Russia broke the bond market

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Shoshana Gordon/Axios

The prospect of a Russian government bond default may be the most visible market symbol of Russia’s new pariah state status — but there’s also nearly $100 billion in Russian corporate bonds now sitting in a sort of investor limbo.

Why it matters: It's yet another way that markets have been upended in the aftermath of Russia’s invasion of Ukraine — alongside the broken nickel market and sky-high European energy prices.

- The gridlock in the market for Russian bonds is unprecedented, says Sergey Goncharov, emerging markets portfolio manager at Vontobel’s Fixed Income Boutique.

- “The infrastructure has been challenged … trades and basically any market activity related to Russia are definitely difficult to get executed,” Goncharov says.

How it's playing: Want to sell those bonds backing a Russian oil company — which your firm either requires you to sell, or you just feel kind of dirty holding onto? You might have a hard time doing it.

- Any one trade often goes through several intermediaries — like payment agents and brokers — and at each step along the way someone has to decide if it’s compliant with U.S. and European sanctions, Goncharov says.

- Trades that used to close in a matter of days now stretch into weeks of uncertainty.

Want to collect interest payments on the Russian corporate bonds that you hold? Don't hold your breath for that either.

- Just like doing a trade, paying interest also goes through a series of intermediaries, all of whom have to make the same type of decisions related to sanctions compliance.

- So far, Russian Railways, Nordgold and Eurochem have all failed to pay their bondholders — and they blame the sanctions for preventing their payments from hitting creditor accounts.

Moreover, if there’s a default, there's no playbook for orchestrating a consensual debt restructuring and getting a recovery on your bonds.

- We outlined the difficulty of addressing a Russia sovereign debt default, and the driving principle is the same with corporates: There's no clear mechanism that issuers and bondholders can use to talk to each other and work out a deal.

The bottom line: Both Russia and Russian companies appear to have the willingness and the means to pay interest — but can’t get it done.

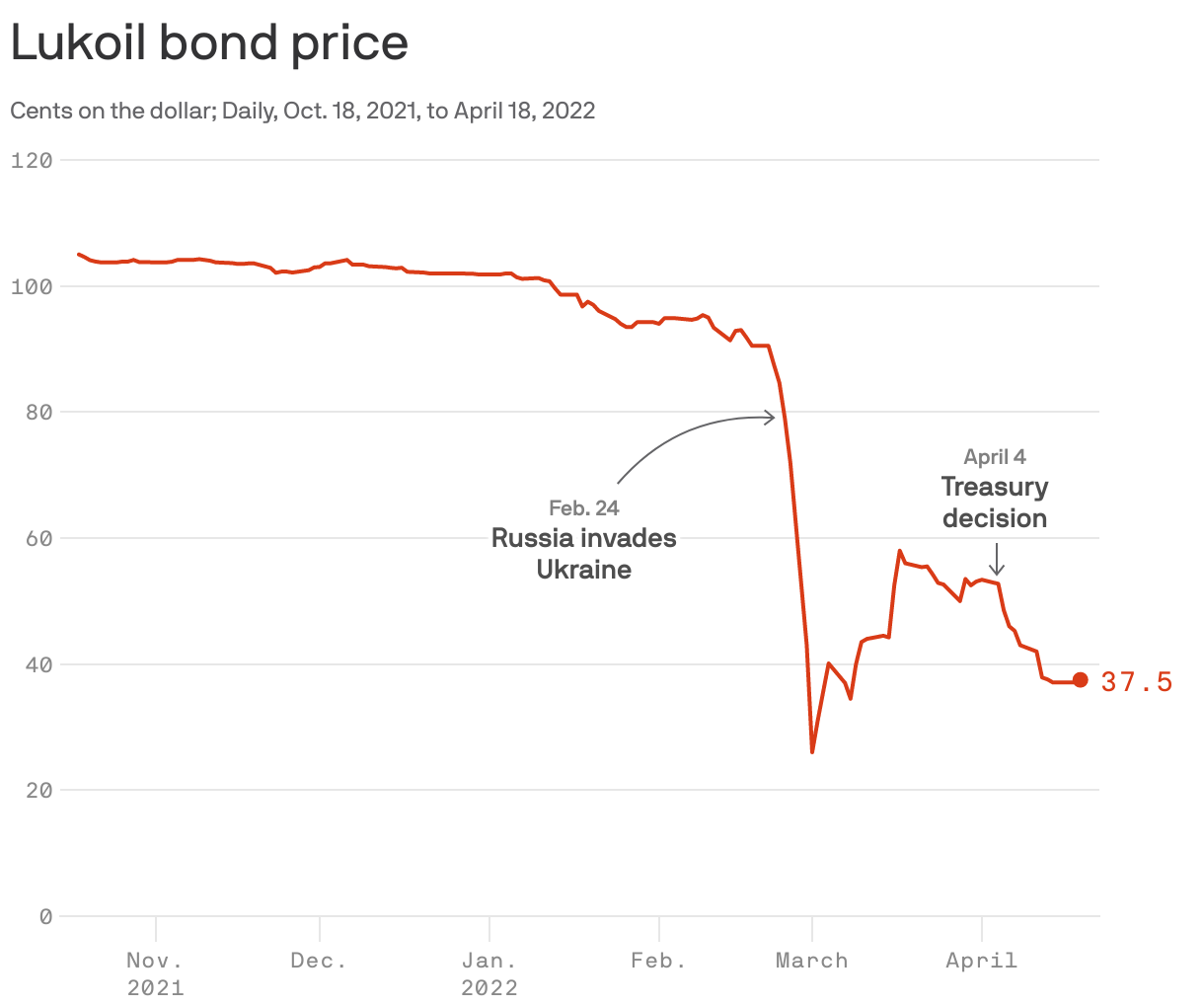

Charted: Bond reality check

Default risk for Russian corporate bonds got a little more real on April 4.

- That's the day the U.S. Treasury Department forbade Russia from accessing dollar reserves it holds in U.S. bank accounts to pay interest on its bonds.

State of play: Though the move applies to government bonds, it doesn't bode well for the ability of Russia-linked entities — like energy company Lukoil — to continue making good on their obligations.

- Flashback: Russian bond prices had strengthened over the course of March after companies showed a willingness to keep making payments even as sanctions excised Russia from the international financial markets.

- "But in April, this paradigm has been challenged because of the Treasury ruling, and the prices have corrected again," Goncharov notes.

Editor’s note: This story has been updated to refer to Russia’s action as an invasion (rather than conquest).