people regret not building a strong foundation — that is, not saving money early, not being prudent," Pink says. "With financial regrets, they're less about not hitting a home run and more about not regularly getting on base."

- "Second, people regret not being bolder in their careers," he add. "For instance, lots of folks regret staying in lackluster jobs instead of starting a business or even not being more entrepreneurial in their job-holding careers."

More broadly, Pink urges people to cast aside "no regrets" as a life motto and focus on how, properly channeled, regrets can make us happier and wiser.

5. The great beer brawl

Beer varieties abound. Photo: Brian van der Brug/Los Angeles Times via Getty Images

American beer drinkers have plentiful options, with the variety of pilsners, IPAs and stouts available in a typical grocery store or sports bar greater than ever before.

- Yet paradoxically, the beer industry has also become highly concentrated, with two massive companies accounting for an estimated 65% market share. Some regulators want to make the industry more competitive.

The big picture: The Treasury Department on Wednesday published a report urging vigorous antitrust enforcement in the beer, wine and spirits industries — which could affect what Americans drink in the future, who makes and distributes it, and what it costs.

State of play: The report cites evidence that in any given local market, beer distributors must in practice closely ally with one of the two giants of the industry — Anheuser-Busch InBev or Molson Coors. Independent brewers must then rely on one or the other to get in stores, restaurants, and bars.

- One commenter cited by the Treasury called it "a duopoly that together holds 90% or greater of the beer market in a specific geographic territory" that "helps entrench dominant beer suppliers."

The bottom line: Is the beer industry a triumph of consumer-friendly competition, or a trust-buster's worst nightmare? It's both.

Have a good weekend, everybody.

Sign up for Axios Capital

Learn about all the ways that money drives the world