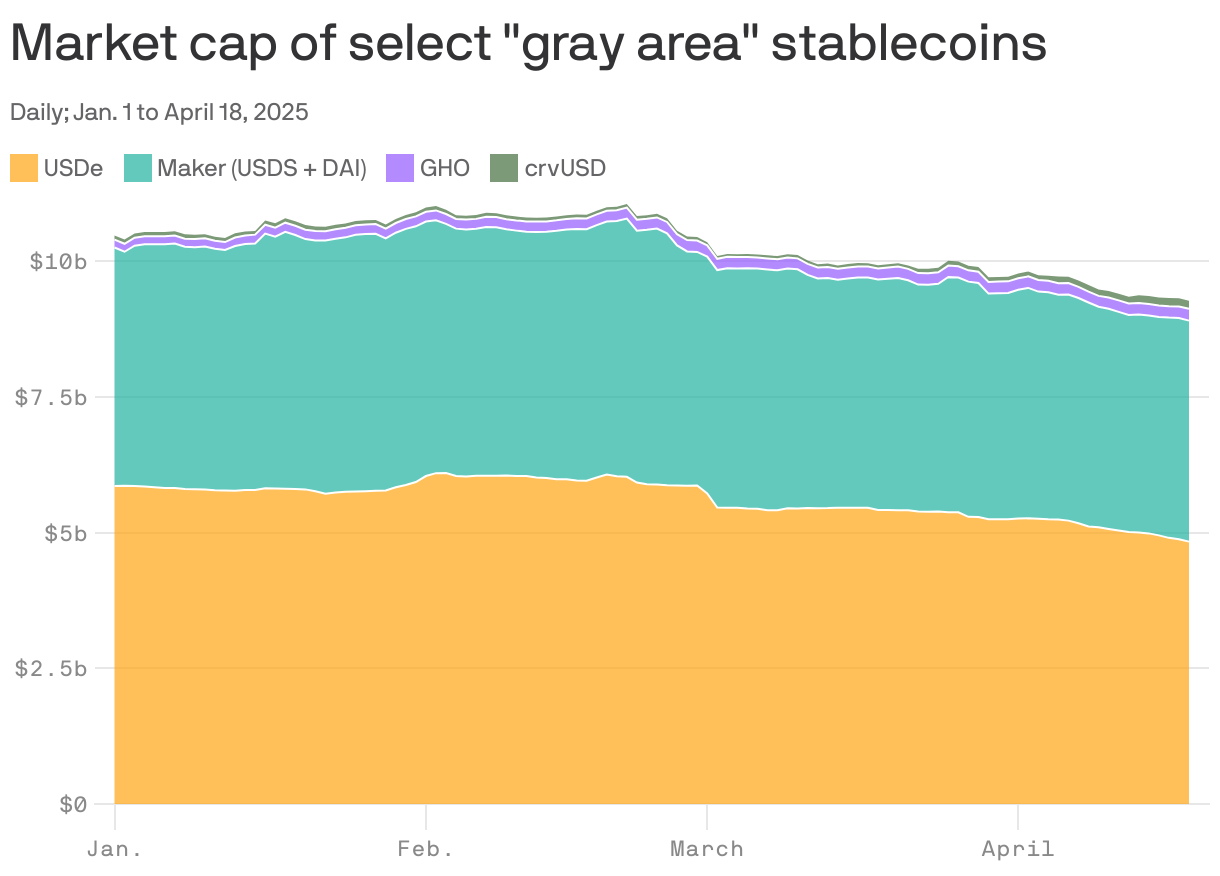

Charted: Stables in the gray area

Add Axios as your preferred source to

see more of our stories on Google.

Many more creative stablecoins will find themselves in a legal gray area if something like the STABLE Act passes, because it calls for a moratorium on issuing new "endogenously collateralized" stable tokens.

- Which leaves the ones that exist in a strange spot.

Why it matters: The market for such tokens (known better as algorithmic stablecoins) is much smaller than that of the big guys, Tether's USDT and Circle's USDC, but the market for these more decentralized alternatives exists and persists into the billions of dollars.

How it works: Unlike stablecoins backed by real-world assets like dollars or U.S. Treasuries, algorithmic stablecoins seek to maintain their peg using code and innovative financial schemes. (Like how MakerDAO/Sky issues DAI as loans against collateral.)

- Under the STABLE Act, these kinds of coins can't be issued (at least not for use by U.S. users) for two years.

- Meanwhile, the U.S. Treasury will study the matter of payment stablecoins, including these.

- In a report last week from Nansen Research, the authors point out that this new legislation could provoke changes in these coins, either carving out the U.S. or changing their fundamentals in some way, in response to policy.

Between the lines: Not all these stablecoins are competitors with Tether and Circle.

- For example, Ethena's USDe is mainly used to access yield from a crypto-native carry trade, and crvUSD seeks to offer more liquidation-resistant lending to borrowers in DeFi.

- Yes, but: The MakerDAO/Sky tokens, USDS and DAI, seek to be more decentralized, more censorship-resistant solutions to the same problems that USDT and USDC seek to solve (fast payment, low fees, zero intermediaries).

What we're watching: Their collective market cap has receded somewhat as it looks more likely that these stablecoins won't have a place in the first draft of the U.S. regulatory regime for stablecoins.

- But only a little.