Bond market sounds the alarm on debt ceiling negotiations

Add Axios as your preferred source to

see more of our stories on Google.

An unprecedented dislocation in the Treasury markets is a sign of extraordinary nervousness about the upcoming U.S. debt ceiling negotiations.

Why it matters: Short-term interest rates are normally the most boring and predictable part of international financial markets. The current chaos is a sign of just how seriously traders are taking the extreme level of uncertainty in Washington.

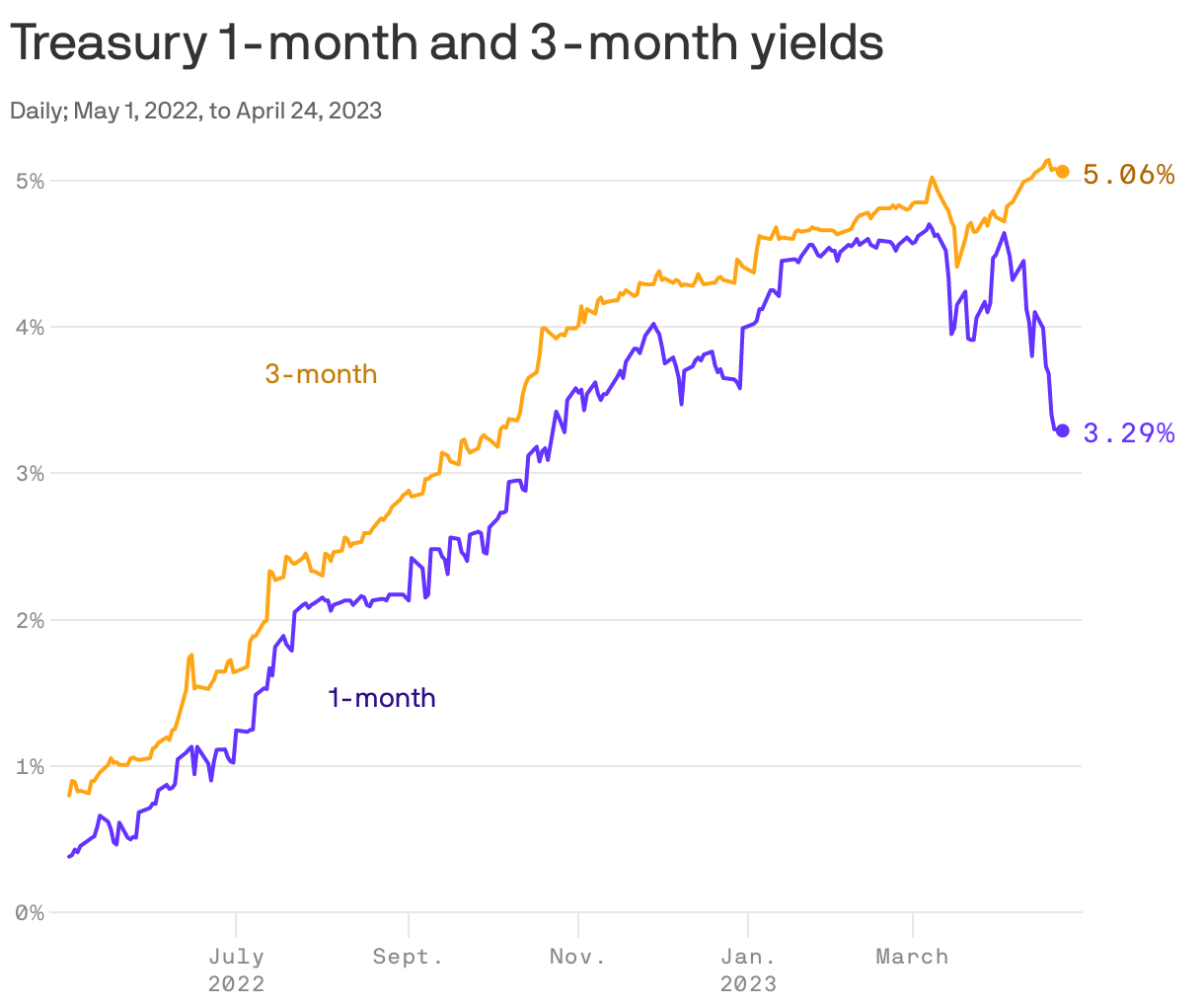

By the numbers: Three-month Treasury bills are yielding 1.77 percentage points more than their one-month equivalents. That's the largest gap of all time.

The big picture: When markets are nervous, they pile into Treasury securities, which are conventionally considered to be the risk-free benchmark against which everything else is measured.

- The sharp drop in one-month Treasury yields reflects just such a flight-to-quality trade. (Yields fall when prices rise in the face of strong demand.)

Between the lines: Three-month yields haven't fallen — indeed, they've risen over the past couple of weeks — because fast-forwarding three months from now takes us into the heart of any potential debt ceiling default.

Where it stands: The U.S. hit the debt limit earlier this year. Since then, the Treasury Department has used "extraordinary measures" to allow the nation to keep paying its bills. But it can only do that for so long.

- The Treasury is expected to issue new guidance in the coming days on when those measures might be exhausted, based on tax revenue data.

- Private sector economists, including those at Goldman Sachs and Bank of America, warn that revenues have been weaker than anticipated. That means a potential default might be sooner.

The bottom line: Buying a one-month Treasury bill doesn't protect against a government default; nothing can do that. The bill will mature, and the cash will need to be reinvested somewhere.

- But for the time being, a one-month bill is significantly — and alarmingly — less risky than a three-month bill.