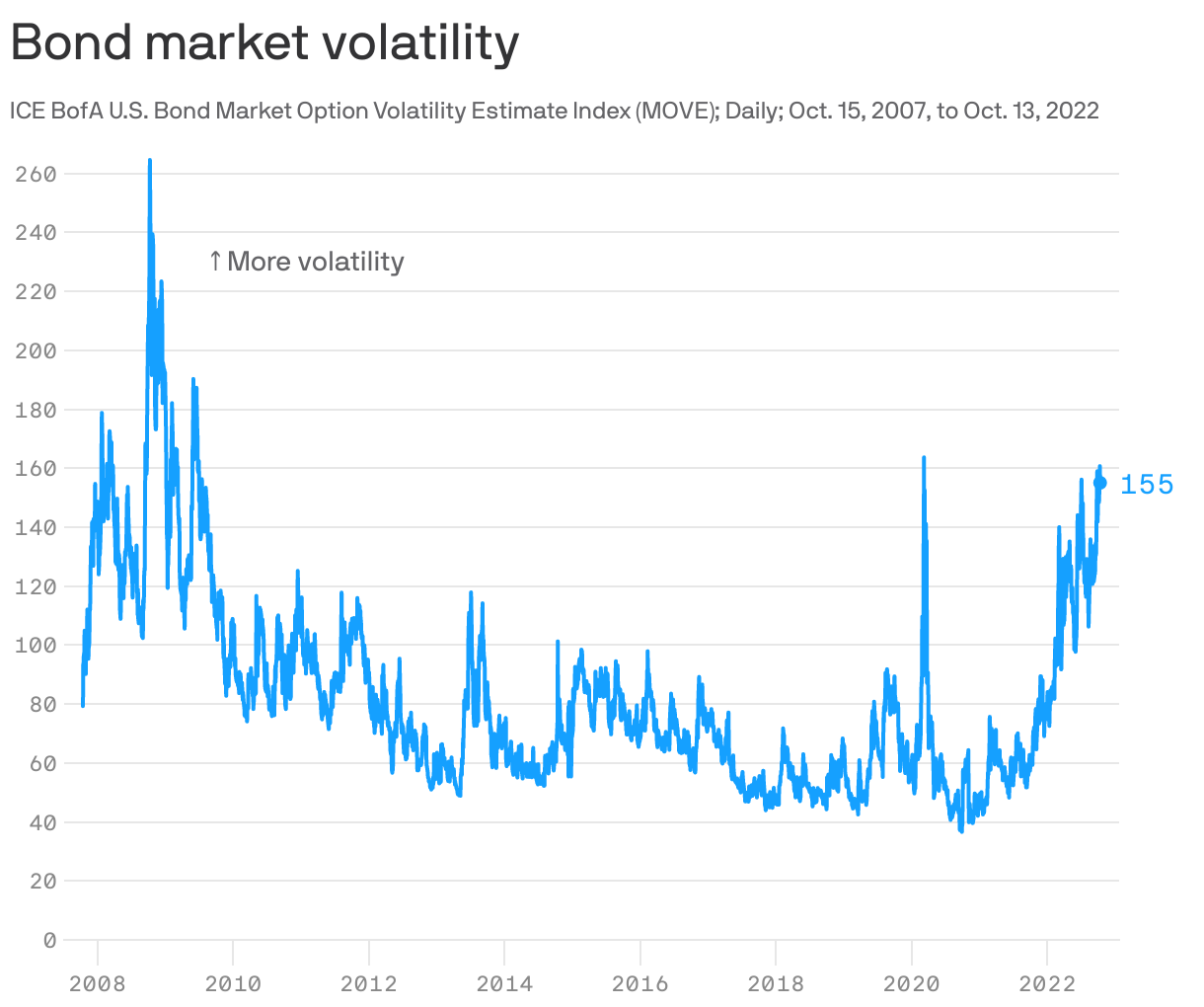

Bond market volatility is at COVID-crisis levels

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

Open embedded content from datawrapper.dwcdn.netThe bond market's version of the VIX — a volatility index — is freaking out.

What’s happening: The index that measures Treasury market volatility is flirting with levels not seen since the peak of the COVID-induced market crisis of March 2020.

Why it matters: Turbulence in safe haven Treasuries is a sign that markets aren’t functioning as smoothly as they should. And it comes as the Fed is only just beginning to extract itself from the COVID-era bond purchases that propped up the market.

- Problems with liquidity (the ability to easily buy and sell without moving prices sharply) in the Treasury market are concerning — and they "could spill over into broad financial stability concerns," wrote Javier Corominas, Oxford Economics' director of global macro strategy, in a research note Thursday.

State of play: Volatility can be something of a self-sustaining spiral.

- Big price swings trigger margin calls for hedge funds and speculative investors. That leads to selling, which leads to losses, which leads to more selling — and fuels further volatility, Corominas wrote.

Context: The benchmark 10-year Treasury's biggest one-day move in 2021 was a 0.16 percentage point drop on Nov. 26.

- This year: There have already been seven days with even bigger moves, as the FT reported last week.

- Thursday the 10-year went on a wild ride — the yield initially rose 0.15 percentage points after the CPI report, before clawing back about half of that.

The bottom line: The way the Treasury market functions during periods of stress has been a worry for a while now. And there's no shortage of theories for why the market has seemed to grow much jumpier lately.

- Here's a decent primer on the topic from the group of Wall Street bankers and traders advising the Treasury about issues in the market.

- For now, it will likely get worse before it gets better, wrote BofA Research analysts in a note this week.