Stock market selloff causes pension assets to plunge in value

Add Axios as your preferred source to

see more of our stories on Google.

State and local pension assets have plummeted in value during the broader market selloff, thrusting many government pension plans back into a precarious financial position, according to a new report.

Why it matters: The health of pension plans affects their ability to pay off promises they've made to retirees and affects the budgets of cities, counties, school districts and states that are on the hook to make pension contributions.

- The S&P 500 was down about 18% for the year through Tuesday — and most pension plans rely heavily on stocks.

By the numbers: State and local pension plans are 77.9% funded, down from 84.8% in 2021, according to estimates published Wednesday by Equable, a nonprofit with Republicans and Democrats on its board that advises governments on pension issues.

- The shortfall in government pension plans — known as an unfunded liabilities — had tumbled in 2021 to its lowest point since the Great Recession after several years of stock market gains.

- But this year's selloff has caused unfunded pension liabilities to balloon from $933 billion in 2021 to $1.4 trillion in 2022, according to Equable's estimates.

- "Most public plans are fragile" though not yet "distressed," said Anthony Randazzo, executive director of Equable and co-author of the report.

The big picture: A big reason for the unfunded liabilities is that state and local governments have a median expected annual rate of investment returns of 6.9%, but their assets have not kept pace with that rate of growth, according to Equable.

- "The implicit promise of investment returns above 7% has been shown by actual market performance to be an illusion, and increasingly public retirement systems are embracing the reality that they need lower assumed rates of return," wrote the report's authors, Randazzo and Jonathan Moody.

Threat level: The likeliest effect of reduced asset values is that governments will be forced to divert more funding from public programs to their pension plans, thus reducing their ability to prop up basic services, according to Equable.

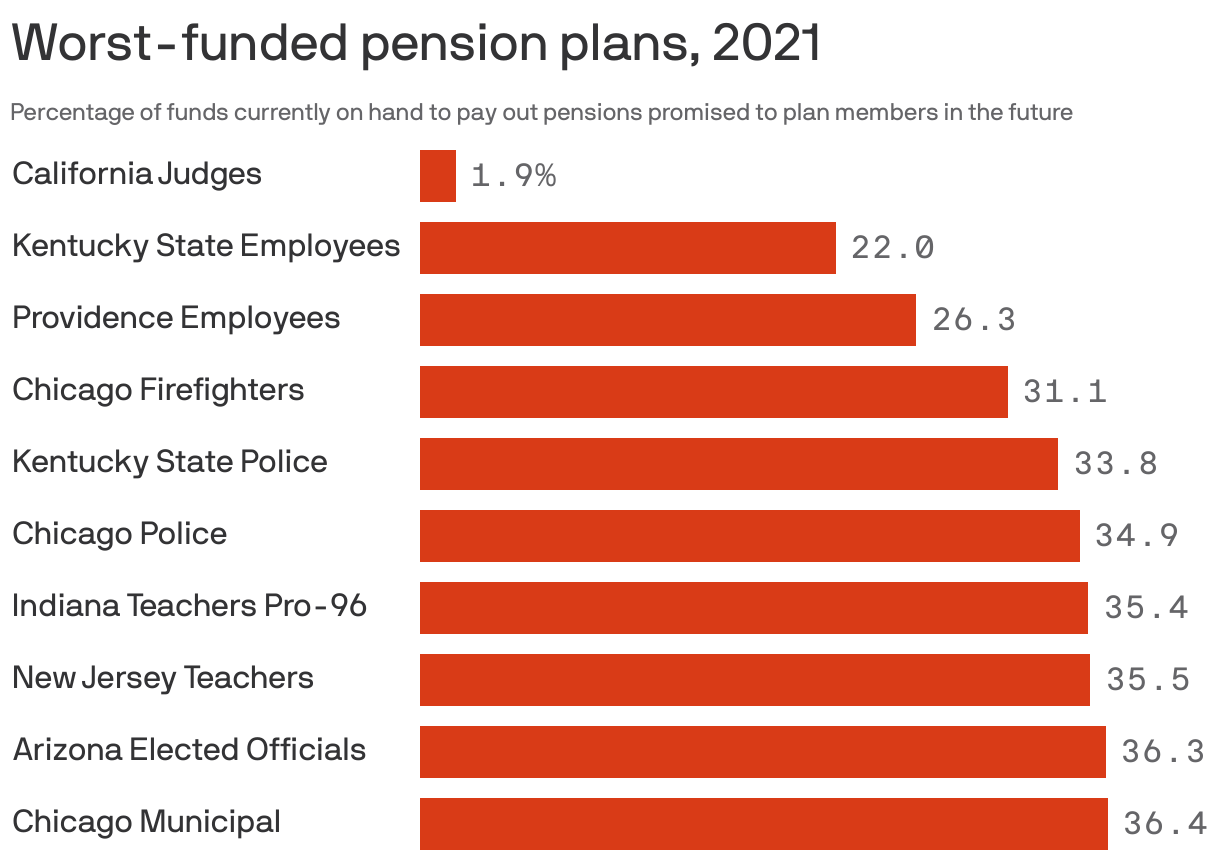

- The five worst-funded statewide pension plans as of 2021 were California Judges (1.9%), Kentucky State Employees (22%), Kentucky State Police (33.8%), Indiana Teachers Pre-96 (35.4%) and New Jersey Teachers (35.5%).

- The five worst-funded local plans as of 2021 were Providence Employees (26.3%), Chicago Firefighters (31.1%), Chicago Police (34.9%), Chicago Municipal (36.4%) and Chicago Laborers (45.9%).

- A few more bad years and some of the Chicago pension plans may be in a "death spiral," Randazzo said.

Zoom in: Some public pension funds are turning to potentially risky deals to bolster their funded status.

- More than 100 borrowed money in 2021, according to a Municipal Market Analytics assessment of Bloomberg data. That was double the highest previous number.

Of note: Pensioners are particularly susceptible to the 40-year high in inflation because the average cost-of-living-adjustment (COLA) for a government pension plan is 1.58%, according to Equable.

- Eight states have no COLA provisions at all or have suspended it.

- And even in states that have COLA provisions in place, "only a select group of public retirees have a reasonable hope that their pension benefits will keep up with inflation," Equable reported.

But, but, but: While 2022's selloff has delivered a setback to pension plans, even with the projected declines from last year they remain better funded than any other year since the Great Recession.

💭 Our thought bubble: Political leaders often prioritize short-term funding needs over the long-term. Hence why pension plans are perpetually underfunded.