As summer's hazards near, all eyes are on insurers of last resort

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netWith hurricane season set to begin June 1 and wildfire risk gradually ratcheting up as well, the pullback by private insurers from danger zones is coming into sharper focus.

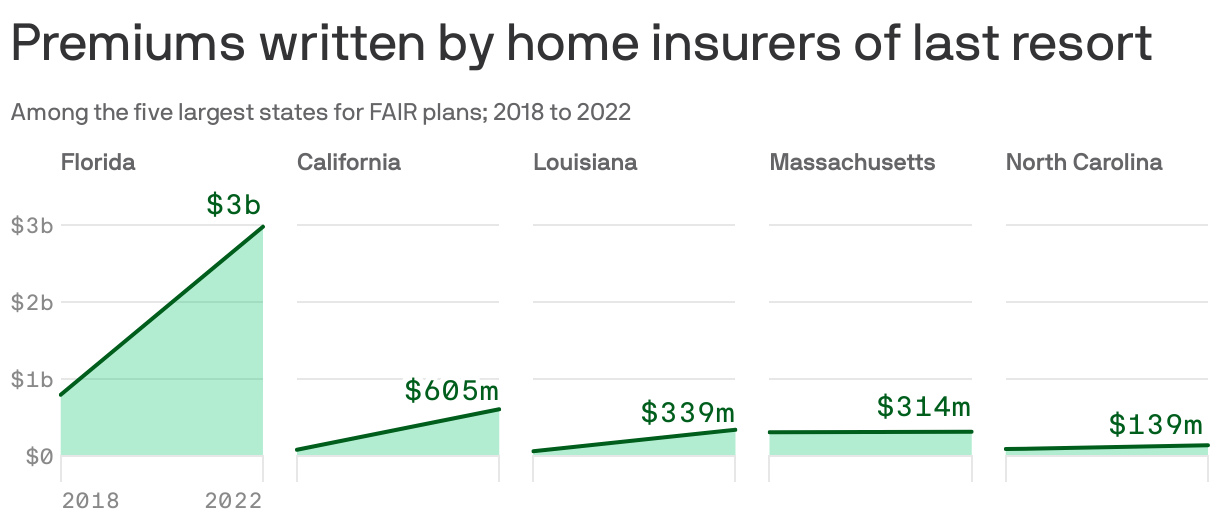

Why it matters: In certain states — particularly Florida, California and Louisiana — private insurers are fleeing areas considered at high risk. It's leaving so-called "residual," or last resort plans, to pick up the tab.

- But these state-run insurers, as is the case in Florida, may not be able to cover all the losses in the event a major hurricane strikes a heavily populated area.

Driving the news: Forecasts for the 2024 Atlantic hurricane season are worrisome, with record warm tropical waters likely to combine with a developing La Niña in the Pacific to yield an unusually active one.

- Due to its relatively frequent hurricanes and high population growth in catastrophe-prone areas, Florida is ground zero for private insurers retreating from high risk zones, as homeowners insurers seek to contain their losses.

- For residents, the remaining insurance options are either pricey residual plans; underinsuring; or no home insurance at all.

- With a potentially record number of Atlantic storms this season, the likelihood of a landfalling major hurricane is higher (though not guaranteed).

- As meteorologists and insurance experts tend to say, "All it takes is one" to have a disastrously expensive year, with knock-on market effects.

Zoom in: A new Moody's report on homeowners insurance finds Florida has about 2.9 million homes and $580 billion at risk of a potential hit by a catastrophic Category 5 hurricane.

- In other states like California, other perils such as wildfires are driving insurance flight, and a growth of residual insurers.

- And in the Midwest, the costs of severe thunderstorms carrying large hail and damaging winds are driving up insurance costs, too.

- In 2023, more than 80% of the country saw a double-digit homeowners insurance rate increase, with up to a 30% increase in some states. This is expected to continue as insurers retreat, Moody's found.

The intrigue: Major insurers like Allstate and State Farm have stopped issuing new policies or decided not to renew existing ones in increasingly risky states, helping residual plans to take off.

- Florida saw a 274% increase in premiums written for its Citizens Property Insurance Corporation, Moody's found.

What they're saying: "The topic of insurability is only going to grow more important as natural catastrophe risk continues to accelerate," Steve Bowen, Gallagher Re's chief science officer, said in an email.

- "There is a real possibility that we could see not just a higher volume of uninsured property damage in the coming years, but also a greater amount of underinsured damage," Bowen said.

- "This is due to people actually having insurance coverage but only being covered up to an amount that does not equal the total value of the physical structure and its contents."

What's next: Bowen said that new insurance products designed for specific perils could help fill protection gaps, such as parametric insurance, which would pay a set amount if a hazardous event occurs, based on its magnitude.

- For example, such a policy might pay $150,000 in the event of a magnitude 5.0 earthquake.