Open embedded content from datawrapper.dwcdn.net

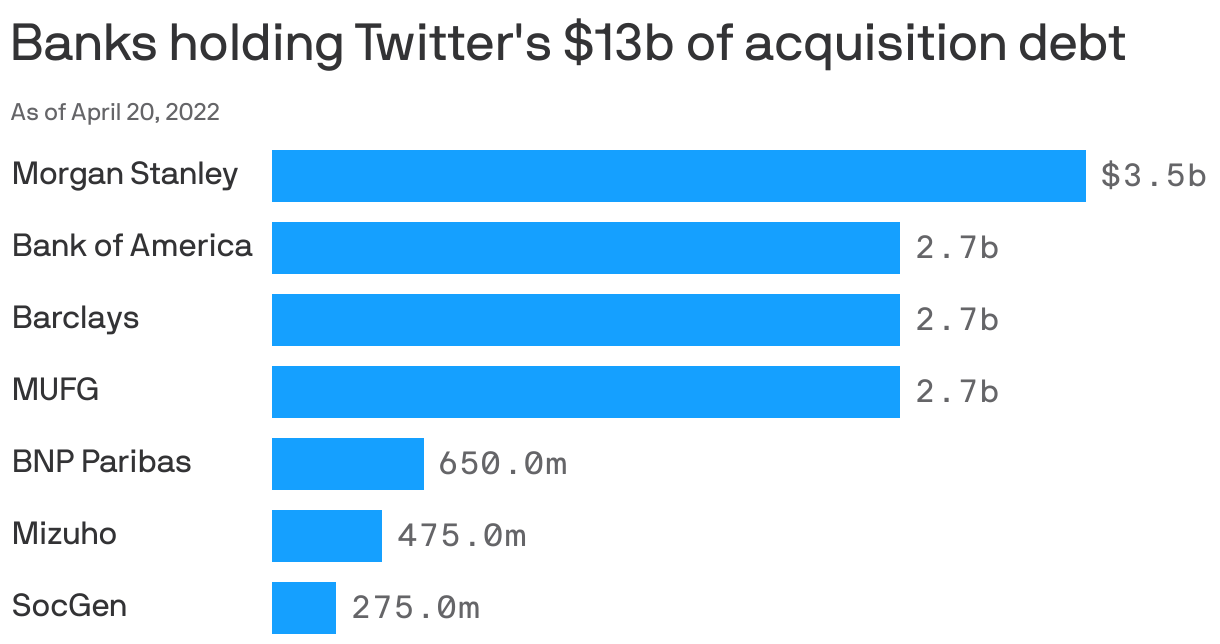

Open embedded content from datawrapper.dwcdn.netEmerging from a near freeze, most banks holding acquisition debt are seeing prices pickup, with buyers emerging. But that's not the case for the banks that financed Elon Musk's $44 billion purchase of Twitter.

Why it matters: The six banks holding onto $13 billion of Musk's Twitter financing face a double whammy: the debt limits banks' ability to underwrite new deals from other clients, and the only way to get the loans off their books is to sell at a steep loss.