Saving for a San Diego home can take nearly two decades

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netIt'll take the typical San Diegan more than 18 years to save for a 10% down payment on the typical area home, Zillow data shows.

- That's by saving 5% of the median household income ($96,000) every month, or about $400 per month.

Why it matters: In 2022, California was the state people most often moved away from, according to a recent analysis by real estate company Home Bay.

- But, but, but: More than a quarter of those polled said California would be their dream state to live in if money wasn't an issue.

What's happening: It's getting harder for first-time homebuyers in San Diego given record high prices, elevated interest rates and low inventory, according to Julie Chang, a local agent with Pacific Sotheby's International Realty.

- Meanwhile, there's not much to buy, in part, because of under-building and current homeowners don't have incentive to sell.

- Many existing homeowners locked in low interest rates years ago and have increased home values and limited property taxes from Proposition 13, so could end up paying more to move, even if they're looking to downsize or rent, Chang said.

By the numbers: Zillow's research uses a San Diego home valued at $878,800 — the 4th highest in the country, behind San Jose, San Francisco and Los Angeles.

- $4,546 is the median mortgage payment with 20% down.

- Homebuyers should also expect to pay an extra 3% in closing costs.

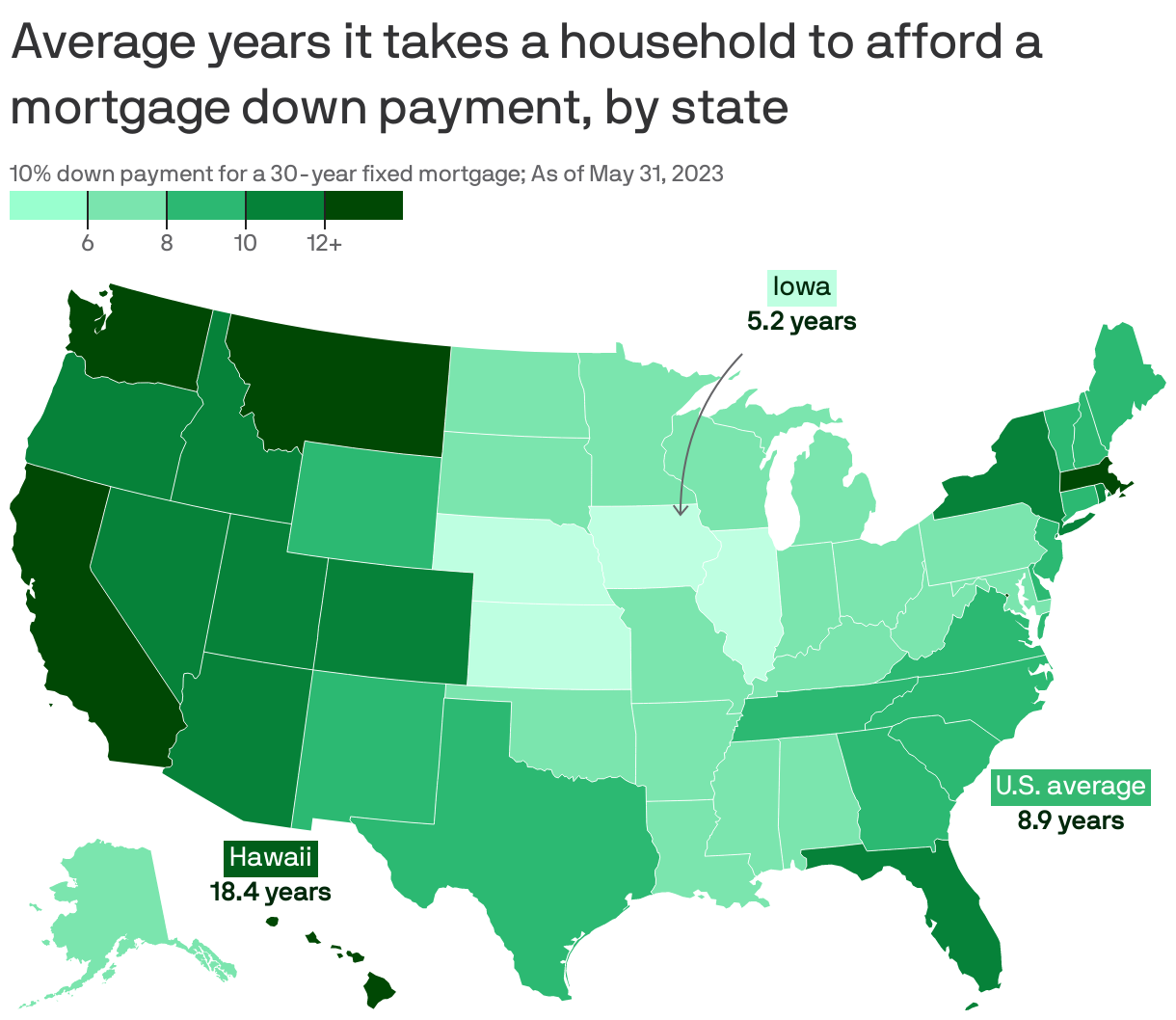

- Nationwide, the average time needed to save for a 10% down payment is 8.9 years. It's 16.5 years in California.

- Yes, but: Down payments can be as low as 0-3.5% for first-time home buyers, military personnel and others depending on the loan.

Between the lines: The share of first-time buyers in the U.S. has shrunk to a record low as inventory and affordability issues persist, according to the National Association of Realtors.

- First-timers are also waiting longer to buy; the median first-time buyer age jumped from 33 to 36 from 2021 to 2022, the latest data shows.

The big picture: Saving enough for a down payment is the biggest barrier to entry, says Brandi Snowden, a director at the National Association of Realtors.

- Many would-be-buyers are saddled with debt, including student loans, car loans and credit card debt.

- Homebuyers aren't putting as much money down as they did at the height of the housing frenzy, Axios' Emily Peck reports.

What they're saying: "It's very competitive … If you don't have a lot of money to put down or savings that can be a deciding factor as to why you don't get picked," Chang said.

The bottom line: Prospective homebuyers should contact a realtor and lender before looking to buy a house to understand what they can afford, not just what they qualify for, and build a personal strategy to achieve their goals, she said.

Be smart: Chang offered some tips for future homebuyers...

- Save for down payment and closing costs, plus an emergency fund for unexpected repairs or life events.

- Spend time in the community or neighborhood before buying there.

- Be able to hold a property for 7-10 years, whether that's living in it or renting it, to see the market cycle through.

- Consider house-hacking with 2-4 units to help cover the cost of living.

- Bring contractors and realtors to the property to understand things in the house like the roof or water heater.

- A first home should be a stepping stone, not a dream home.