America may need to start caring about the deficit again

Add Axios as your preferred source to

see more of our stories on Google.

In the latter years of the 2010s, there was a widening bipartisan sense that fiscal deficits don't really matter. Now, they do again.

Driving the news: That's a clear implication of new long-term forecasts for deficits and debt issued by the Congressional Budget Office on Wednesday afternoon.

Why it matters: The United States fiscal deficit is now at levels that have been surpassed only in deep crises — and are forecast to widen from here, even in the absence of new challenges.

- If unchecked, that would imply higher interest rates and inflation and less private investment and growth in the coming decades, the CBO warned.

By the numbers: The U.S. government is set to run a deficit of 5.8% of GDP this fiscal year, the agency said — a period in which the unemployment rate has averaged a mere 3.6% so far.

- The deficit exceeded that level in only seven years since 1962, all of which coincided with rebounds: 1983 (aftermath of severe recession); 2009-2012 (global financial crisis); and 2020-2021 (pandemic).

- The deficit is on track to narrow as a share of the economy later this decade before soaring in the 2030s and 2040s.

- Those numbers, however, assume relatively steady economic growth — and not the kinds of surprise shocks like major recessions, wars or financial crises that have a way of upending fiscal forecasts for the worse.

Flashback: In the late 2010s, interest rates seemed locked at perpetually low levels, leading to widespread equanimity about the fiscal picture. After all, even though deficits were large, low interest rates meant debt service costs were manageable.

- The Trump administration and Congressional Republicans enacted a major tax cut package without offsetting spending cuts, adding to deficits.

- Influential center-left economic thinkers including Olivier Blanchard and Larry Summers backed away from deficit alarmism, citing low long-term interest rates.

- Modern monetary theory, which is thoroughly dismissive of fretting over budget deficits, gained momentum in some precincts of the political left.

What's changed: For one thing, nearly $5 trillion of emergency pandemic spending added to the pile of debt in a way no one anticipated in 2019.

- "The pandemic created enormous economic losses, and we used borrowing not so much to make the losses vanish into thin air but to spread them out over time," Wendy Edelberg, director of the Hamilton Project and a former CBO chief economist, tells Axios.

- Moreover, the high-inflation environment of the last two years has caused interest rates to rise, making debt service costs higher.

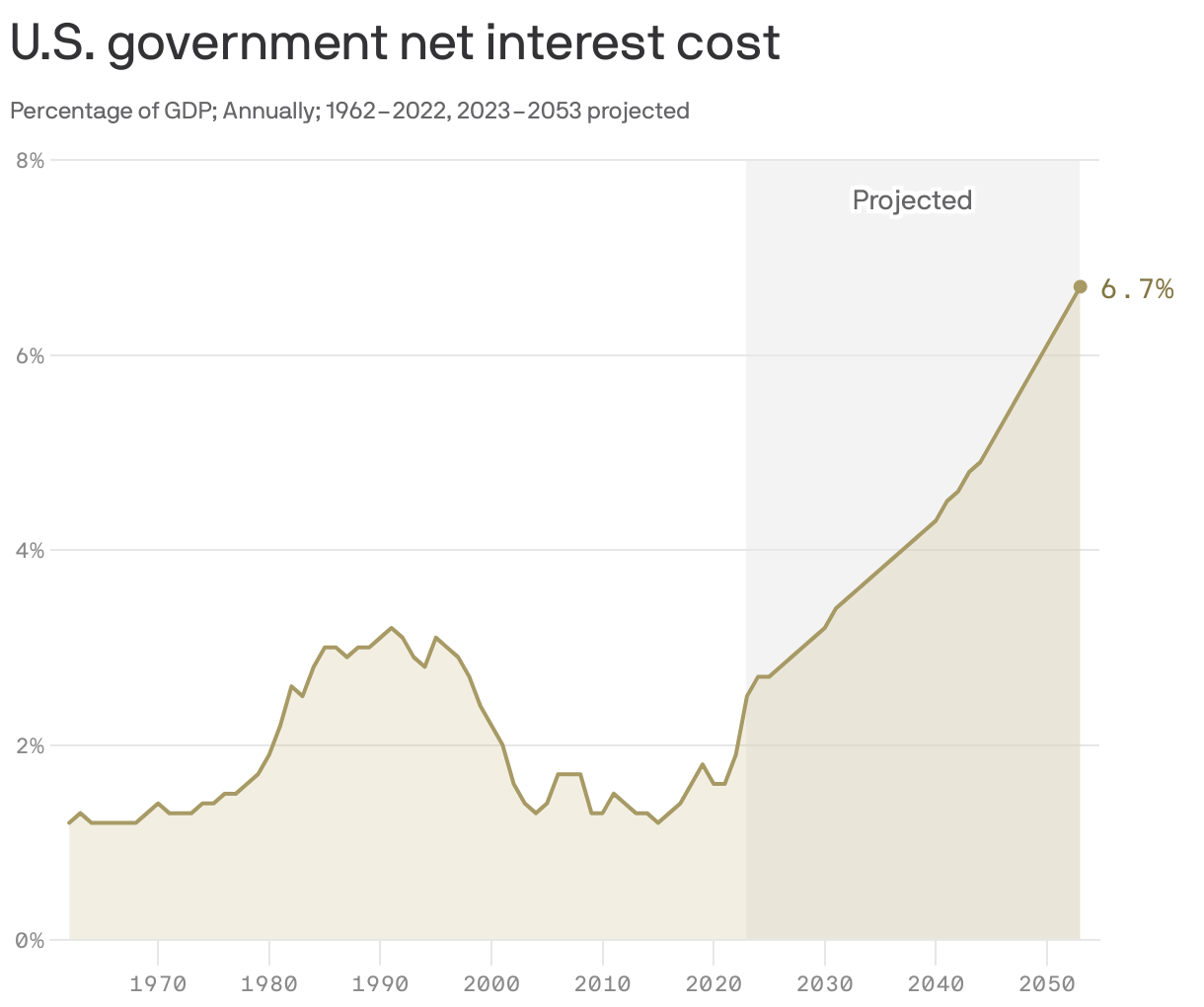

Back in 2017, net interest costs for the U.S. government were only 1.4% of GDP. In 2023, with a higher debt load and higher interest rates, that is on track to be 2.5% of GDP.

- It is forecast to rise steadily from there, implying trillions in government payments to bondholders that would crimp other national priorities.

- Net interest reaches an astounding 6.7% of GDP in 2053 in the CBO projections, though interest costs rising according to the projections would almost certainly generate a course-correction long before then.

- The previous peak dating back six decades was 3.2%, and that occurred in 1991 — coinciding with an aggressive deficit reduction plan from the George H.W. Bush administration.

What they're saying: "A decade ago Washington was overly obsessed about the deficit," says Jason Furman, an Obama economic adviser and author of an influential 2019 article with Summers titled "Who's Afraid of Budget Deficits?"

- "I don't think it is our No. 1 problem today, but it is time to start paying attention again."

- He adds that deficit reduction now would help control inflation without very high interest rates.

Yes, but: There could be positive surprises that improve the fiscal outlook, such as a productivity boom spurred by artificial intelligence (as happened with information technology in the late 1990s) or global interest rates receding.

The bottom line: In the early 2010s, as the nation suffered from the aftereffects of the financial crisis, there was probably too much alarm about deficits and debt. Now, there's probably too little.