The JOBS Act, 10 years later

Add Axios as your preferred source to

see more of our stories on Google.

Photo Illustration: Shoshana Gordon/Axios; Photo: Daniel Acker/Bloomberg via Getty Images

The JOBS Act celebrated its 10th birthday on Tuesday. Signed into law by President Obama to great bipartisan fanfare, it was intended to increase the number of companies going public but has yielded mixed results.

Why it matters: The bill was designed as an antidote to some of the Sarbanes-Oxley Act’s onerous auditing and reporting rules and the SEC's failure to make it easier for companies to go public.

Flashback: The law that was eventually named the Jumpstart Our Business Startups (JOBS) Act was born out of Washington's efforts to counter the drop-off in IPOs in the years following the dotcom bust.

- "If you’re a startup and you take money from early-stage investors, there are really only two ways to return that capital to the investors… selling or going public," Latham & Watkins partner Joel Trotter said on Tuesday during a roundtable hosted by the House Financial Services Committee, which convened participants who worked on the law. "We thought the balance had tilted too far toward M&A."

- Some of the legislation's shepherds also touted public companies as significant job creators.

Yes, but: "What determines a company going public: the market ... and the stage of a company and the availability of private capital for funding," University of Florida professor Jay Ritter, who studies IPOs, tells Axios. "All of these things are independent from tweaks in regulation."

- The JOBS Act also made it easier for companies to not go public sooner, he adds, for instance by increasing the maximum number of shareholders of record a company can have before it has to register to go public.

- The boom in available private capital in the decade since the law passed also affected IPO decisions. "If it wasn't there, there would probably be fewer startups, and there would be more hasty exits," Ritter said.

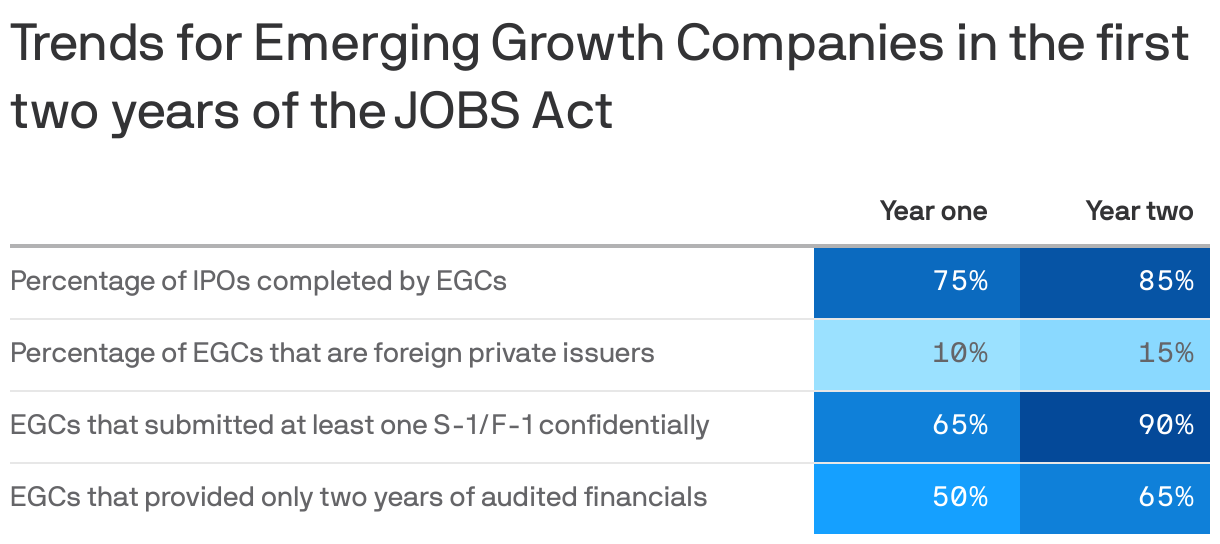

But, but, but: The JOBS Act did include some productive provisions — namely allowing emerging growth companies (EGCs) to confidentially file a draft of their IPO prospectus for feedback from the SEC, and the ability to "test the waters" with institutional investors, says Ritter.

- While in office, SEC Chairman Jay Clayton extended those benefits to all companies in a bid to further stimulate IPOs.

Moreover: Proponents of the legislation also tout the high share of EGCs among IPOs in the years since, hinting that the JOBS Act's on-ramp and lower compliance burden were effective tools.

- Since 2013, 93% of U.S. IPOs were completed by EGCs, per a report from the House Financial Services Committee.

What we're watching: Whether the SPAC mania and cryptocurrency boom will cool regulators' interest in new rules that are in the spirit of the JOBS Act.

One boom, one whimper

Along with IPOs, the JOBS Act included provisions that dealt with other forms of fundraising — like crowdfunding and private capital raises.

- While crowdfunding (and its cousin, Regulation A+ offerings) didn't become the blockbuster hit their architects hoped, the newfound ability for startups to fundraise through "general solicitation" made it possible for platforms like AngelList to flourish.

Crowdfunding and Regulation A+:

- Crowdfunding offerings in the first three years after the provision took effect in 2015 were well below the then-limit of $1.07 million, despite more companies using it, per SEC staff reports. (2020 was a record year, however.)

- And while the number of offerings under the updated Regulation A+ went up, the capital raised in aggregate and the number of offerings have paled in comparison to traditional IPOs, suggesting it remains a more niche fundraising mechanism.

Private placements:

- The JOBS Act lifted the ban on general solicitation for companies raising capital through a Regulation D exemption — that is, the usual startup-style raising of venture capital.

- The only caveat was that the company would have to ensure that it was raising only from "accredited investors," which excludes checks from friends and family that don't meet accreditation requirements. Until 2020, those were income- and wealth-based, though certain professional investors can now meet them thanks to their jobs.

- Most important, Title II made it possible for AngelList (and later, other marketplaces) to flourish. The company, which wasn't charging fees before the JOBS Act, and thus avoided legal troubles, became the go-to network for accredited angel investors to meet startups looking for funding.

- A report from the House Committee on Financial Services also notes that sites like AngelList have contributed to an increase in funding for startups led by underrepresented founders.

The bottom line: The JOBS Act being a bit of a hodge-podge of various measures has not surprisingly led to some provisions being more successful than others.