High yield spreads race tighter as recession fears ebb

Add Axios as your preferred source to

see more of our stories on Google.

Investors are pouring back into the U.S. high-yield market, a signal that they're dialing back recession jitters — for now.

Why it matters: For a minute, things got dicey: Borrowing costs for U.S. companies with lower credit ratings shot up to levels suggesting possible recession concerns or that a sharp rise in defaults could be in the offing.

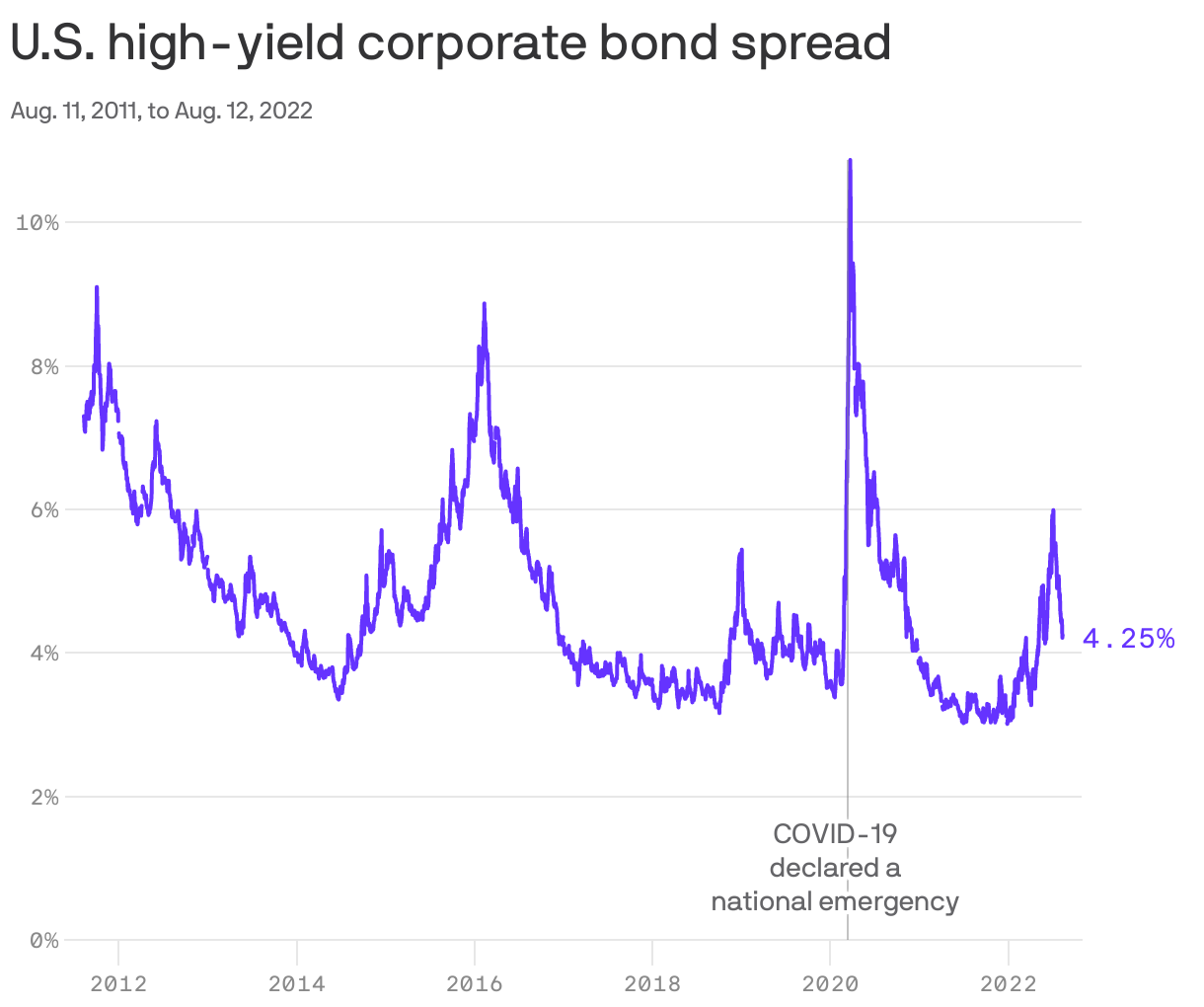

But over the last month, high-yield bond spreads over Treasuries — a measure of how much more high yield-rated companies pay to borrow compared to the U.S. government — have tightened massively. They're now actually a little tighter than the median stretching back to 2011.

- That came after spreads had surged to 6 percentage points. (The 5-point mark, which high-yield spreads breached in June, is something of a red line between a market that’s healthy, and one seeing a worrisome level of flight.)

Some of the same stuff that propelled the equity market higher in July also gave tailwinds to high yield, dragging spreads back down to earth.

- Among them: Earnings season came in better than many had expected, the Fed started providing wiggle room about potentially slowing down its pace of rate hikes — and inflation data started to cool, says Will Smith, AllianceBernstein's director of U.S. high yield credit.

So investors reshuffled. For one, hedge funds with super bearish positioning ultimately had to cover shorts — that pushed up bond prices and was a sort of “lighter fluid” on the price movement, Smith says. “The negative catalysts [that bearish investors] were waiting for didn’t really happen,” he adds.

- High-yield mutual fund and ETF investors returned: The asset class is headed for two straight months of net inflows, after six months of outflows to start the year, according to Refinitiv Lipper.

And even companies got in on the action: With loads of bonds trading in the 75 to 85 cents on the dollar range, companies have been quietly buying back their own debt in the open market, says David Norris, head of U.S. credit at TwentyFour Asset Management.

- That means that, rather than hoarding cash for a coming economic downturn, companies are deploying it to take advantage of the market dislocation.

The macro signal: High-yield spreads moving closer to risk-free Treasury rates “is generally a positive,” says Norris. “It’s credit markets expecting a softer landing, or a shallow recession, or not even entering into recession.”

What to watch: Spreads may yet widen back out as new earnings and data points trickle out.

- "It's been a pretty vicious move [tighter]. If you had told me three months ago some of those data points, like CPI, earnings and Fed commentary, I would have said high-yield would probably rally — but not this hard," says Smith.

- "And the question that we're all grappling with is: Is it too much in a short amount of time?"