Homebuyers face mortgage cliff

Add Axios as your preferred source to

see more of our stories on Google.

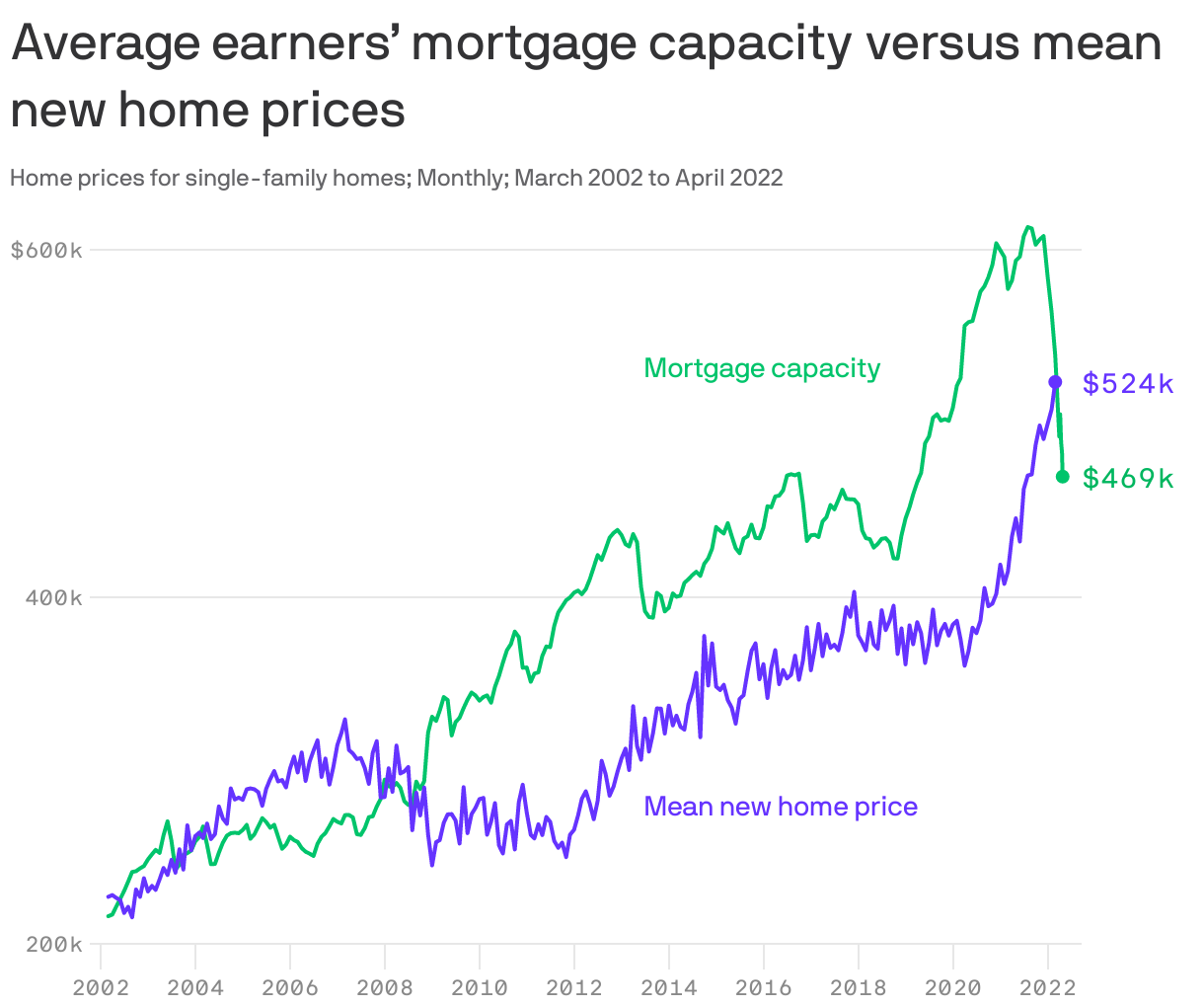

Not since the housing bubble of 2007 has there been such a big gap between the cost of a new house and the amount a two-earner household can borrow in order to buy it.

Why it matters: Homebuyers are facing a double whammy of higher prices and higher mortgage rates, which reduce the amount of money they can borrow to buy a house.

By the numbers: The average new single-family home sold for $360,000 in April 2020, according to Census Bureau data. Less than two years later, in March 2022, that number had risen by 45% to $524,000. (The median price rose 41% in the same period.)

- At the same time, the mortgage available to two people making average hourly earnings has shrunk by $144,000 since August, and now stands at a relatively low $469,000 — assuming they limit their mortgage payments to no more than 28% of their combined income.

The bottom line: Houses are still affordable if you're already in one. But market dynamics right now make it clear why new transactions are slowing dramatically.