The day everything — and nothing — changed for the Fed

Add Axios as your preferred source to

see more of our stories on Google.

Illustration: Sarah Grillo/Axios

The Federal Reserve surprised the market Wednesday with new hints about its timeline for a rate liftoff — and an acknowledgment of taper talk.

Driving the news: Investors were on one hand relieved the Fed may act to keep the market from getting (more) overheated, and on the other skittish about the pending removal of the punchbowl.

Why it matters: The signals point to a Fed that's increasingly willing to contemplate a pullback from the emergency market support that began last spring in reaction to the pandemic. But don't expect these changes to happen any time soon.

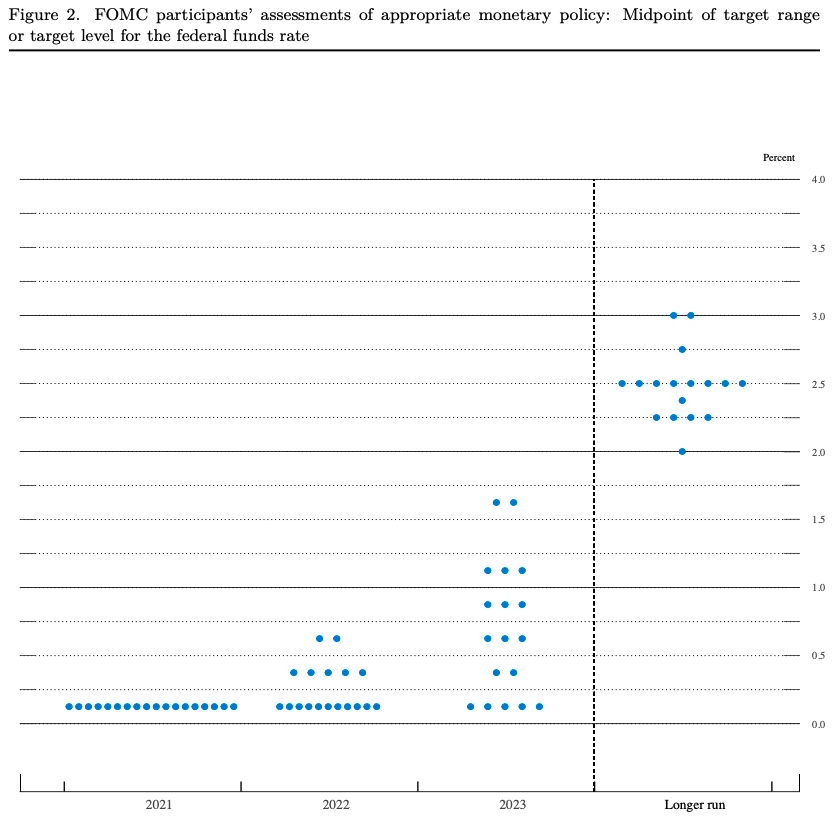

What changed: The "dot plot" of Fed member sentiment indicates a median expectation of two rate hikes by the end of 2023, up from zero.

- Fed chair Jerome Powell acknowledged that this week's meeting of the Federal Open Market Committee is the "talking about talking about tapering" meeting.

- That means that it may actually begin discussing the appropriate timeline to taper its $120 billion per month asset purchases at its next meeting (July 27-28).

What didn't change: There still won't be any tapering until December or the beginning of next year — at the earliest.

- The Fed still isn't likely to hike interest rates for years.

What they're saying: "The Fed is still going to be remaining accommodative from a policy standpoint," Don Ellenberger, senior portfolio manager at Federated Hermes, tells Axios.

- Especially considering the "real" fed funds rate, after accounting for inflation of around 2%, will be negative for the next two or three years, Ellenberger notes.

State of play: Markets went into risk-off mode, with equities declining and the Treasury yield curve flattening somewhat.

- The market's reaction is probably "a bit of digestion, and a bit of position-squaring," Ellenberger says. After that works its way through the system, markets may very well return to new highs in the short term.

Our thought bubble, via Axios' Felix Salmon: Rates have been at zero for well over a year and will remain at zero for well over a year, which makes all Fed announcements inherently anticlimactic.

- In a desperate attempt to find something — anything — to seize upon, observers turn to the dot plot and parsing the semantics of "talking." But the big picture remains exactly what we knew it would be: No change to anything.

Here are the dots. Now ignore them.

The Fed updated its "dot plot," which tallies where each member expects the benchmark fed funds rate to be at the end of 2021, 2022 and 2023.

Driving the news: The new median dots imply there would be two rate hikes by the end of 2023. This compares to the March dot plot that implied no rate hikes in that year.

- Stocks sold off and interest rates jumped on the change, suggesting market participants are worried tighter monetary policy is coming sooner.

What they’re saying: Powell explicitly pushed back on this interpretation, saying: "Dots are not a great forecaster of future rate moves. … Dots are to be taken with a grain of salt."

Others former Fed chairs agree...

“I think that one should not look to the dot plot, so to speak, as the primary way in which the Committee wants to or is speaking about policy.”— Janet Yellen, March 19, 2014

“I think you could also retitle this conference 'Why We Don’t Like the Dot Plot.' I think the dot plot is like the advanced level of the video game. If you haven’t been to the first 12 levels, forget about the dot plot.”— Ben Bernanke, Nov. 30, 2016