The pandemic brought more Americans into the financial system

Add Axios as your preferred source to

see more of our stories on Google.

The fiscal stimulus unleashed on America in the wake of the pandemic had one interesting side effect: It significantly decreased the number of U.S. households without bank accounts.

Why it matters: Broadly speaking, the pandemic was good for economic inclusion. It seems to have significantly increased homeownership among Black, Asian, and Latino Americans; it also significantly decreased the number of households outside the banking system entirely.

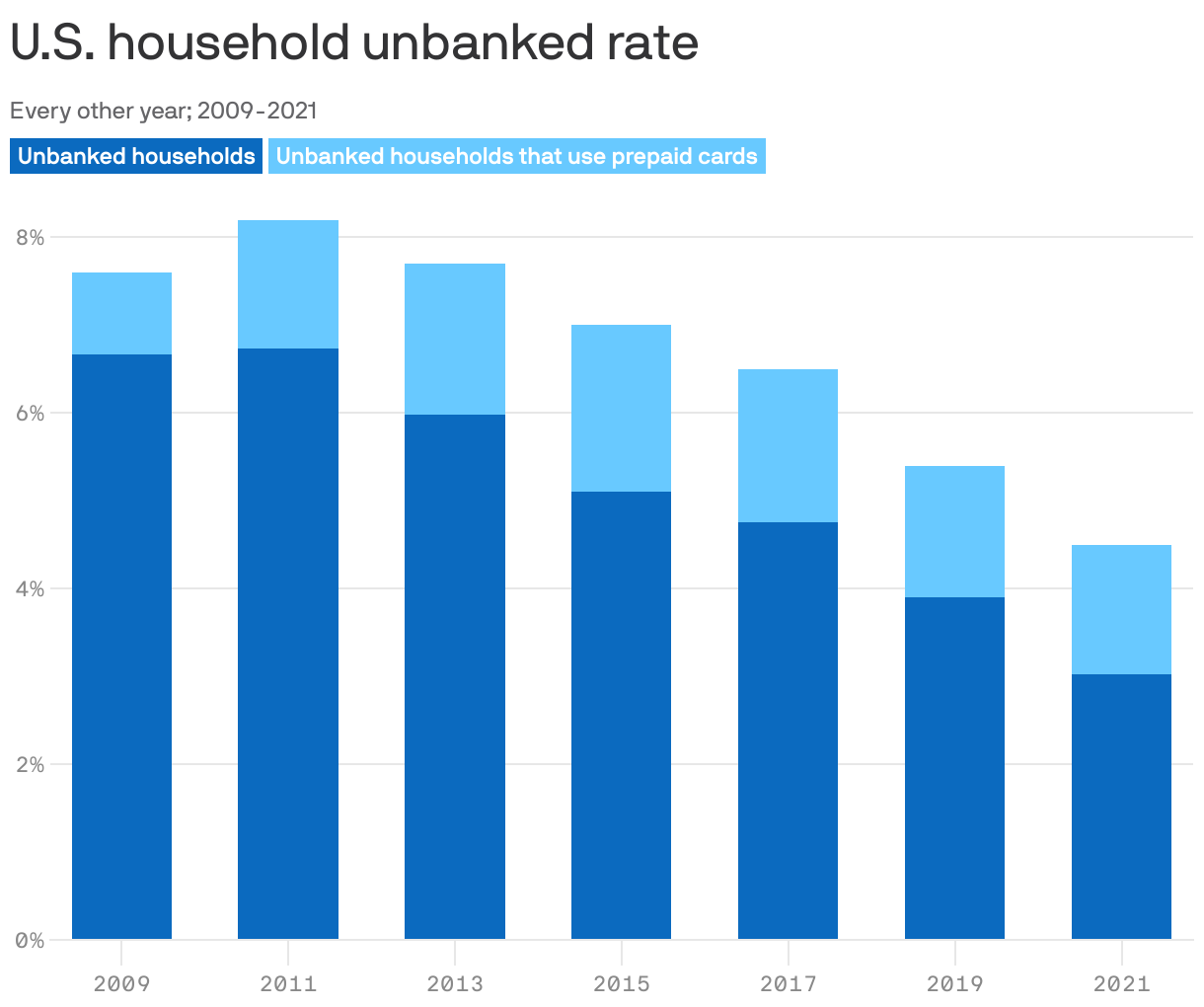

The big picture: The FDIC measures the proportion of U.S. households that are unbanked every two years — but defines unbanked as not having a checking or savings account at a bank or credit union.

- Practically speaking, however, general purpose reloadable prepaid debit cards have become de facto checking accounts. Anything you can do with a basic checking account you can normally do with one of these cards — and most of the time your funds are FDIC insured.

- If you consider households with such cards to be banked, then only 3% of U.S. households are now unbanked — down 23% from 2019, and down 55% from 2011.

- That number falls even further if you subtract the people who have accounts at Venmo, Cash App, or other non-card-based digital depository institutions.

Driving the news: The biggest reason given for opening an account was the desire to easily receive stimulus checks and other government payments during the pandemic.

- The second-biggest reason was getting a new job.

Between the lines: The pandemic accelerated the mobile banking revolution. In 2017, the most popular method that households used for accessing their bank accounts was going to a physical bank teller. That was the preferred channel for 25% of households, while mobile banking was popular with only 15%, per the FDIC.

- In 2021, just four years later, tellers were the preferred choice of only 15% — while mobile banking was the go-to channel for 44%.

The intrigue: Klaros senior advisor and former Green Dot Bank CEO Mary Dent has a good question. If almost everybody is banked, why do check cashers still exist?

- The answer: Not everybody is comfortable banking with an app. For people living paycheck-to-paycheck, mobile check deposit can take too long to clear; people with outstanding debts might also fear that their funds will be frozen by creditors.

The bottom line: Most of the remaining unbanked are unbanked by choice, says Dent. If you rationally don't trust banks, then you won't want to deposit your money with one. That helps explain why Black and Hispanic Americans have much higher unbanked rates than white Americans at every level of the income spectrum.