Get ready for corporate default rates to climb

Add Axios as your preferred source to

see more of our stories on Google.

Open embedded content from datawrapper.dwcdn.net

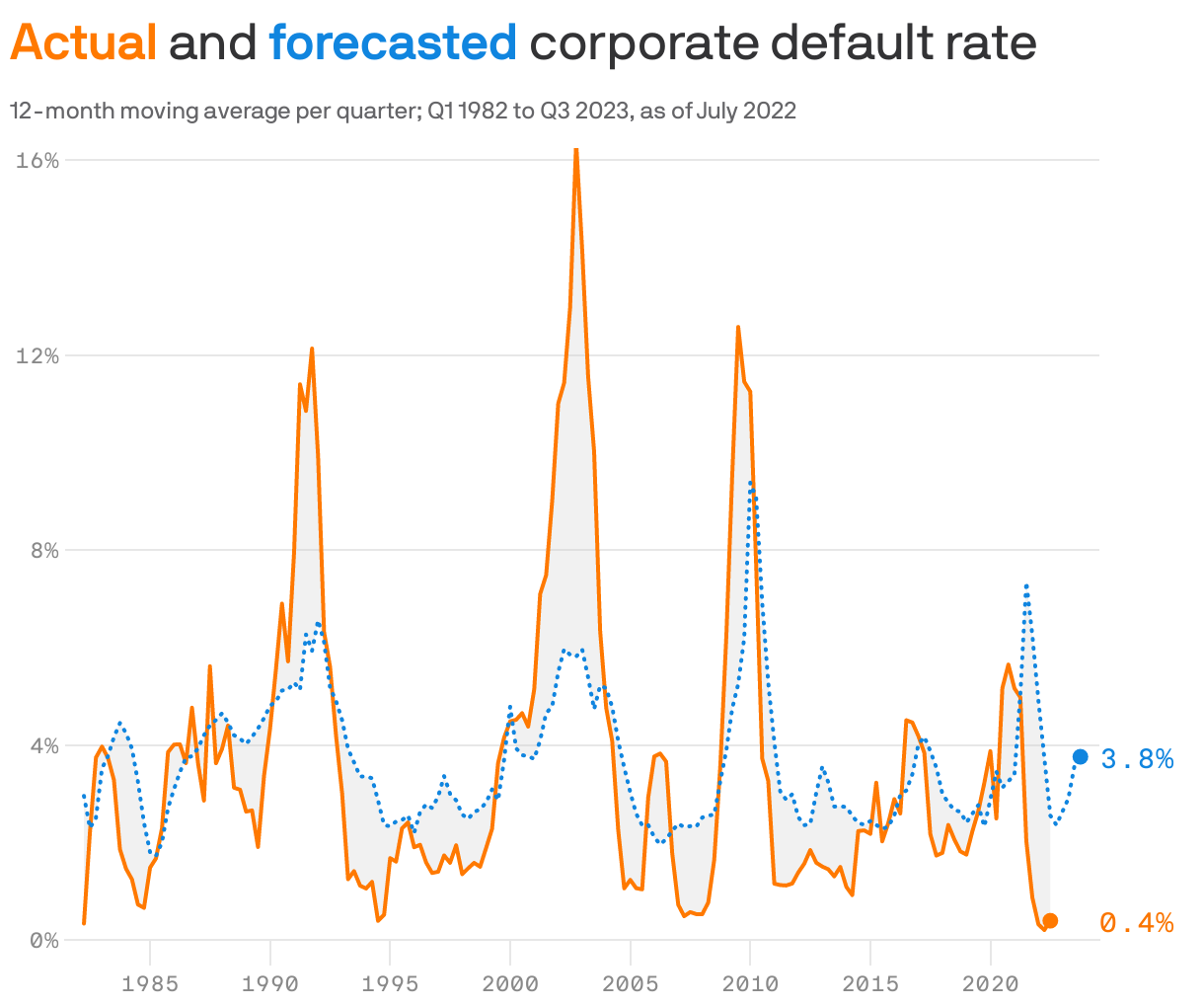

Open embedded content from datawrapper.dwcdn.netDefault rates in the U.S. corporate bond market hit all-time lows near zero last year — but they’re starting to tick back up.

Why it matters: With recession worries hitting a fever pitch, the question isn’t whether defaults will rise — it’s how high they’ll go, and how much damage that'll inflict on investors.

State of play: KBRA Analytics forecasts that the high-yield bond default rate a year from now will be around 3.76%.

- That’s up from 0.40% now — and would surpass the historical mean of 3.61%.

What they're saying: "We are in a post-COVID world, and everything is kind of going back to normal," Van Hesser, KBRA's chief strategist, tells Axios. "Now the question is: what follows?"

- Already, the capital markets have all but cut off the lowest-quality issuers, the ones with "CCC" credit ratings. Constrained access to capital is usually an early sign that defaults will soon rise.

- BofA Research noted in July that a CCC-rated refinancing hadn't cleared the market since February. And overall high-yield issuance has slowed to a near-standstill, according to Leveraged Commentary & Data (LCD).

Threat level: In past recessions, default rates have spiked above 10%.

Yes, but: There’s reason to think they won’t climb nearly so high in the upcoming default cycle. That's because, for one, we just went through a default cycle two years ago that cleared weaker companies out of the bond market.

- For another, the exceedingly loose credit conditions of 2021 allowed companies to virtually eliminate near-term maturities. Goldman Sachs estimates there's just $125 billion of high-yield bonds maturing in 2023 and 2024 combined (that jumps to around $200 billion per year starting in 2025).

- Last year's loose conditions also mean companies can better afford their debt — 36% of U.S. high-yield bond issuers have a coupon of less than 5%, a claim that only 16% of issuers could make in December 2019, as Oaktree Capital Management wrote in a recent market commentary.

- Finally, credit quality in the high-yield market has also improved over the last decade. Bonds with a credit rating of BB (the highest high-yield rating) now constitute 53% of the U.S. high-yield bond market, up from 43% in 2012, Oaktree notes.

The bottom line: Those conditions may take the edge off the pain of the next default cycle. But they won't prevent it altogether.