Wall Street's battle with private credit hits fever pitch in M&A game

Add Axios as your preferred source to

see more of our stories on Google.

Private credit lenders and Wall Street banks are in a heated battle for mergers and acquisitions business, as deal supply remains significantly below financing demand.

Why it matters: The intense competition has led to loose financing packages that could cause trouble if the frothy market turns.

By the numbers: The Federal Reserve has said that leverage levels that exceed six times EBITDA "raises concerns for most industries."

- Lenders, especially private credit firms, are stretching that ratio in the current climate.

- "The amount of nine and 10 times leverage structures I've seen in the past month is astonishing," a senior banker tells Axios. "It's a food fight."

Zoom in: The financing for Bain Capital and Reverence Capital's $4.5 billion Envestnet deal involved four investment banks and three private credit funds, a large syndicate for a relatively small private equity deal.

- Notable, too, was that the three private credit firms involved — Ares Management, Blue Owl Capital, and Benefit Street Partners — worked together on the same deal. Direct lenders typically prefer to operate as a single lending unit.

- "The financing markets are a little stronger, a little more favorable to borrowers surely than they were a year ago," says Phil Loughlin, a Bain Capital partner who helped lead the Envestnet deal.

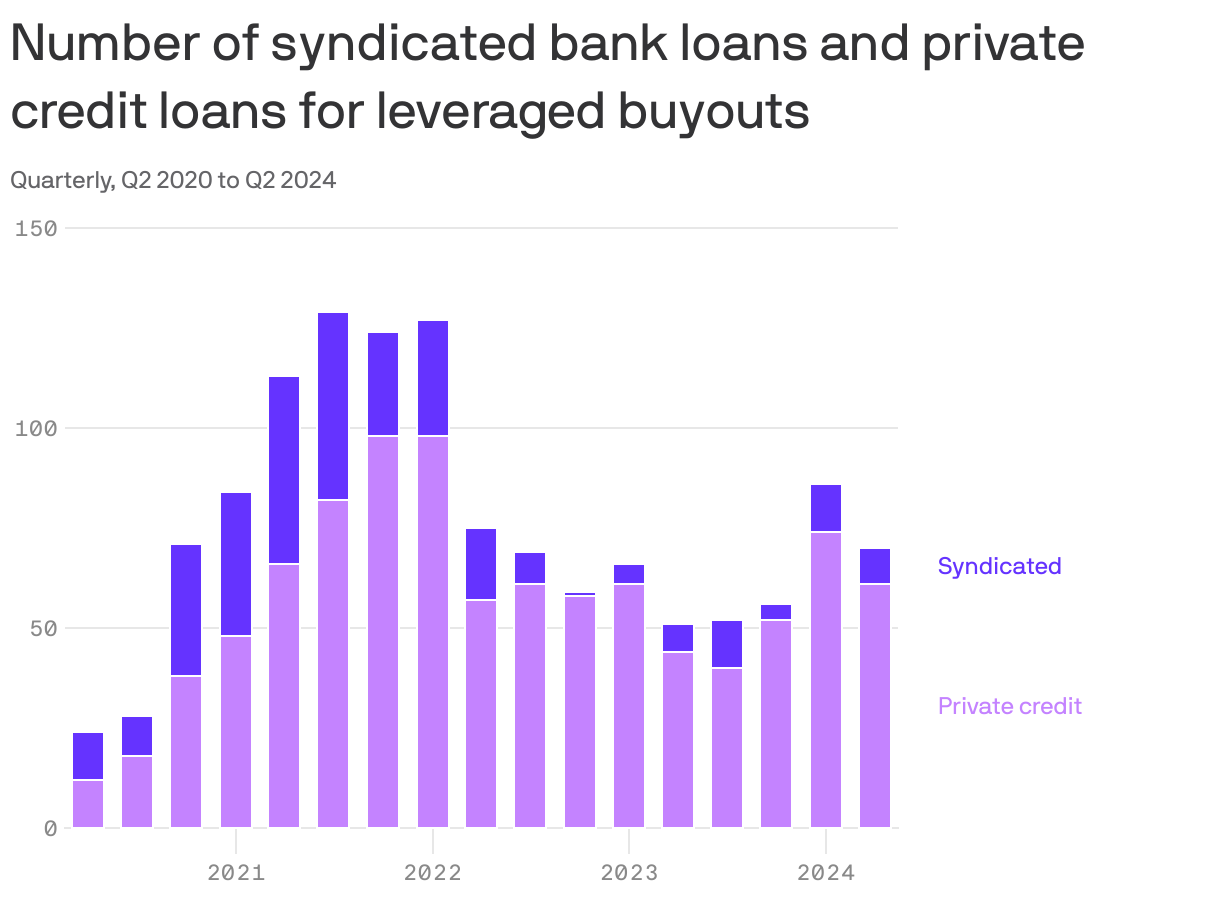

Catch up quick: Private credit kept the sputtering M&A machine going over the last few years while banks remained on the sidelines. But Wall Street firms jumped back in this year, boxing out direct lenders in certain deals.

State of play: Private credit funds raised a ton of money over the last few years and they need to put that money to work. Direct lenders typically offer more expensive financing and a simpler, quicker process than traditional banks.

- The demand these two entities are seeing comes as the supply of deals remains low. U.S. M&A is far below where it was in 2021 and, after a strong start to the year, it slowed in the second quarter.

Reality check: Private credit needs to deploy the capital they raised. These lenders therefore tend to be more concerned about putting money to work than return on investment, an approach that can stoke an already heated leveraged finance market.

Zoom out: Even though banks are back, private credit shops remain the dominant M&A lenders. And they're showing up on multiple sides of a given deal.

- When Thoma Bravo agreed to buy automotive research company JDPower, KKR's capital markets business was part of the financing team. In addition, KKR's private credit business purchased part of the deal's second lien debt as well.

The bottom line: Markets are humming at the moment but should things turn quickly, borrower-friendly financing deals will come back to haunt the lenders — and the companies — that stretched to win that business.