Democratization is coming for private markets

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Sarah Grillo/Axios

Trading stocks has gotten cheaper and easier in recent years — now something similar is happening in the once exclusive world of private equity.

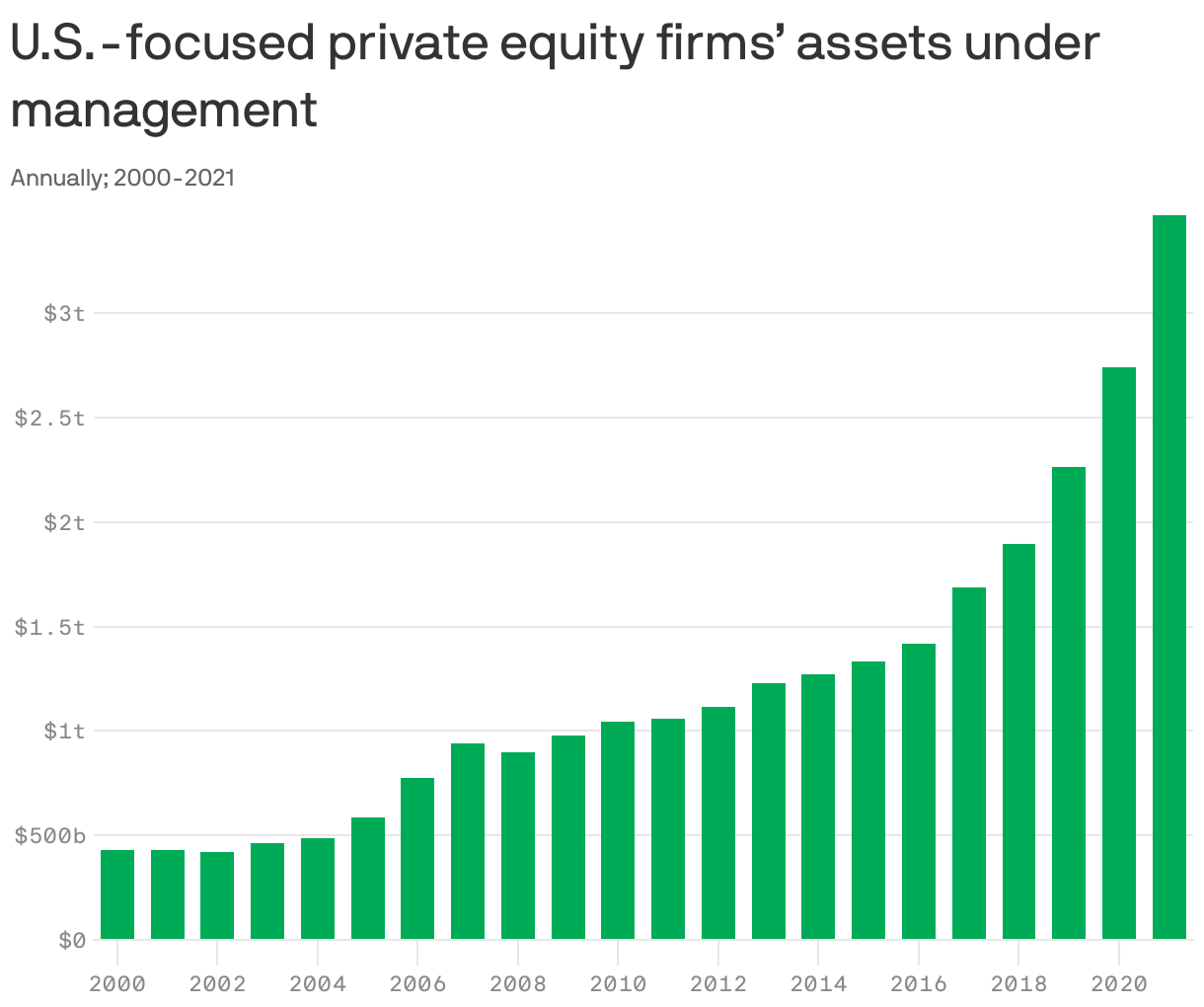

Why it matters: A majority of U.S. companies are private — and about a third of the benchmark S&P 500 index often consists of just 10 companies. Meanwhile, private equity assets under management have more than tripled since 2010 — putting even more mid-size and growth companies outside the reach of public investors.

- Some PE firms rack up returns far in excess of the S&P, though the performance of the industry as a whole is hotly debated.

- The collapse of the traditional 60/40 portfolio this year has amplified the mainstream appeal of alternative assets, says Joan Solotar, who runs Blackstone's private wealth solutions business.

How it works: Private equity firms raise capital from institutions like pension funds and endowments, pool it together and buy companies — often purchasing them out of the hands of public shareholders.

- These firms usually aim to sell those companies at a profit a few years down the road and distribute the original money (plus gains) to investors.

The big picture: For most of private capital managers' history, their fundraising from individuals was focused on ultra-high net worth types who could write $15 million-plus checks at a time.

- That's now shifting in a big way, Jason Singer, partner and head of product innovation at Apollo Management, tells Axios.

State of play: Apollo manages a host of alternative assets, which includes private equity. It recently built out a team that helps serve individual investors — and that team has gone from a single-digit headcount to nearly 150 people in just the last year or so, he says.

By the numbers: Apollo raised an average of $1 billion annually from individual investors in 2018-2020 — and it expects to lift that amount to around $15 billion per year through 2026.

- Meanwhile, at Blackstone, retail investors in 2018 represented $58 billion in assets under management, for 13% of total AUM. They're now $233 billion, and a 25% share.

These retail efforts so far have largely focused on real estate and credit strategies that have regular dividends or income streams.

- KKR has taken a similar approach — and sees it expanding. On its earnings call earlier this month, IR head Craig Larson said this about the firm's "democratized" products: "It feels to us like there’s real interest in expanding those opportunities into additional asset classes like [infrastructure] and PE."

What they're saying: “Even recently, we thought private equity reaching individual investors more broadly was a five to 10 year out trend," says Brenda Rainey, executive VP of Bain & Co.'s global private equity practice. "Based on the recent announcements of some of the large publicly traded firms, this could be in the next two years.”

Between the lines: For private equity to reach the masses, the main challenges to solve include frequently sky-high minimum buy-ins, and investments that aren't very liquid — since they usually involve locking up money for years at a time.

Tech platforms, like Moonfare and iCapital, offer accredited investors workarounds for both of those issues. They pool individual investments as low as $50,000 and write one big check; Moonfare also lets clients sell their fund exposures to other clients.

- They automate much of the tedious administrative and customer care stuff that historically made smaller-dollar investments inefficient for PE firms.

Separately, the democratized products that firms like Apollo and Blackstone have rolled out bring versions of their private market strategies to the broader "mass affluent" market — with, importantly, monthly or quarterly redemption options.

- These are the models that, according to Rainey, could eventually be replicated for private equity.

The bottom line: Private markets, by definition, will never be as liquid as their public counterparts — so there are limits to how far mass democratization can go.

- But for now, "firms will continue to innovate where they can," says Solotar.