Despite Bessent, Treasury message, bond returns aren't the economy

Add Axios as your preferred source to

see more of our stories on Google.

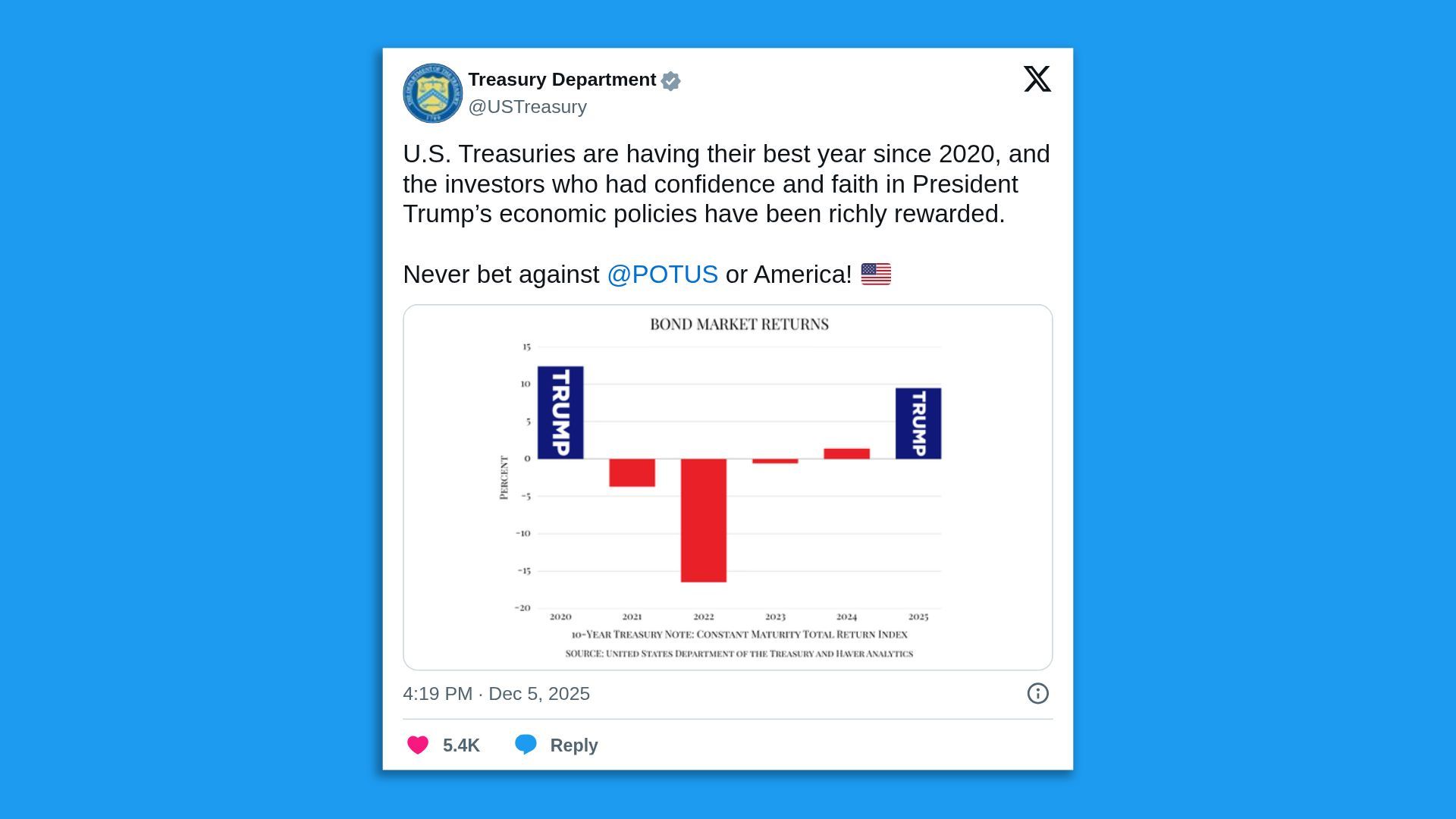

Screenshot: @USTreasury/X

Treasury Secretary Scott Bessent has a message for America: Investors in U.S. Treasury bonds have enjoyed a strong year of returns, and this is a reflection of American economic strength.

The big picture: Bessent's description of this year's returns on Treasury securities is accurate, but bond returns don't necessarily correlate with overall economic conditions.

- Frequently, bonds display inverse correlation with the economy as a whole, rallying when times are bad and losing ground when times are good.

What they're saying: "The bond market had its best year since 2020, and if I have anything to say about it as your top bond salesman, bonds will have another strong year in 2026 as we fight to bring Treasury borrowing costs down," Bessent said at a Tuesday night rally with President Trump in Pennsylvania.

- It was no mere offhand remark; Bessent has emphasized bond returns in social media posts and a Sunday TV appearance as well.

Zoom in: Treasuries have returned 5.4% so far in 2025, per the Morningstar U.S. 10+ year Treasury bond total return index. That is, indeed, the highest since 2020.

- Those returns — like any year's returns on bonds — reflect two factors: the interest earnings bondholders receive and can reinvest, and a move in rates that changes the value of existing bonds.

- The 10-year Treasury yielded 4.57% a the end of 2024, for example, so anyone who bought a security then has enjoyed both interest earnings and appreciation in the bond, due to the prevailing 10-year rate falling to 4.17% as of Wednesday morning.

- Bessent has emphasized that — contra much commentary in the spring when the trade war flared — this reflects global investor appetite for U.S. assets.

Yes, but: Often the biggest drivers of bond returns are changing expectations about growth and inflation — and those tend to negatively correlate with broader measures of well-being. (Historical numbers here are from New York University finance professor Aswath Damodaran's invaluable database of asset class returns.)

- The best year for Treasuries this century? That would be 2008, when they returned 20.1% — because the global economy was falling off a cliff and investors plowed money into bonds, seeking safety.

- The best year for Treasury returns since the 1920s? That would be 1982, when they returned 32.8% — amid an intensely painful recession that pushed the unemployment rate above 10%.

- There are examples that cut the other direction, as well. Some of the years remembered as boomtimes for the economy featured negative returns for bonds, as rates rose reflecting expectations of a more buoyant future. Bond investors lost 8.3% in 1999, for example, and 5% in 1987.

- To be fair, there are also plenty of examples of years that align with Bessent's framework, in which a good year for bonds coincided with a good year for the economic performance, like 1985, 1995, and 2019.

The bottom line: Bond prices move for many reasons — because of changing expectations for growth, inflation, or Federal Reserve policy; shifting appetites for U.S. dollar assets; and more.

- So while they can move in tandem with overall economic performance, they routinely move in the opposite direction.