Credit card balances grow at fastest pace in decades

Add Axios as your preferred source to

see more of our stories on Google.

Credit card balances are ballooning at the quickest pace in decades, reflecting higher prices and more open accounts than ever before.

Why it matters: The debt will get costlier for borrowers to carry as the Fed raises interest rates quickly to tamp down scorching hot inflation. There are early signs lower-income consumers are starting to fall behind on payments.

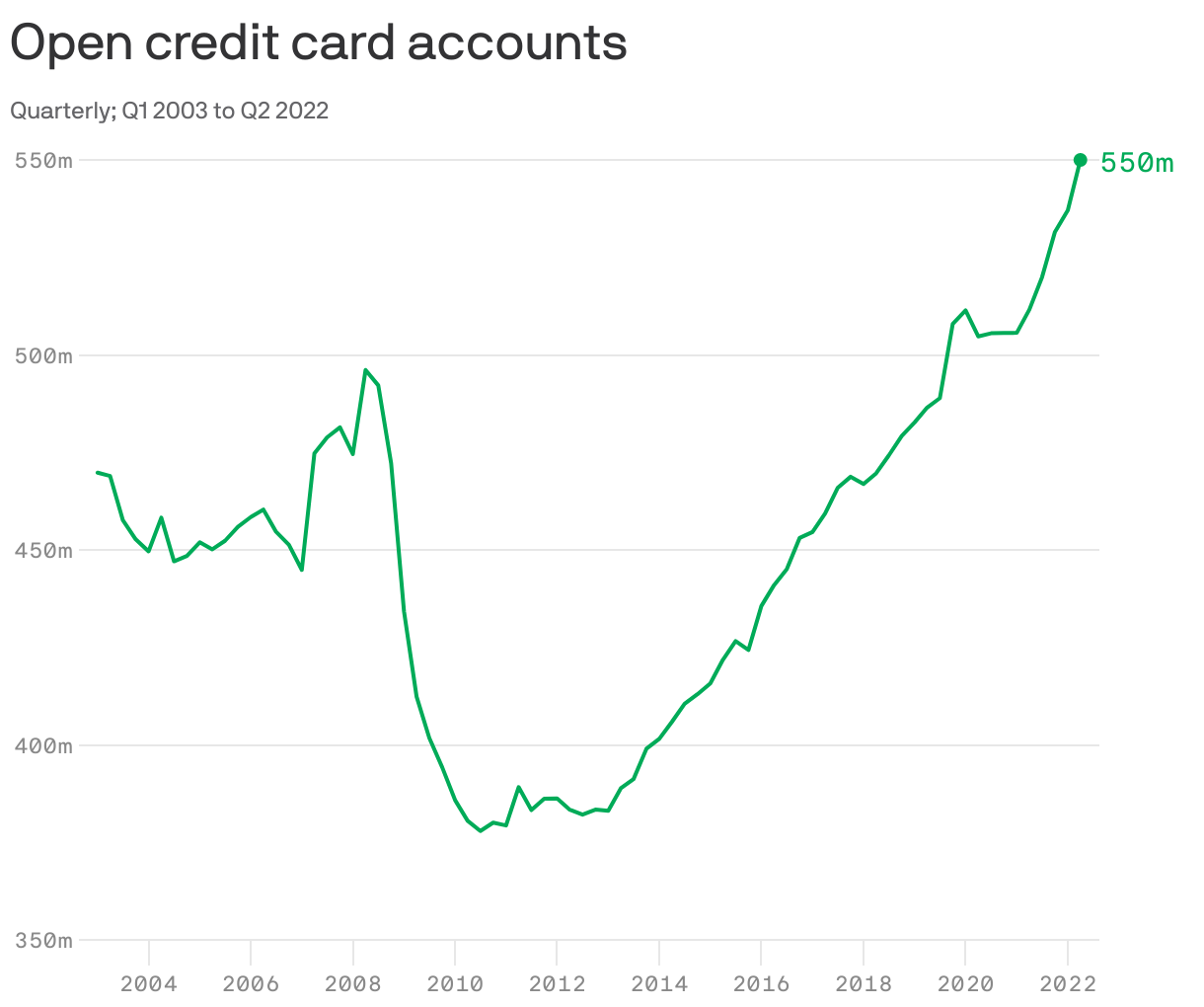

Two fresh stats — courtesy of the New York Fed — tell the story:

- Credit card debt surged by $46 billion last quarter — a 13% jump from the prior year that marks the biggest increase in over 20 years.

- Americans opened 233 million new accounts in the April-June period, the most since 2008.

By the numbers: Household debt now totals more than $16 trillion. Credit card balances make up $890 billion of that.

- Credit cards remain historically low, but they are rising — particularly among those in the poorest zip codes, according to the New York Fed.

What they're saying: "The recent uptick in delinquencies in some households suggests that many communities or individuals are experiencing the economy differently," researchers wrote.

Worth noting: Credit card balances may be rising quickly, but they remain below the pre-pandemic level of $930 billion.

- And the uptick in new accounts comes alongside more advertising on the part of issuers to get people to open said accounts.

- Capital One and Discover, for instance, both saw marketing costs jump nearly 50% from a year ago, largely because of their efforts to increase credit card sign-ups, the Wall Street Journal reported today.