Why natural gas costs so much more in Europe

Add Axios as your preferred source to

see more of our stories on Google.

Surprisingly, the natural gas market is not as global as you might expect.

Why it matters: There's a limit to how much U.S. production can help European allies wean themselves off Russian gas.

- This is a bummer for Europeans who need to heat and cool their homes — and for the West's ability to prevail in the economic war against Russia ... but, hey, it does help keep stateside prices low (relatively speaking).

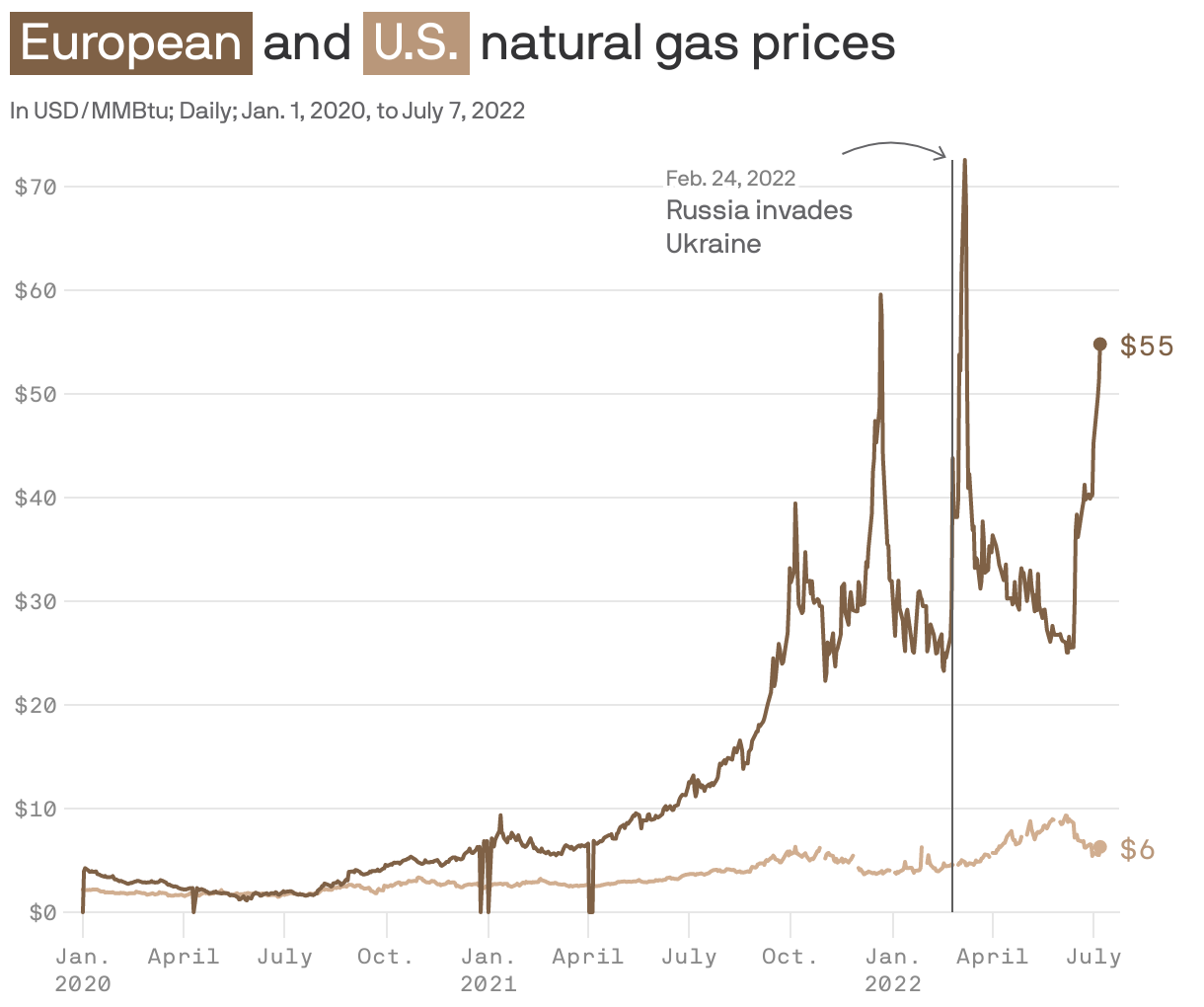

Context: The European benchmark, known as Dutch TTF, is priced in euros per megawatt-hour, making it hard to see just how much more those on the continent pay versus Americans’ average cost. The U.S. benchmark Henry Hub gas is priced in dollars per million British thermal units (mmBtu).

- Research firm Rystad Energy crunched the numbers for Axios, converting the daily TTF price into dollars/mmBtu, for an apples-to-apples comparison going back to just before the pandemic.

The result: Yikes. As of the end of last week, European prices were a staggering ninefold higher than U.S. costs.

- Prices were on top of each other early in the pandemic, when energy demand was low.

- But Europe's prices started skyrocketing last year, on the heels of an unusually cold winter, and as Russia had already started curtailing supply.

So why don't more U.S. producers send their gas over to Europe to tap into the potential profit bonanza? The answer has to do with the transport process: To ship it overseas, natural gas has to be liquefied.

- The complex and expensive facilities that transform gas into LNG (liquified natural gas) are a relatively new thing in the U.S. — borne of the recent shale boom — and right now stateside producers are maxing out the available liquefaction capacity, Emily McClain, Rystad senior analyst, tells Axios.

- That traps much of our gas here — and means that U.S. prices are largely driven by regional dynamics rather than global arbitrage.

The oil market, on the other hand, is more global: Prices for U.S. and European benchmarks (known as WTI and Brent, respectively) track pretty closely to each other.

- Oil's much easier and quicker to ship, so "the arbitrage dynamics are much tighter," says Rystad senior analyst Louise Dickson.

What's next: The West's antagonistic relationship with Russia has increased investor appetite for funding new U.S. gas liquefaction projects to fill the void that Russia may eventually leave. At least two projects have received a final investor go-ahead since the war began, McClain says — but they won't come online until 2025 and 2026.

- Other projects that Rystad once viewed as speculative now look more likely to move forward, she adds.

- All told, by 2030 the U.S. export capacity is now expected to more than double from current levels, she says.

What to watch: More exports shouldn't, alone, push U.S. prices higher — unless production doesn't keep up.