U.S. banks face liquidity dilemma as they sit on glut of cash

Add Axios as your preferred source to

see more of our stories on Google.

U.S. markets needed liquidity last year, and the government helped provide it. Now, by at least one measure, that liquidity is starting to erode bank margins.

What’s new: Net interest margins at U.S. banks reached record lows on average in Q1 2021, according to new data from S&P Global Market Intelligence. That's largely due to a glut of cash sitting on bank balance sheets, along with the low-rate environment.

Why it matters: The market debate is raging over whether the Fed should pull back from its unprecedented market support. Evidence of the bank cash pile is just one more data point that indicates there’s extra money in the system.

Yes, but: Banks are doing just fine, overall. In fact, they had record profits in Q1 2021, thanks to noninterest income in the form of stock trading, IPOs and SPAC formations.

- They’re also poised to do even better, on the loan margin side, if and when rates go up.

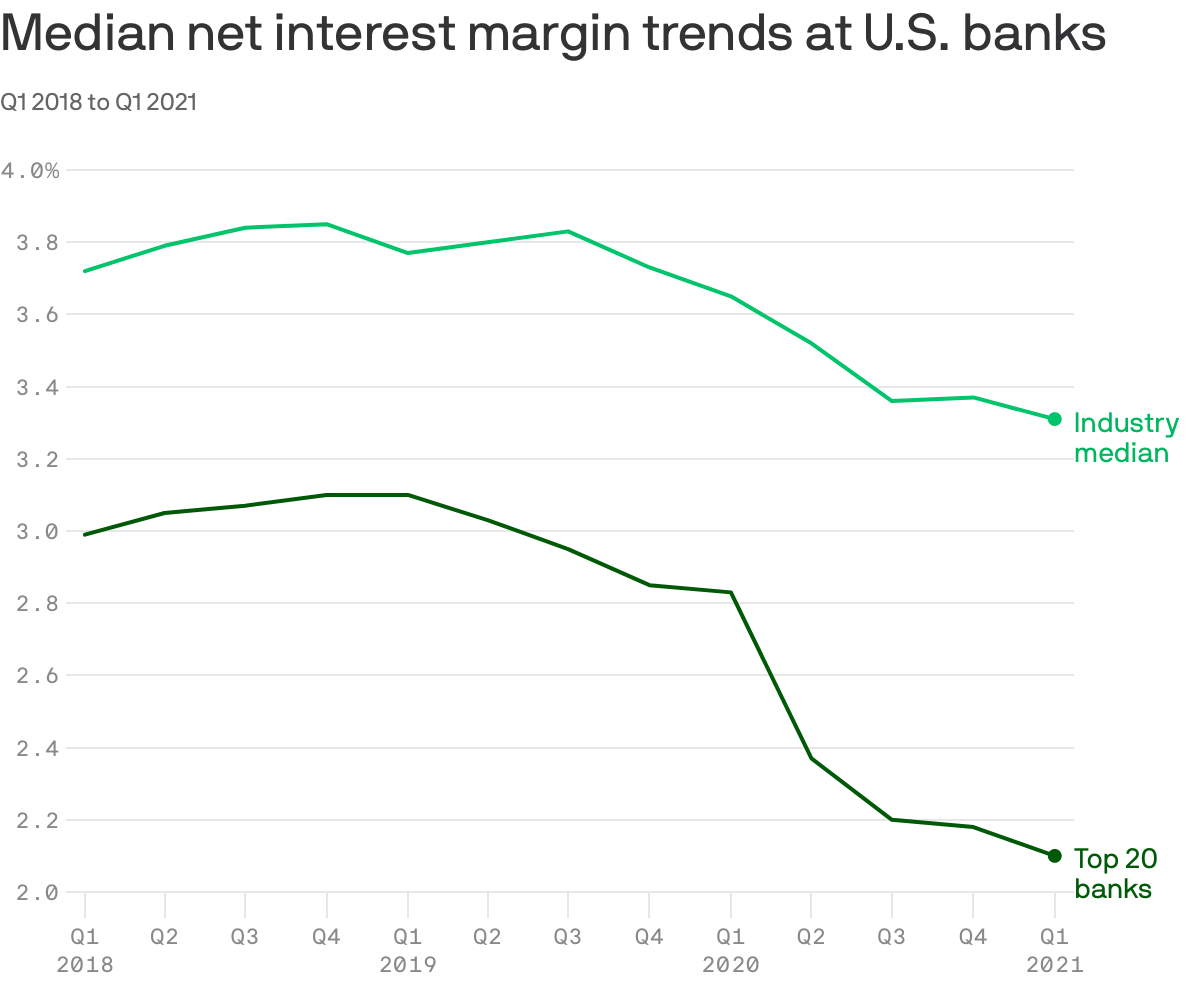

By the numbers: U.S. banks’ median net interest margin — a measure of the difference between interest income and interest paid out — hit a record low in Q1, at 3.31%, from 3.37% in Q4 2020. That’s down from a recent high of 3.7% in mid-2019.

- Among the top 20 largest U.S. banks, the median fell to 2.1%, from 2.18% the prior quarter and 3.1% in 2019.

- In Q1 2021, deposits grew 17% from the first quarter last year, while loan balances dipped 1.2% (or 5.5% when excluding the low-interest PPP loans).

- Banks' loan-to-deposit ratio fell to 59% in Q1, from 69% a year earlier.

What they're saying: "Banks have a dilemma. They have all these deposits and are not able to deploy it into loans. They're also reluctant to put too much into securities because yields are so low. So right now, they're sitting on a lot of cash," S&P's Robert Clark tells Axios.

The bottom line: The Fed and Treasury are not overly concerned about banks' lending profitability as they debate next steps. But the dilemma facing banks is one more side effect of the liquidity sloshing around the market.