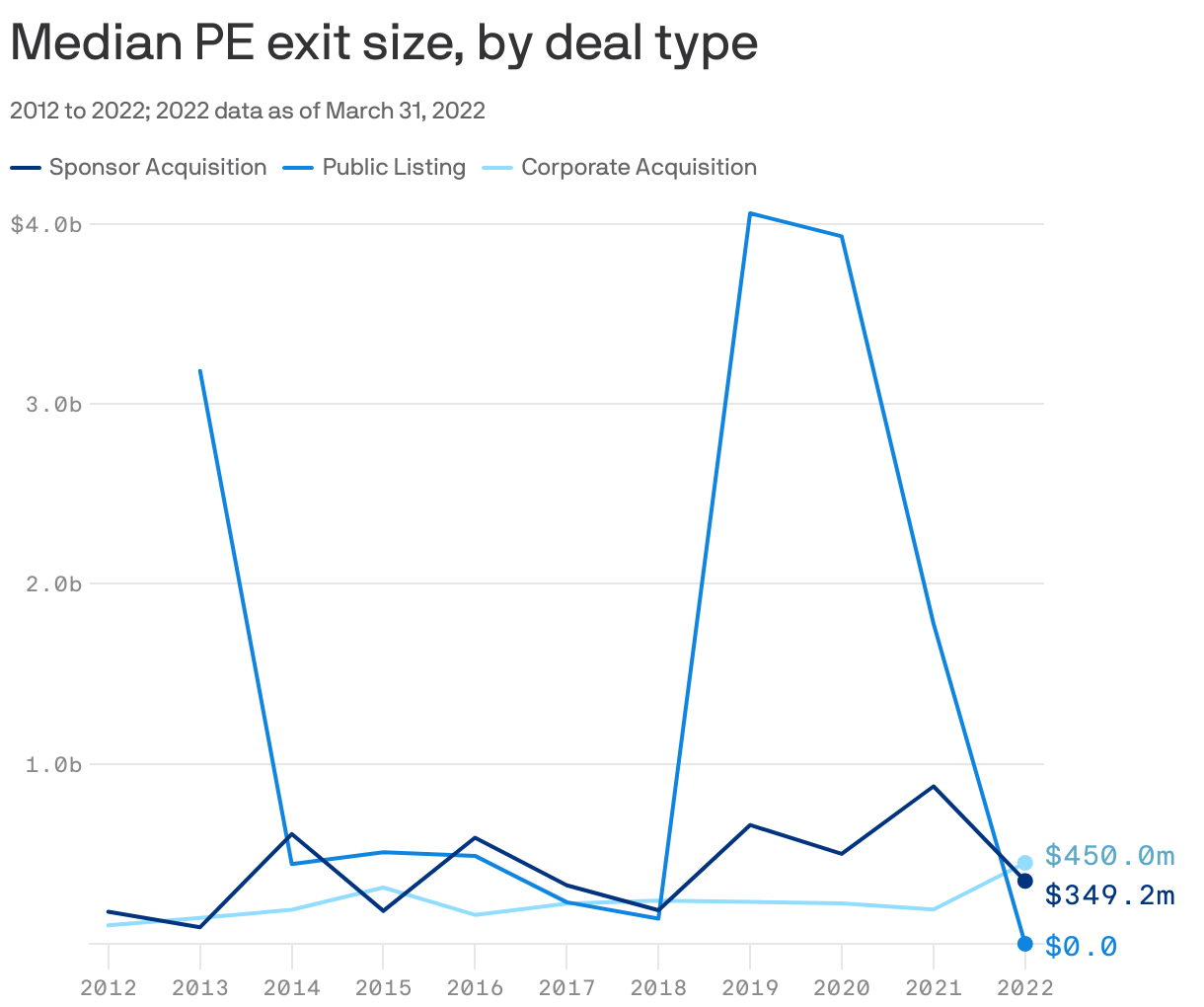

In contrast to the preceding three years, when PE shops exited investments in Q1, corporate buyers paid higher prices than private equity sponsors, as public listings effectively vanished, per PitchBook data shared with Axios.

By the numbers: In 2021, the median deal size for sponsor acquisition and corporate acquisition of a PE-owned health care company landed at $875 million and $191 million, respectively.