The problem with America’s high homeownership rate

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Aïda Amer/Axios

America's decades-long love affair with homeownership is holding back the economy, hobbling the Federal Reserve, and exacerbating a national housing crisis.

Why it matters: We're stuck here now — at this point there's just too much wealth stored in too many houses for anything to meaningfully change.

The big picture: Life is an unpredictable journey. People change where they want or need to live all the time, and a country with a 66% homeownership rate is not conducive to that.

- We get married or divorced. Children arrive, leave the home, maybe come back again. Parents sometimes move in. A job might appear in a different city — or an employer might embrace remote work, allowing a move to anywhere. Wealth and income rise and fall, affecting the amount of house we can afford. Personal taste changes, too — someone who loves a sleek downtown condo when they're in their 20s might prefer something secluded in the countryside a few decades later.

- For all these reasons and many more, there's huge value in being able to easily move from one house to another. Instead, the U.S. system has effectively locked millions of Americans into a single home, one they can often barely afford and might not even much like.

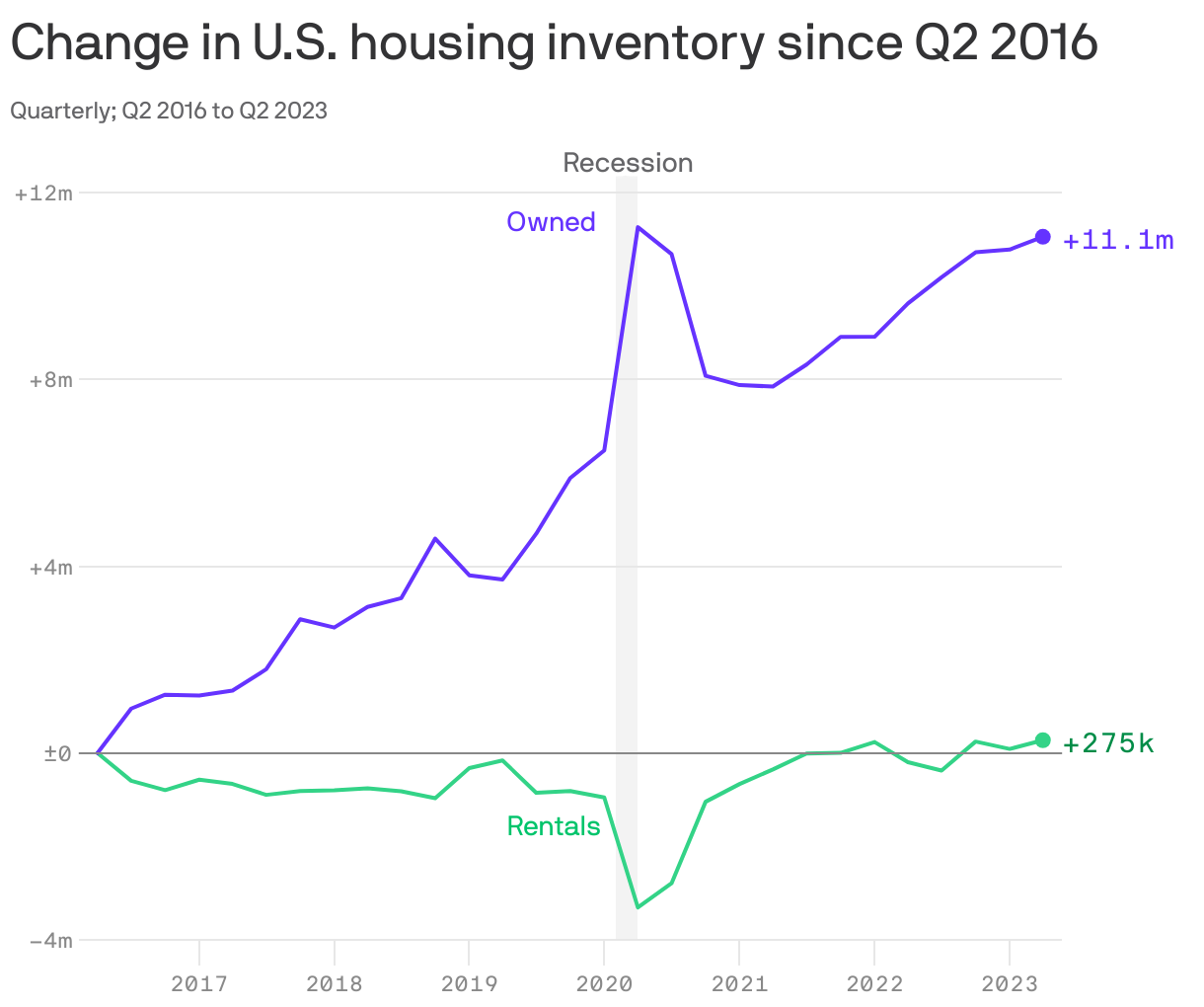

By the numbers: 20 years ago, in the third quarter of 2003, there were 83 million owner-occupied homes in America, and they were changing hands at a rate of 6.5 million homes per year.

- Today, the number of homes has increased to 96 million, but the rate of existing-home sales has slumped to just 4 million homes per year.

- Percentage-wise, that's a fall from 7.8% of existing homes sold per year to just 4.2%. Americans are staying in their homes for many more years on average than they used to, and that's mainly for financial reasons — not because they particularly want to stay put.

The result is a deeply inefficient distribution of where people live.

- Not only do Americans give up happiness and even income when they stay rather than move, they also take up millions of square feet of space that are desperately needed by a growing population.

How it works: Quite aside from the ludicrously high direct cost of selling a house — often 10% of the sale price — tax law also provides a huge incentive for individuals to remain in a house that might be far too big for them and that could provide shelter for many more people.

- Selling the house can trigger a significant capital-gains taxes. (One bill in the House of Representatives wants to exempt up to $1 million in housing capital gains from tax, for just this reason.)

- Renting the house can allow an owner to continue to reap the benefits of a low mortgage rate — but they would need to pay income tax on that rental income.

- Besides, the homeownership norm in many single-family neighborhoods is so ingrained that it sometimes doesn't occur to people that wanting to move doesn't have to mean selling.

A market is efficient when there's abundant liquidity and scarce resources get allocated to where they can be put to best use. The rental market, by those standards, while far from perfect, is vastly more efficient than the thin and janky market in existing homes.

The downsides of financialization

Houses are like credit cards: They're a combination of something we all need with a complex and inefficient financial product. In the case of credit cards, a convenient payment mechanism is blended into a very costly line of credit; in the case of houses, basic shelter is incorporated into a cumbersome and expensive forced savings device.

- That savings device — the 30-year fixed-rate mortgage — is distorting the U.S. economy and making it much harder for the Federal Reserve to do its job.

The abundance of fixed-rate mortgages in the economy have rendered it largely immune to the Fed's rate hikes, thereby forcing the central bank into a "higher for longer" stance.

- In a speech on Friday, Fed chair Jerome Powell was at pains to point out that house prices and rent prices are still going up, even after 11 rate hikes.

- Indeed, he worried that even now, "the housing sector is showing signs of picking back up."

Key stat: U.S. mortgage debt now totals $12 trillion, or 45% of GDP.

Between the lines: Houses — or rather, mortgages — have become the primary means of American middle-class wealth creation.

- The principal amount outstanding on a mortgage slowly declines over time, even as the value of the home (generally) goes up. The result, if everything goes according to plan, is ever-greater home equity, and therefore wealth.

Where it stands: A U.S. household in the middle earnings quintile has $145,200 in median net worth, according to the Census Bureau. Of that, $93,910 — or 65% — is equity in their own home.

- Amazingly, that number includes the 36% of households in the middle quintile who don't own their home at all, and for whom home equity is therefore 0% of their net worth.

Zoom out: Houses have become Americans' most important financial asset. As a result, a majority of the population is literally invested in seeing the value of homes always go up.

- The result is endemic Nimbyism — knee-jerk local opposition to any attempt to build more desperately needed housing, pretty much anywhere.

- Because homeowners are much more likely to vote than renters, and infinitely more likely to vote in local elections than people who would like to move into the district but can't afford to, politicians too have every incentive to hobble new construction.

The bottom line: All humans need shelter. But homeownership has created a class of winners (think of everyone smugly sitting on a mortgage fixed at 3% regardless of what the Fed does) — who also have a financial incentive to deny new shelter to others.