FTX management details new allegations on misuse of customer funds

Add Axios as your preferred source to

see more of our stories on Google.

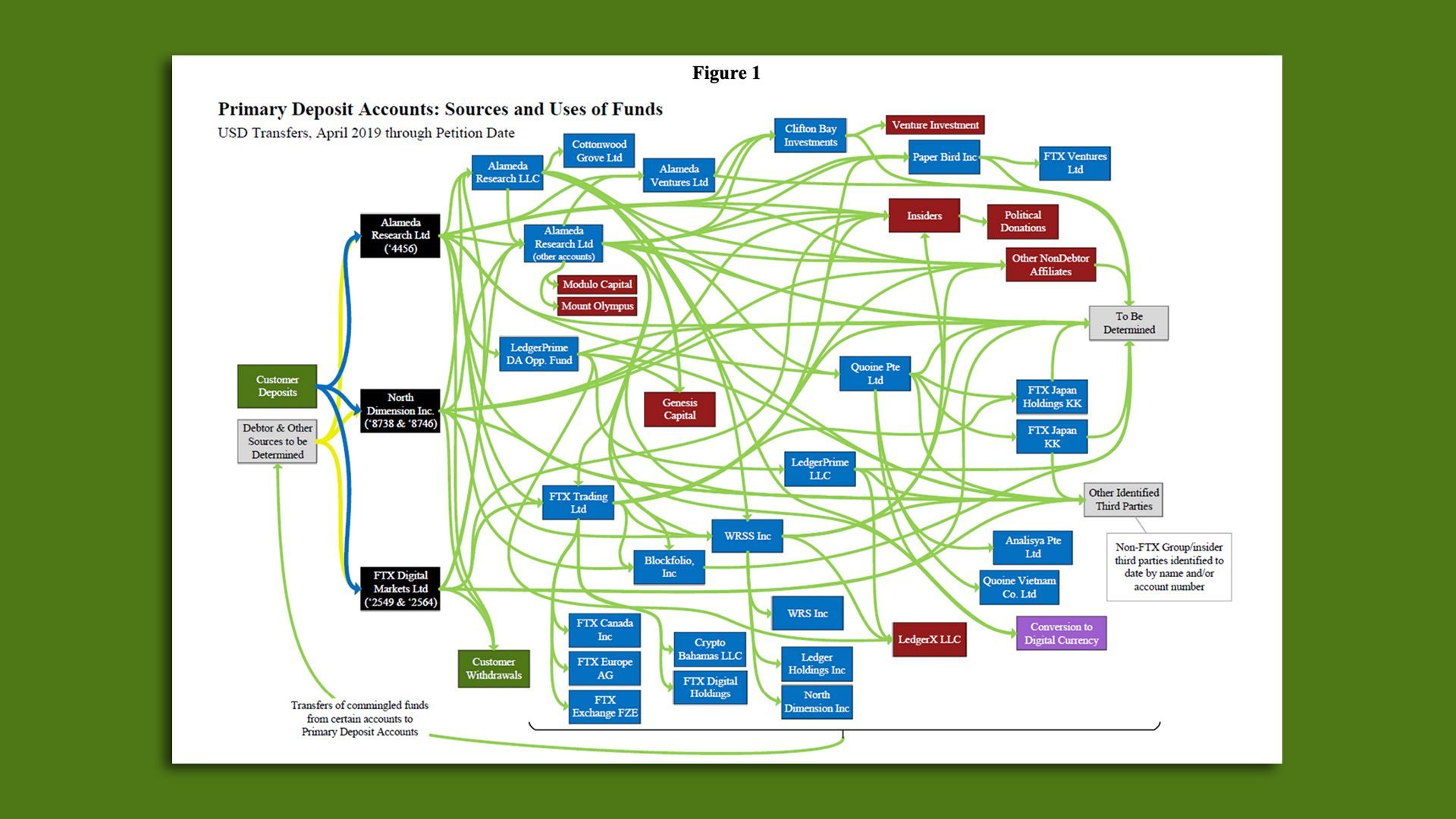

Flow chart of FTX user money from the new report by current FTX Management.

FTX's new management has provided more details on the alleged misuse of FTX customer funds by FTX, Alameda Research and related entities.

Why it matters: Most FTX watchers already believe claims that the firm made use of funds deposited by users of the FTX exchange, but allegations made in this report would confirm that more directly than we've previously seen and shed considerable light on various aspects.

- The report released Monday, "The Commingling and Misuse of Customer Deposits at FTX.com," gives us an updated estimate of how much money was missing at the time of its bankruptcy filing: $8.7 billion (pretty much in line with what we'd all been led to expect). The missing money primarily came in the form of stablecoins and cash.

What they're saying: "Simply put, as a former Alameda employee explained to the Debtors, the FTX Group made no meaningful distinction between customer funds and Alameda funds," the report says.

Of note: "It is important to recognize that this analysis is ongoing, incomplete and subject to change," the report notes.

Context: FTX and its related companies collapsed globally in November 2022. Up to that point, the new management argues that FTX had been, from the very beginning, making use of customer funds, without any real intention even to keep track very carefully of what they were misusing.

- In a few cases, customers were really protected. They were protected in places like Japan, Cyprus and Singapore, which had taken the time to write updated rules for crypto exchanges.

- The report doesn't deal with FTX.US.

- FTX is known to have operated from the U.S., Hong Kong and The Bahamas. The report contends that these moves were made seeking lax regulatory environments.

Zoom in: The report frequently discussed the actions of a person going by Attorney-1, alleging that this person was instrumental in making it possible for FTX to create legal smokescreens about its illicit behavior.

- The person who seemed to be the top attorney at FTX was previously associated with a gambling site that eventually admitted to inappropriately making use of customer funds.

Meanwhile, the report goes into detail explaining how entities like FTX Digital Markets and North Dimension, Inc., were set up for no other reason than to receive customer deposits on behalf of FTX and distract banking partners.

- It also contends that the political donations made by way of various FTX executives may have been described as loans, but there was no documentation of the loans of any kind.

- It does, however, describe a document where the firm kept track of banks that had become suspicious and would no longer work with the firm.

The intrigue: While we previously noted that the FTX terms of service forbade the firm from taking custody or making use of its users' "Digital Assets," the new report draws attention to the fact that FTX's terms were silent on another crucial point.

- "In fact, the Terms of Service were silent on what FTX Trading Ltd. would do with customer fiat currency, and made no claim that the company would segregate, custody, secure or otherwise protect it," the report notes.

The bottom line: The document explicitly accuses Sam Bankman-Fried and his staff of lying about customer funds repeatedly.

Editor's note: This article was updated with information detailed in the report on the terms of service for FTX Trading Ltd.