The 2024 loan boom

Add Axios as your preferred source to

see more of our stories on Google.

The Fed hasn't cut rates yet, but in the first half of this year, the riskiest U.S. companies slashed the interest they're paying on more than half a trillion dollars in loans.

Why it matters: The huge investor demand for debt has driven rates down, granting welcome relief to borrowers who were shocked in 2022 by the speed with which their floating-rate loans became much more expensive to service than they'd anticipated.

How it works: Borrowers with expensive debt can refinance it into cheaper debt — or they can simply approach their existing lenders and ask them to reprice the outstanding loans.

- Those lenders are likely to sign onto the so-called repricing if they know the borrower could easily refinance at a lower rate elsewhere.

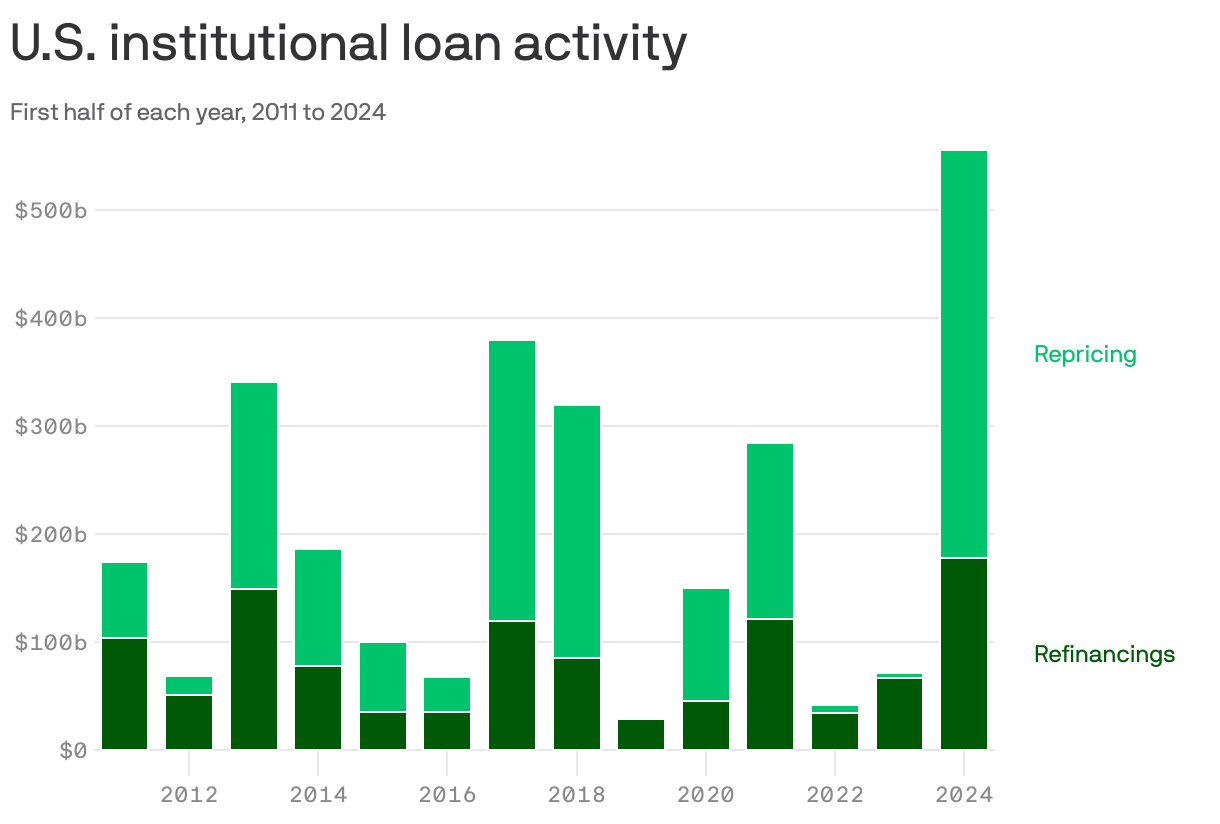

By the numbers: Refinancings and repricings of below-investment-grade corporate loans totaled $556 billion in the first half of 2024, up from $71 billion in 2023 and just $42 billion in 2022.

- Add in new loans, and the loan market has reached "a fever pitch" of $736 billion in first-half activity this year, per Pitchbook LCD, up from less than $200 billion in the same period of 2022 and 2023.

- That number obliterates the previous first-half record of $584 billion set in 2017.

Follow the money: The average borrower is saving 0.54 percentage points in interest costs every year — which means $2.2 billion of annual interest savings overall.

Between the lines: One reason for the repricing activity is that very few companies are showing much interest in taking out new loans.

- Non-refinancing issuance was barely over $110 billion in the first half, not nearly enough to keep up with demand from big loan investors.

What's next: This breakneck pace will probably continue for at least the next several months, as borrowers try to squeeze in deals before an election that could inject uncertainty into the market.