The bond market's record February

Add Axios as your preferred source to

see more of our stories on Google.

Company executives are starting to believe the “higher for longer” story about interest rates.

What's happening: They’re scrambling to tap the debt market now, before borrowing costs go up even more. Call it a capitulation to the new reality.

Why it matters: It’s a behavior shift from last year, when rising rates had many companies sitting on the capital markets' sidelines.

State of play: The investment grade bond market, where companies with higher credit ratings borrow, saw a record February for new bond placements — despite the fact that yields were soaring.

- The month's final deal tally of $147 billion was fairly surprising, considering estimates heading into it had been in the $90-to-$100 billion range, Blair Shwedo, head of investment grade trading at U.S. Bank, tells Axios.

- Executives wanted to "get a lot of their issuance out of the way, for fear that they could run into higher rates if they were to delay issuance," he adds. "I think there may be some nerves about whether corporate yields go back out to 6%."

- (A key index measuring the market went from yielding 4.9% on Feb. 2 to 5.56% at the end of the month.)

The big picture: The recent string of hot economic data, which started with the Feb. 3 jobs report, jolted investors and market watchers out of the theory that a pause in Fed tightening was close at hand.

Flashback: Bond issuance slowed drastically last year.

- That's because rate volatility made it difficult for bankers to place deals with investors — and companies balked at yields that were vastly higher than anything they'd seen over the last decade.

- February's activity shows that companies are now coming around to the idea that we may not be returning to the low-rate world of the 2010s any time soon.

Zoom out: In fact, that era is something of an anomaly, historically speaking.

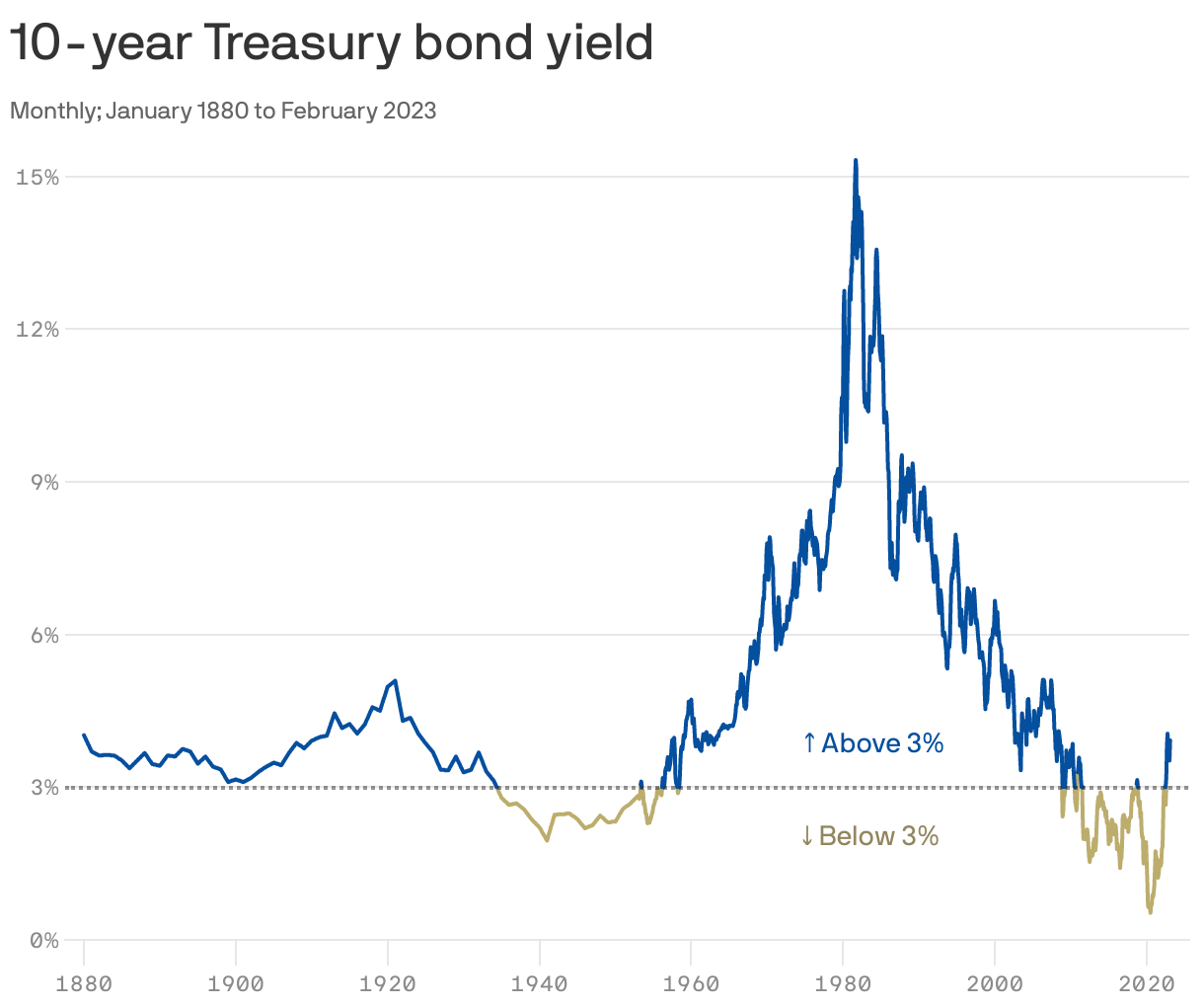

- Just look at the 10-year Treasury, the main benchmark for corporate borrowing. It sat below 3% for only two periods in modern U.S. financial history — the post-Great Depression and post-financial crisis eras.

- “The level of rates that we had from 2012 to 2022, we've never seen that before except after the Great Depression and World War II,” says Robert Tipp, chief investment strategist at PGIM Fixed Income.

The intrigue: Tipp says all that recent data pointing to the strength of the economy and labor market amid the rapid rate hikes means the neutral interest rate may very well have moved up.

The bottom line: If the 10-year settles into a range that’s more in line with historical norms than the post-financial crisis decade, it could reshape borrowing strategies across corporate America, which got pretty accustomed to ultra-cheap money.